Below are analyst updates on our fourteen current high-conviction long and short ideas. We will send a separate email with Hedgeye CEO Keith McCullough's refreshed levels for each ticker.

IDEAS UPDATES

CACC

Click here to read our analyst's original report.

Credit Acceptance Corp (CACC) increased its salesforce 31% from 2Q16 through 3Q17. Looking back historically at prior periods when the salesforce grew materially we find that the growth in both the dealer base and the unit volume was equal to or greater than the growth in the salesforce on a 1- 2 year lag. Consequently, we expect to see 30+% growth in dealers & units over the 2018- 2020 period. This assumption is reflected in our forward earnings estimates.

STAY

Click here to read our analyst's original report.

Extended Stay America (STAY) | JOLTS DATA IMPLYING STEADY GROWTH THROUGH 1Q 2019

Our preferred forward looking tool for STAY – the US Total Job Openings data – points to RevPAR upside for the next 3 quarters. We’ve found that this dataset correlates on a lead more highly with STAY’s RevPAR than any other hotel company (and it’s statistically significant). The JOLTS data implies RevPAR growth closer to 3%+ for 4Q18 and 1Q19, but we are modeling closer to 50-100bps of renovation disruption in the Q’s. STAY’s shaky 2Q18 print confirms the notion that this is very much a “prove it to me” story and they’ll need to be more consistent around the quarterly prints. That said, given the very robust drivers in their niche lodging segment (low cost, extended stay), a management team dedicated to capital return, and early successes in capital recycling and refranchising, we remain bullish on STAY’s future and on the stock.

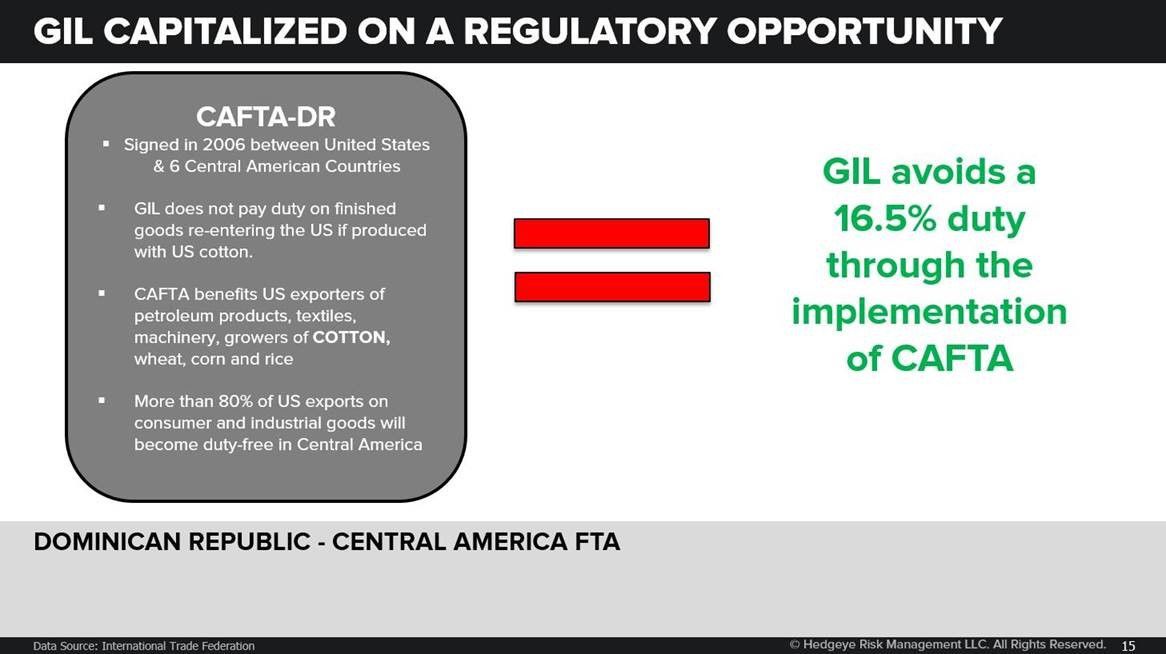

GIL

Click here to read our analyst's original report.

