NEWSWIRE: 11/12/18

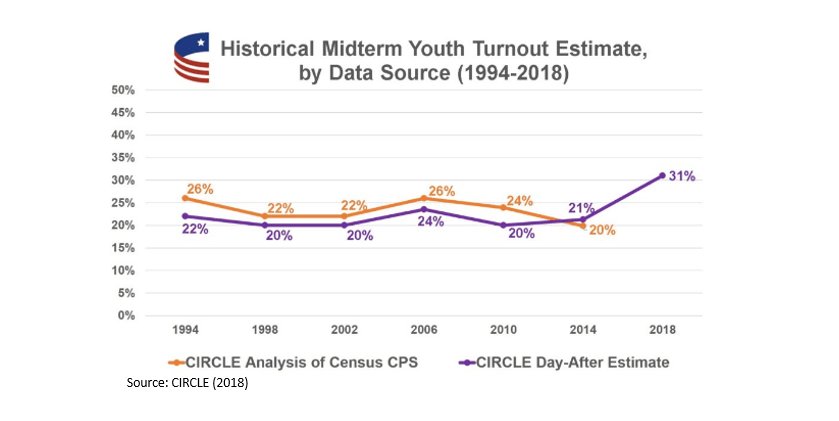

- At 31%, turnout among youth (ages 18 to 29) in the 2018 midterms was the highest it’s been for any midterm election in the past 25 years. The civic engagement and enthusiasm Millennials displayed in the Obama era has come roaring back as even stronger resistance, with young voters supporting Democratic House candidates by a historic 2-to-1 margin (67% Democrats vs. 32% Republicans). (CIRCLE)

- NH: The youth voting rate in 2018 may have been historic. According to our early read, it was certainly the highest youth voting rate in any midterm since the big "Watergate" drop-off in youth voting in 1974. And it may even be higher than the youth rate in 1966 and 1970--back before young late-wave Boomers just "gave up on the system, man." We'll have to wait a few months to get the official Census participation rate numbers to find out. (Census has no comparable age data before 1964.) From 2014 to 2018, according to CIRCLE, the rate jumped by an amazing 48%, from 21% to 31%.

- As for party preference, this was the 2008 Obama election all over again--with a sweeping 2-to-1 margin for the Democrats, though this time without any national figure at the top of the ticket. The gap in age-bracket preference was equally impressive. In 2008, the under-30s' share for Obama was 21 percentage points higher than the over-65s' share. In 2018 (see the Washington Post graph below), the numbers were similar--and the youth-senior age gap was 20 percentage points. We're talking about the largest age gaps ever measured--for any national election for which we have good age data (that is, since the early 1960s). By comparison, the Nixon versus McGovern age gap in 1972 was "only" 16 percentage points.

- This youth crescendo could have inundated the GOP last week with a much larger blue wave had it not been for one other fact: There was also a big surge in the turnout for every older age bracket. Nationally, the voting rate climbed from 37% in 2014 to an estimated 49% in 2018--not as big as the youth surge but substantial nonetheless. Measured as a share of the population, it may turn out to be the highest total midterm voting rate since 1970. Measured as a share of eligible voters, it may be the highest in over a century. Say what you want about Donald Trump, but he has succeeded in reversing several decades of growing voter apathy by fanning "populist" intensity among all age brackets, income groups, and regions. The 2018 story is not voter suppression, but more like voter aggression. It's as if we all cared again about which direction our national ship of state is heading--and about who is at the tiller.

- A new WSJ exposé discusses “customer lifetime value” (CLV), a secret score that U.S. retailers use to rank their customers. This covert practice, which rewards the most valuable shoppers with everything from better customer service to exclusive perks and discounts, bears an unsettling resemblance to China’s social credit system. (The Wall Street Journal)

- NH: Don't know your CLV? Take this quiz to calculate its likely value. Some of these factors seem pretty obvious. For instance, being higher income or married will increase your CLV--just as it would on a credit score. On the other hand, being younger will also increase it--since you have more years of purchasing ahead of you. A bit more obscure are telltale signs that you love searching for bargains (lower score: reduces likely price margin); like to buy lots of things all at once (higher score: raises likely price margin); tend to complain or return items (lower score: raises service cost); or are a strong "influencer" (raises score: brings in new business). Perversely, too much brand loyalty can actually lower your score since the retailer will see no need to offer you a discount. Deliberately switching brands from time to time and leaving Web clues that you do some comparison shopping (even if you don't) is absolutely a smart plan.

