Editor's Note: Below is a brief excerpt from Market Edges, our weekly newsletter of investable macro insights. Click here to learn more about Market Edges.

|

"If you watch mainstream TV, everything is always all about Trump and the “Trade War”… but how helpful has that Macro Tourism been to improving your returns or process in 2018? Measuring and mapping the economic cycle in rate of change terms? Now that’s the stuff of championship alpha this year." |

If you've been following our current market call you already know we're calling for U.S. growth to slow in 4Q 2018. We're seeing "less good" data across much of the high-frequency economic indicators we track. Just look at third quarter earnings...

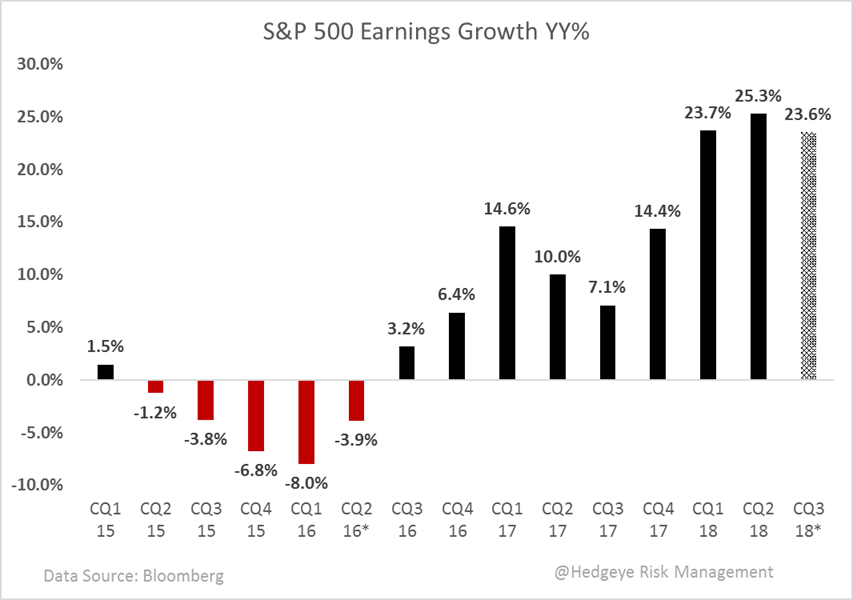

We're two-thirds of the way through earnings season and here's the update so far: 328 of 500 companies having reported, sales & earnings growth for S&P 500 companies in aggregate is tracking +8.0% & +23.6% year-over-year.

Some conclude earnings growth is "good" and corporates are "resilient". We would say that those Q3 line items are rate-of-change slowdowns from Q2 if earnings season ended today. We're confident that debate and its implications will continue indefinitely...

From an expectations standpoint we know that a wall of steepening base effects has taken out-quarter expectations lower. As of now, the aggregate Q4 consensus Bloomberg estimate for YY sales & earnings growth for S&P 500 constituents is ~6% & ~17% year-over-year.

- Should Q3 end here, the conclusion is a "top-line growth slowdown"

- Should Q3 end here, the conclusion is an "earnings growth slowdown"

Q2 of 2018 marked the 8th consecutive quarter of GDP growth, Earnings Growth and Margin expansion and ended with the steepest top-line rate of growth for S&P 500 companies (+9.4% year-over-year) since Q3 of 2011 and the steepest bottom line rate of growth (+25.3% year-over-year) since Q3 of 2010.