There are several factors behind Gildan Activewear's (GIL) low cost advantage. The earliest advantage came from the passage of CAFTA in 2006. Under the Central American Free Trade Agreement with six Central American countries the US permits the importation of textiles without a 16.5% duty as long as US cotton is used. Gildan was one of the first companies to move production to Honduras to take advantage of its duty free status and lower shipping costs compared to Asian countries and lower wages compared to North America. The Trump administration has not mentioned the repeal of CAFTA, because the US has a trade surplus with the six countries.

CMG

Click here to read our analyst's original report.

There may be some short-term bumps in store for Chipotle Mexican Grill (CMG) – but there is significant upside beyond that according to veteran Hedgeye Restaurants analyst Howard Penney.

After (correctly) being one of the company’s biggest bears, Penney has become one of its most vocal bulls. His analyst team is very bullish on Chipotle over the longer term and believes it could have enormous upside for the stock in two to three years.

That said, the next couple of quarters could be rocky as the once-beleaguered burrito chain travels Redemption Road to that lofty number.

“I think the rubber meets the road from [Chipotle CEO Brian Niccol’s] pass that he’s getting to a certain degree because there hasn’t been any substantial improvement in the operating performance of the company,” Penney explains in the video below.

“And I think that’s really going to boil down to fiscal ’19 guidance. There is a recovery in place, but the question then becomes, ‘How big is the recovery?’”

If Penney’s call is correct, that recovery could be very big.

After the company’s health scandals, many in the industry wondered which restaurant chain would become the next Chipotle. As Penney declared in a recent institutional client call, “Chipotle is the next Chipotle.”

MD

Click here to read our analyst's original report.

Mednax (MD) EBITDA guidance was on the surface disappointing, which calls for a decline of -3% to -8% year over year, however, adjusting the prior year for a +$5.5M EBITDA contribution from Southeast and the carrying cost of these physicians of $10M in 3Q18, the more accurate comparison shows EBITDA growth of +3% to +8% in 3Q18. Data shows reported group practice member counts at Southeast have fallen from 116 as of March 2018 to 110 as of August 2018. As the company outlined, $10M in costs per quarter in the second half of 2018 are associated with these clinicians, although if the company helps these physicians move on more rapidly, there should be upside to results.

There were a number of questions focused on company guidance 3Q18 and beyond as it relates to carrying cost of Southeast and cost initiatives. The line of questioning took the position that while cutting G&A is concrete and believable, medical practice costs and margin improvement was less believable.

ZBH

Click here to read our analyst's original report.

Long Zimmer Biomet (ZBH) is all about getting their supply back online and we are incrementally more confident in the trade after doing additional field work and hearing management from both companies present at an industry conference yesterday.

Management sounded optimistic about their turnaround with positive momentum heading into 2H18 and seem to be setting expectations appropriately. Margin guidance for 2019 is likely conservative given CEO Bryan Hanson’s commentary "If you are looking for a drop in gross margins again in 2019 it is not going to happen."

In addition, we recently updated our ZBH pricing tracker which continues to show stabilization through 3Q18.

TPR

Click here to read our analyst's original report.

Beginning on Monday handbags imported from China will incur a 10% tariff. By year end the tariff will increase to 25%.

Coach began diversifying its manufacturing away from China more than a decade ago. The replacement process can take several years especially with higher quality and labor intensive products.

Today less than 5% of Tapestry's (TPR)Tapestry’s products are manufactured in China.