- No, this isn't China's social credit system: The state is not compelling you to transact with these "profiling" retailers. Still, retailers should be advised. With all of these personalized tactics, each retailer alone may think it is cleverly scooping a bit more revenue out from under every consumer's demand curve. But as a group, the retailers' growing abuse of customer trust is likely to trigger an aggressive and (inevitably) ham-fisted regulatory response. “Not all customers deserve a company’s best efforts,” explains Peter Fader, the Wharton whiz kid who helped popularize the CLV. That says it all. And similarly, not all companies deserve much customer sympathy when voters are deliberating over the merits of, say, Elizabeth Warren in 2020.

- Senior housing developments are sitting empty as more Boomers and Silent age in place. Hopeful developers and investors insist the oversupply won’t last as more Boomers retire and need care, but they won’t be able to convince the many members of this generation who just don’t want to live there. (The Wall Street Journal)

- NH: A "severe supply problem," in the real estate business, is a euphemism for plunging occupancy rates. Please. I've been warning investors endlessly about these active adult communities. (See: "The Aging of Aquarius.") The Greatest Generation (G.I.s) loved them. The Greatest Generation's children (Boomers) do not. Aging Boomers don't especially want to live near each other. They want to be with or near their children. A growing share of them are still employed past age 65. Those who have money tend to be in the best health, and see no reason to move into the luxurious assisted-living quarters being designed for them. And, with each passing birth cohort reaching 65, their net worth is declining. Too many investors refuse to think generationally. They simply see a rise in age-bracket numbers and brainlessly pull the trigger--as if all these septuagenarian hippies and yuppies just can't wait to play bingo in Leisure World.

- When asked “Is this generation misunderstood?”, high school teachers around the country had mostly warm, complimentary words for their students. The descriptions offer a portrait of young people who are, by turns, accepting, anxious, creative, empathetic, and optimistic—much more, in other words, than the stereotype of narcissists glued to their phones. (The New York Times)

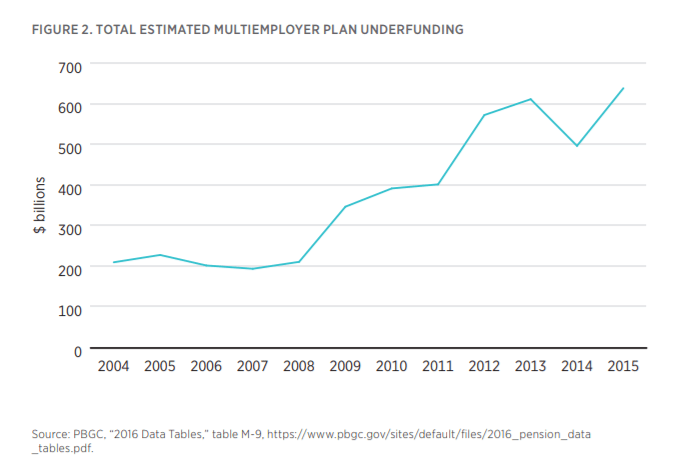

- New estimates show that the federally chartered U.S. multiemployer pension insurance system is on track to be insolvent by 2025. While much attention has been paid to the severe shortfall faced by many state plans, a similar crisis is happening in multiemployer plans, which are now paying the price for setting wildly optimistic discount rates that understated their true liabilities. (Economics21)

- NH: If you want an object lesson in myopic, can-kicking government dysfunction, just read this report and weep. Multiemployer pension funds, a monstrous "pooled" creation of unions and many employers, were never intended to be solvent. From the very beginning, they were able--like state and local plans (see: "Why Are Public Pensions So Messed Up?")--to choose whatever discount rate they found convenient (the higher the better, boys!). What's more, member firms were allowed to drop out of these plans without paying anywhere near the cost of their remaining liabilities. This created a free-rider incentive to quit and hurried the financial unraveling of these funds. Sure, the Great Recession and the subpar recovery of construction added to the burden. But these plans were never as healthy as single-employer plans.

- Some Democrats are backing measures (like the proposed Butch Lewis Act) that would bail out these plans, and the PBGC, by issuing low-interest Treasury debt. Thus are the majority of taxpayers, who do not have DB plans, supposed to shore up the benefits of an aging cadre of workers who do while letting the companies and unions off the hook. Hey, if the U.S. Treasury has access to free money, why not spread it around to all of us?

