THE HEDGEYE EDGE

Splunk (SPLK) is a $15Bn big data/machine learning company that has been on a tear over the last 4-5 quarters. The company was an early mover in the ingestion and indexing of machine log data, and created a powerful set of APIs which allow Splunk users to search and use the data for an ever growing set of unique use cases.

There are many items we have always loved about this model, and this company, and we still see some residual long-term potential (or theoretical) upside. But in the near term we also see correlation to some trend lines of investment that we think slow in the coming months and years.

We think the slowdown will mean investors will need to pivot from EV/S to EV/FCF to Growth. These transitions aren’t always fluid and in the case of Splunk there is the bugaboo of ongoing large stock based compensation to sort through. We are also aware of more commoditizing forces of late in this category, such as the separation of elastic compute and storage in the cloud, which could also dent growth as Splunk's model mostly prices both at the more expensive side.

INTERMEDIATE TERM (TREND)

Splunk is still priced on go-go growth but multiple recent tailwinds begin to fade on a forward basis. Accelerations that drove the stock higher will not repeat next year including ~600-700bps benefit from the shift to ASC606, a big data center spending bump, plus the Machine Learning and Analytics splurge in the last year.

The company also faces secular headwinds on the margin with its tools always among the most expensive in its peer group, but also providing the most value. A recent pivot in the industry to separate expensive compute costs from cheap storage costs means there are some deflatable costs in the SPLK model, which bundles both at the higher price.

We aren’t really sounding an alarm on that one as the debate has been pretty consistent, but our recent work surfaced more chatter about offloads from Splunk or ways to limit the Splunk bill using other tools, a headwind likely to persist. In short, there are more recent wins / anecdotes by competitors that have caught our attention.

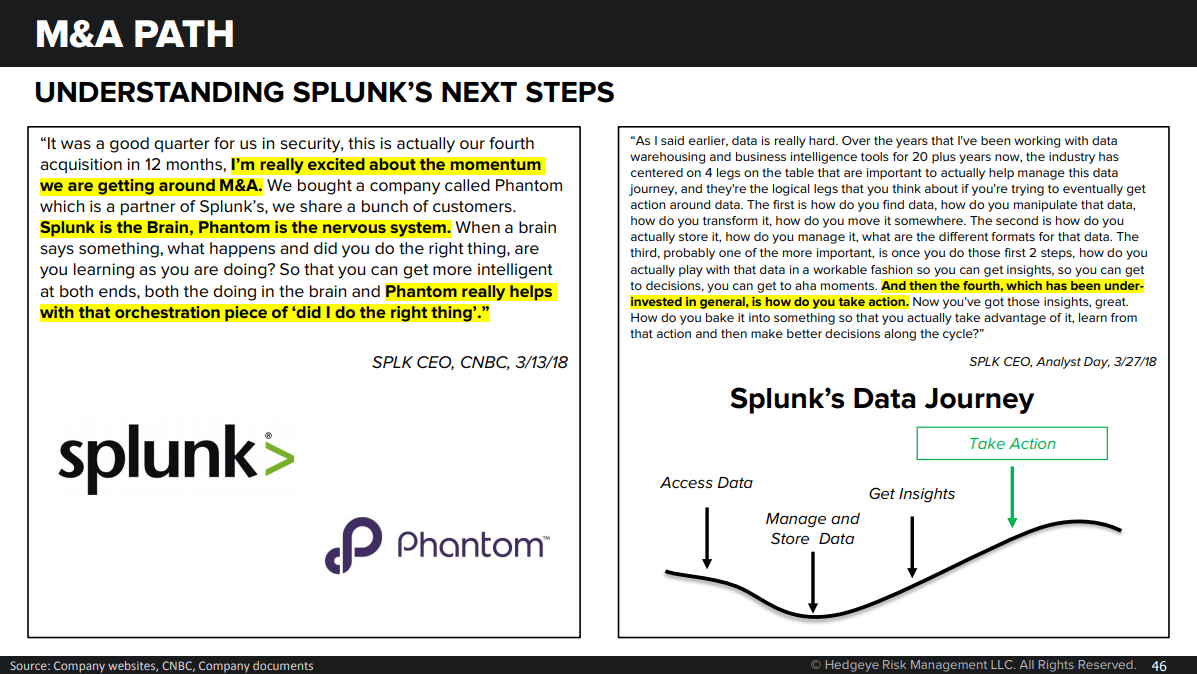

The CEO sees a path forward on functionality but it will involve ramping up the ‘M&A’ machine, already ~120bps of growth in F19 YTD. Companies who pivot from go-go organic growth to M&A plus a slowdown tend to transition from EV/S to EV/FCF and those transitions are rarely smooth. In this case stock based compensation is an extenuating factor without which there really wouldn’t be any OCF.

The story for Splunk is by no means over. Splunk is at a point similar to other large software companies when they hit similar revenue run rates who pivoted towards M&A. In this case, that’ll be the primary use for newly growing FCF. We think the pivot from go-go growth EV/S ratios to slower rates of growth, acquisitions, and EV/FCF ratios usually doesn’t sort out so smoothly.

BOTTOM LINE

We are not telling Longs to hit the competition-panic button, but the combination of slower growth and shift to FCF based valuation will at least present a sideways equation, and in our view sets up for a 20-25% downside risk profile as we enter 2019.

ONE-YEAR TRAILING CHART