China is much more important as an end market to Tapestry than a manufacturing base. The Coach brand has about $600M in revenue in China, up from $50M six years ago. One of the first actions Tapestry took with its Kate Spade acquisition is to acquire its license partner in China. Kate Spade was losing money on $50M in revenues in China prior to the acquisition. Tapestry will leverage its local management team and their relationships to quickly accelerate Kate Spade’s growth in the region. That is why Tapestry has said one of the biggest opportunities for the Kate Spade brand is China.

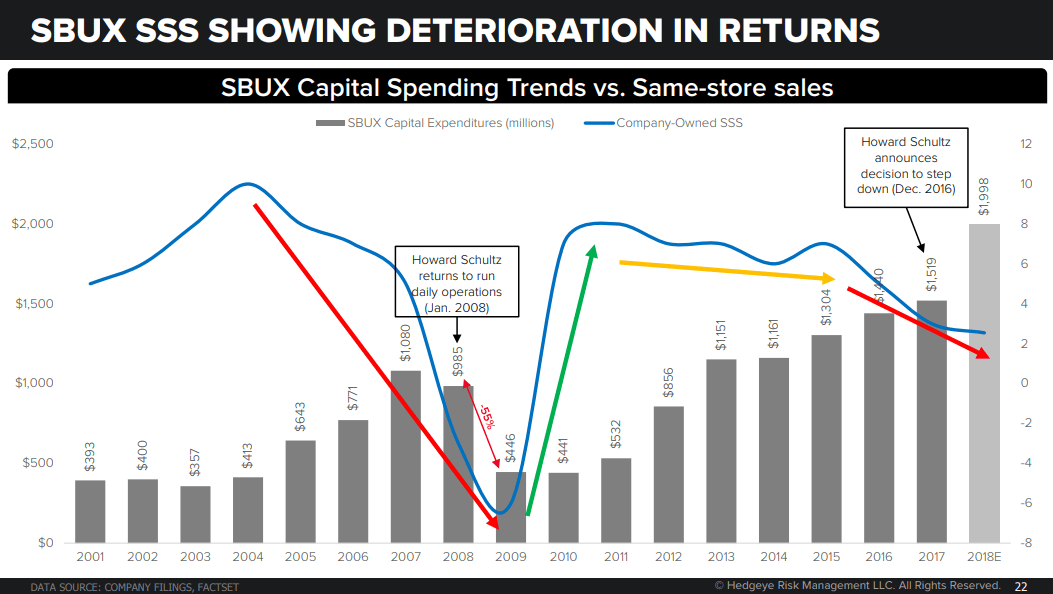

SBUX

Click here to read our analyst's original report.

Below is analysis from Restaurants analyst Howard Penney discussing his short Starbucks (SBUX) thesis:

Complexity is clearly a theme of mine and I’m going to stick with that here talking about Starbucks (SBUX). On slide 19, you see the Starbucks American same-store sales and you see sales in the 1Q 2016 posting 9% growth and 1% growth by 3Q 2018.

This is another complexity story as their ticket times have gone down. They’re serving food and trying to sell more to consumers. If you look at the menu trends. Total menu items are up a lot. If you look at menu trends and correlate that with sales and promotions, when menu items go up sales go down.

Now this is my Howard Schultz slide, where he came back when Starbucks was struggling after he left. The company cut capital spending because they were growing too fast. And then he left at the peak of capital spending again as sales were slowing. So now once again he’s left the ship drifting along with a CEO who doesn’t look like he’s ready to take the right steps to fix the sales trend.

CCL

Click here to read our analyst's original report.

Cruise investor sentiment has improved dramatically recently. We attribute the optimism to a lack of Caribbean hurricane activity, improved US consumer sentiment, a less strong dollar, and some funds rotating out of the G and L of the GLL sector. With the improved sentiment, Carnival (CCL) is testing the high end of its PE valuation range in yield decelerating environments of 10-14x. Yet, while early, CCL seems to be lagging its peers in terms of 2019 pricing.