- Mom blogger Karen Johnson sticks up for Millennial dads everywhere. Johnson points out that today’s young dads—competent, hands-on, and load-sharing—in no way resemble the pervasive “dumb dad” stereotype that may have fit earlier generations of dads. (Scary Mommy)

- NH: The rehabilitation of dads actually started with Gen Xers. (See: "The Dawn of 'Dadvertising.'")

- Millennials are more likely than any other generation to engage in various healthy financial practices, such as sticking to a budget and cutting back on discretionary spending. The financial services industry should be scrambling to get these risk-averse young savers in the door—especially considering that just a small share of Millennials currently work with a financial adviser. (Society of Actuaries)

- Only 31% of Gen Xers say they love their homeowners’ association, compared to 39% of Millennials and 52% of Boomers. For Xers, HOAs are a source of mixed feelings: They need them to make sure their neighbors behave, but also wish they would leave their own houses alone and let them live how they want. (The Washington Post)

- NH: Gen Xers, who tend to favor a libertarian, live-and-let-live ethos, loathe the argumentative and dictatorial Boomers who currently dominate HOA boards. Many Gen Xers never cared much about the whole Boomer lifestyle "image" when they first moved in. They just wanted a safe neighborhood with good schools. And they cared even less when they got to know their neighbors. Gen Xers are not only 21 percentage points less likely than Boomers to "love" their HOA. They are also 15 percentage points more likely to "hate" it. Some of these stories will make you shake your head--like the veteran who lost his life savings in legal fees trying to safeguard his right to show a 17-inch American flag next to his front door.

- U.S. adults ages 22 to 39 report the highest average stress levels of any age group. When it comes to the impact of stress, however, the youngest Americans take the lead: More than one-quarter of 15- to 21-year-olds (27%) rate their mental health as fair or poor, by far the highest share of any age group. (American Psychological Society)

- NH: This report leaves much to be desired. While this is the 12th APS report in a row on stress, there are no age-bracket comparisons over time. Nor is there any discussion about expected phase-of-life differences in stress. Nor, indeed, does the report ask whether some stress is normal and healthy. The tone is uniformly therapeutic and maternal, as one might expect from an organization full of empathic clinicians. It is nonetheless interesting how often teens and young adults talk about "stress" in entirely passive terms--as though they had little agency to do much about it. Many of these youth find the state of the nation especially "stressful." The recent midterm turnout reveals that, here at least, they may be discovering a sense of agency after all.

- Labor force participation for 25- to 34-year-old men is still 3 percentage points lower than it was in 2007, the largest shortfall of any adult age-and-sex bracket. Lingering amid the backdrop of a strengthening economy as measured by job creation and employment, this persistent shortfall could have the effect of creating a “lost generation” of workers. (Bloomberg Business)

- NH: There are only three age-sex groups in which employment rates lag significantly (by more then one percentage point) below where they were in 2007. These are age 15-24 among men and women. And age 25-34 among men only. (Women age 25-34 are well above their 2007 high-water mark.) The shortfall among teens and college-age youth is pretty well understood: Teen employment is falling out of favor with parents and teachers; college enrollment rates continue to rise; retail (a major youth employer) is on the ropes; and higher minimum wage laws are making many employers give up on kids.

- The shortfall among older males is more mysterious. We do know a larger share of these young men are living with their parents (a new social safety net of sorts) and going to school. And with Millennials increasingly avoiding marriage and kids until they achieve financial security, many noncollege men may assume that the very possibility of marriage is out of reach. The same young males who, in past decades, would be socialized in their mid-20s by early marriages are today getting by with their parents and friends. And that type of socialization--aka "adulting" in Millennial-speak--often doesn't require a job.

DID YOU KNOW?

Robo-Advising Goes Green. We’ve discussed before how the financial industry has been rolling out low-cost robo-advisory services in an attempt to win over Millennial investors. (See: “The Future of Investing.”) Now, some firms are giving these services another Millennial-friendly twist: sustainability. Enter Newday Impact Investing, a startup backed by the likes of BlackRock that claims to be the first firm to offer “fully automated wealth management solutions for impact and socially responsible investing.” (To be sure, other firms like Robinhood and Aspiration are also experimenting with similar services.) In Millennials, Newday sees a generation that cares more about how they invest than how much they invest. Morgan Stanley research has found that 22 percent of Millennials say they are likely to invest in companies that target specific social or environmental goals, compared to just 12 percent of all investors. Furthermore, Millennials are more than twice as likely as other investors to say they would exit an investment position because of objectionable activity on the part of the firm (15 percent, versus 7 percent of all investors).