“Europe’s problem is not its institutions, its Council, the Commission or Parliaments, the problem is very often nationalism, populism, and narrow-minded parochial views of people who do not believe in the common project for Europe.”

-Jose Manuel Barroso, 3/25/10

Late yesterday Jose Manuel Barroso (President of the European Commission) and Herman van Rompuy (President of the European Council) held a press conference in which they stated the willingness of Eurozone member states to take coordinated action with the IMF to “safeguard financial stability” for Greece, and the Eurozone members as a whole.

The “mixed formula” of financial support came without such details as:

- When Greece, if needed, would receive loans or the value of said loans?

- How much of the bilateral loan would come from the Europeans versus the IMF?

- What budget deficit reduction requirements will be issued for other/all member states?

And to the first bullet point van Rompuy responded, “All this, we’ll work it out later.” Is this policy?

While the Greek market shot up over 4% today and investors’ fears may be allayed for at least a day, Eurozone leaders have done little to address policy measures for the sovereign debt issues of its members. And surely the debt obligations of the other PIIGS aren’t going away just because the fear of a Greek default becomes yesterday’s news…

To return to Barroso’s quote above, Eurozone skeptics exists. And one could argue that the decision by Eurozone leaders to support Greece in a coordinated fashion—rather than a unilateral IMF-led loan—is born out of the desire of the European community to further substantiate the existence of the Eurozone as an entity. While Barroso as President of the European Commission will put his best foot forward in confirming that the Eurozone has a sound governing body, the fact remains that the Eurozone is young, only 10-years old, and still working through honing policy to benefit the whole.

Clearly, finding consensus on policy from country members with vast histories, and divergent economies and cultures, will remain a challenge. Countries will differ on stance; having a unified currency will put additional challenges (handcuffs) on exercising monetary and fiscal policy measures with such issues like debt restructuring and default.

Equally, imbalances in terms of economic weight and political influence will continue to weigh on decision making. These points were put on center stage with German Chancellor Angela Merkel’s full support of a unilateral IMF-led bailout for Greece. The fiscally conservative Chancellor wasn’t questioning the validity of the Eurozone, but suggesting that Greece continue to work to clean up its own “house” (budget deficit) before monies were placed on the table so as to not reducing Greece’s incentive to issue austerity measures to shave its imbalances.

Merkel approached the issue from a pragmatic level, conscious of her own political and fiscal constraints at home—confidence in her party’s management has waned in recent months and reaching into German coffers for Greek aid would put further strain on the German taxpayer.

While pundits could endlessly debate the benefit of a large economy like Germany to the Eurozone and vice-versa, we’ll spend our time understanding the dichotomy that exists within the Eurozone, and collectively throughout Europe, to drive our investment decisions. Despite Greece getting a hall pass for now, in light of the increasing global sovereign debt issues, things continue to shake.

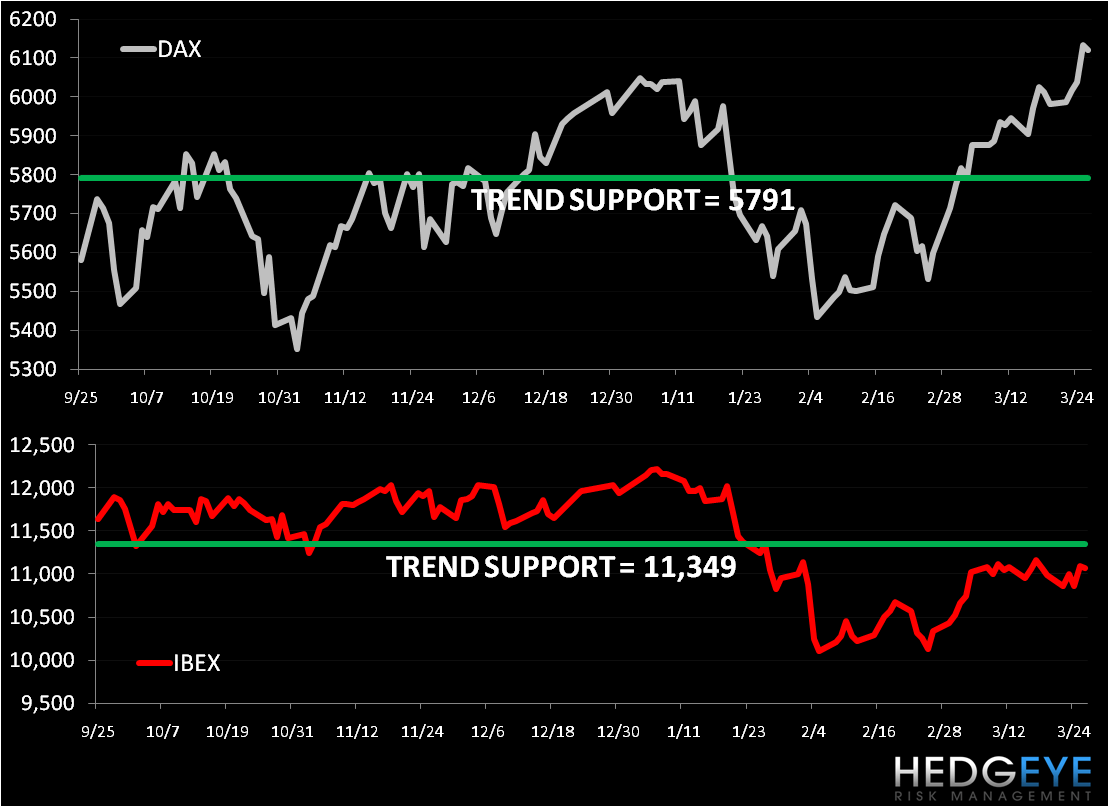

The charts below show divergence between Germany and Spain based on the DAX vs. the IBEX. While the IBEX is broken on its intermediate term TREND (3 months or more), the DAX continues to trade above its TREND line. For more on our fundamental stance on Germany, see our note from yesterday titled ‘Frau “Nein”’.

Matthew Hedrick

Analyst