As for Q3, we expect a smaller yield beat than that seen in 1H 2018 given little close-in lift in Q3 Caribbean pricing but better pricing from Europe. CCL could raise FY 2018 yield guidance to ~3.5% from ~3.0% but this still represents a deceleration from 2017’s 4.5%. CCL maintains the largest exposure to Europe in Q3 with 40% of its capacity there. We believe management will comment on the calmer hurricane season which should increase their confidence in the Caribbean’s performance heading into 2019.

In fact, Caribbean pricing for the next 12 months jumped over the Labor Day weekend promo period. However, it may be difficult to obtain a good read this early considering any supply impact on pricing probably won’t be gleaned until Wave. Early data does however suggest that CCL’s Caribbean pricing for 2019 is lagging behind its peers.

UNFI

Click here to read our analyst's original report.

As we’ve been explaining in recent editions of Investing Ideas, United Natural Foods' (UNFI) agreement to acquire SUPERVALU (SVU) is troubling from a number of different perspectives.

How do you make a low and declining margin distribution business even worse? Buy an even lower margin distribution business strangled by debt, mounting pension liabilities, and add in a small dying retail presence!

Given the strength of larger competitors in food retail and the investments in e-commerce that have been made, we feel that the under-invested in brands that SVU has will be difficult to sell. Furthermore, the retail assets could become a cash drain for the broader UNFI organization over time as they require capex of 1.25% to 1.75% of retail sales, whereas UNFI has been run-rating around 0.6% to 0.7% of sales.

ALRM

Click here to read our analyst's original report.

Alarm.com (ALRM) sits in the eye of market disruption as its leading position in interactive home security systems faces a torrent of new digital systems with innovative business models, customer acquisition, and technology. Meanwhile, the market opportunity for ALRM has exploded in the last few years, but ALRM has not. The stock is expensive on FCF…and OCF/EBITDA improvements in 2017 were mainly inorganic and not repeatable.

SGRY

Click here to read our analyst's original report.

While Surgery Partners (SGRY) revenue recently came in $15.9M ahead of expectations, adjusted EBITDA of $55.4M (which is manufactured) only beat expectations by $1.4M. Meanwhile, free cash flow to common equity holders continues to run negative at -$3M in 2Q18. SGRY's adjusted EBITDA margin of 12.5% declined 40bps YoY, as management continues to invest to "drive organic growth" in 2019. With adjusted EBITDA margins declining 154bps in 1H18, we continue to have a hard time getting to the ~150bps of 2H18 margin expansion needed to hit the 2018 consensus EBITDA estimate of $243.8M. Note management's 2018 guidance of at least $240M was before the impact of acquisitions, and we are modeling $234M including acquisitions and assuming COGS only increase 2% 2H18/1H18. Management's reluctance to quantify the cost savings from the new GPO contract during the earnings call, and commentary that their EBITDA guidance is "heavily weighted towards the fourth quarter," reinforces our view that 2H18 EBITDA estimates are at-risk.

TSLA

Click here to read our analyst's original stock report.

Our data are showing a clear deterioration in the Tesla (TSLA) brand, a potentially lethal development for many institutional long investment theses. Delivery, quality, and service issues for Tesla vehicles have likely negatively impacted demand, while management departures, Musk’s problematic behavior, and SEC/DOJ investigations add to the negative attention. While we continue to look to short squeezes, the local highs may trend lower into our 1H19 catalyst period.

SHAK

Click here to read our analyst's original Shake Shack report.

Black Box and Knapp-Track same restaurant sales (SRS) and traffic (SRT) took a turn for the worse against some of the easiest comparisons in recent history.

Black Box SRS for July was 0.54%, representing a 120bps sequential decline in the 2-year average to -1.1%. SRT for July was -1.8%, representing a 90bps sequential decline in the 2-year average to -3.2%.

The continued negative traffic trends speak to broader problems the restaurant industry faces with being overstored, which is not a new trend. Hence our dislike for restaurant companies with negative traffic and high unit growth rates (Shake Shack [SHAK]), it’s not a sustainable allocation of capital!