Editor's Note: Below are a selection of investing insights from this week's edition of Market Edges, our weekly big picture Macro newsletter with investing implications. Click here to learn more about Market Edges.

EUROPE, CHINA & U.S. #GROWTHSLOWING

|

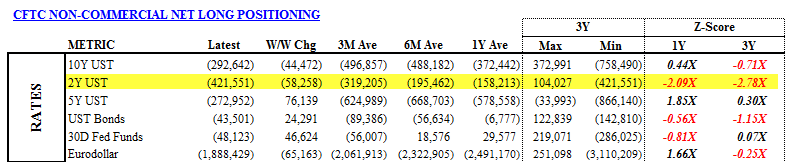

Unsurprisingly, Wall Street is (still) on the wrong side of our global and domestic #GrowthSlowing call. Case in point: Right now, the most contrarian long position in Macro is long Treasuries. Yes, you read that right. According to CFTC Futures and Options data, Wall Street is net short the 2-year Treasury by -421,551 contracts (registering -2.1x on a 1-year Z-score basis). What rallies when global and domestic growth slows? Treasury bonds. With so many taking the other side of that trade and growth continuing to slow, we are sticking with that contrarian call here. |

Draghi & #EuropeSlowing

|

Draghi stuck the dovishly-hawkish dismount last week, formally announcing the cessation of QE while simultaneously downgrading the outlook and clarifying forward guidance around asset reinvestment. Draghi, of course, knows that he’s tightening into a slowdown here with the downgrading of the outlook another tacit admission. All of this remains predictable theatrics against the backdrop of #TheCycle where Europe Slowing remains ongoing …. A reality re-confirmed again this morning with French PMI’s slipping into contraction and German PMI’s falling again sequentially, marking lower multi-year lows in activity across the biggest Eurozone economies. Benchmark Equities and the Euro are closing the week lower and remain Bearish Trend @Hedgeye. |

China Still Slowing

|

The gravity of #TheCycle continues to manifest in Asian high frequency macro data. In the wake of this weekend’s trade data which saw China report a -1010 bps deceleration in Export growth – down to 5.4% YoY in NOV and marking the lowest pace of growth since AUG ’17 - China Retail Sales growth decelerated -50 bps to +8.1% Y/Y, marking the slowest pace of growth in 14.5 years. It was the same story across the manufacturing economy as Industrial Production growth slowed -50bps to +5.4% Y/Y – good for a 10Y rate-of-change low. The 3-month auto tariff détente is the Tourist destination of the day, the cycle remains both the tree and the forest. |