“Being Still and Doing Nothing Are Two Completely Different Things”

-Jackie Chan

My typical macro (news) “flow” the past couple days has been commandeered by reminisces and peri-crisis retrospectives on Lehman Brothers and the GFC.

Outside of a humanist appreciation for the magnitude of lost income and opportunity, my retrospective has a somewhat more sanguine shading.

Hedgeye was, after all, birthed from the creative destruction of the financial crisis and the implosion of antiquated, institutionalized, and levered Wall Street and Ivory Tower conventions.

Keith matter-of-factly highlighted his 2007 firing in a recent Early Look, but in case you failed to read the subtlety between the lines there – he got fired in October 2007 for starting to get too bearish.

He would say being early = being wrong. That’s true … but not really.

KM, I and pretty much the whole early team @Hedgeye would go on to work largely for free over the next couple years, moving upstream amidst an industry in acute cyclical and structural contraction.

That’s not meant as a kind of holier-than-thou anecdote. It’s simply to say, Hedgeye was built more from blue-collar grind than white collar privilege. And building something from the ground-up is the only way to know how strong the foundation is.

Transparency, Accountability, & Trust represent the ethos and foundational trinity upon which this real-time experiment in information democratization and analytical evolution rest.

No pseudonyms, no conflicts of interest, no complacency (… and no, not perfect either).

We said that won’t change and we won’t change what we said.

Back to the Global Macro Grind...

So, Chinese Fixed Asset Investment growth printed a 19-year low, negative Retail Sales growth in Brazil offered negative respite for the beleaguered Real, the Argentine Peso continued to pike lower as CPI growth there breached 34% to the upside and Team Draghi acknowledged the 2nd derivative reality of Eurozone Growth by downgrading the official growth outlook … on a 3 quarter lag.

The OUS (Ex-US) knife catching cabaret remains open for (macro) tourism.

Stateside, benchmark indices advanced, again flirting with new ATH’s as the Treasury showed the FY deficit rising +34.9% Y/Y to $898B in the 11-months through August led by a -$71B decline in Corporate Income Tax receipts.

Unprecedented late-cycle, debt-funded stimulus driving unprecedented divergences in growth, equity performance and corporate profits. #AmericanExceptionalism is the current, euphemistic macro meme of choice for that dynamic.

Elsewhere, domestically, the probable Jun-Aug cycle peak in Inflation we’ve been harping on for like 6+ months found some confirmation as CPI slowed conspicuously and component breadth turned negative.

- Headline CPI = decelerating a full -25bps to +2.7% Y/Y, pivoting off the 80-month high recorded in July

- Core CPI = decelerating -15bps to +2.2% Y/Y

- Shelter, Medical, Energy, Apparel, Wireless = all key consumer cost centers, all decelerating sequentially

- Median & Trimmed Mean CPI (alternate inflation measures calculated by the Cleveland Fed and meant to better capture underlying price trends) = both decelerated sequentially on a year-over-year basis.

- Sticky & Core Sticky CPI (another alternate measure which tracks a selected basket of goods and services where price changes evolve more slowly) = both decelerated sequentially on a year-over-year basis.

Could late-cycle demand-supply imbalance combine with tariff related cost-push inflation ($500B in Tariffs on Chinese Imports with significant exposure to consumer goods) to make the latest disinflationary impulse somewhat transient?

Sure, but that’s not our baseline expectation currently. At least not on an investible 3-6 month duration.

And in the meantime: Nominal Wage Growth ↑ + Inflation Growth ↓ = Real Income Growth/Purchasing Power ↑

Any persistence in dynamic also equates to a higher share of national income going to labor which represents a potential profitability squeeze for corporate margins at peak and moving towards annualizing the tax reform benefit and impossibly steep growth comps.

Lower realized inflation and an ebbing in inflation expectations also support our outlook for lower-highs in bond yields and the gradual shift towards bond proxy exposure (Reits, Utes, etc).

Also, recall a derivative potentiality we’ve been stalking amidst our #Divergences theme:

Layering fiscal stimulus atop an already taut, late-cycle economy is anomalous and presents an interesting, somewhat anomalous potentiality as households could see improved consumption capacity at the same that both headline growth and inflation (domestically and globally) are slowing and yields are making lower highs. Coupled with further downside in the savings rate (post the wholesale NIPA revisions in July), improved real purchasing power could buoy the current consumption cycle a touch beyond what one might otherwise expect …. That (wild-card) potentiality is also why we haven’t gone explicitly negative on consumer discretionary yet

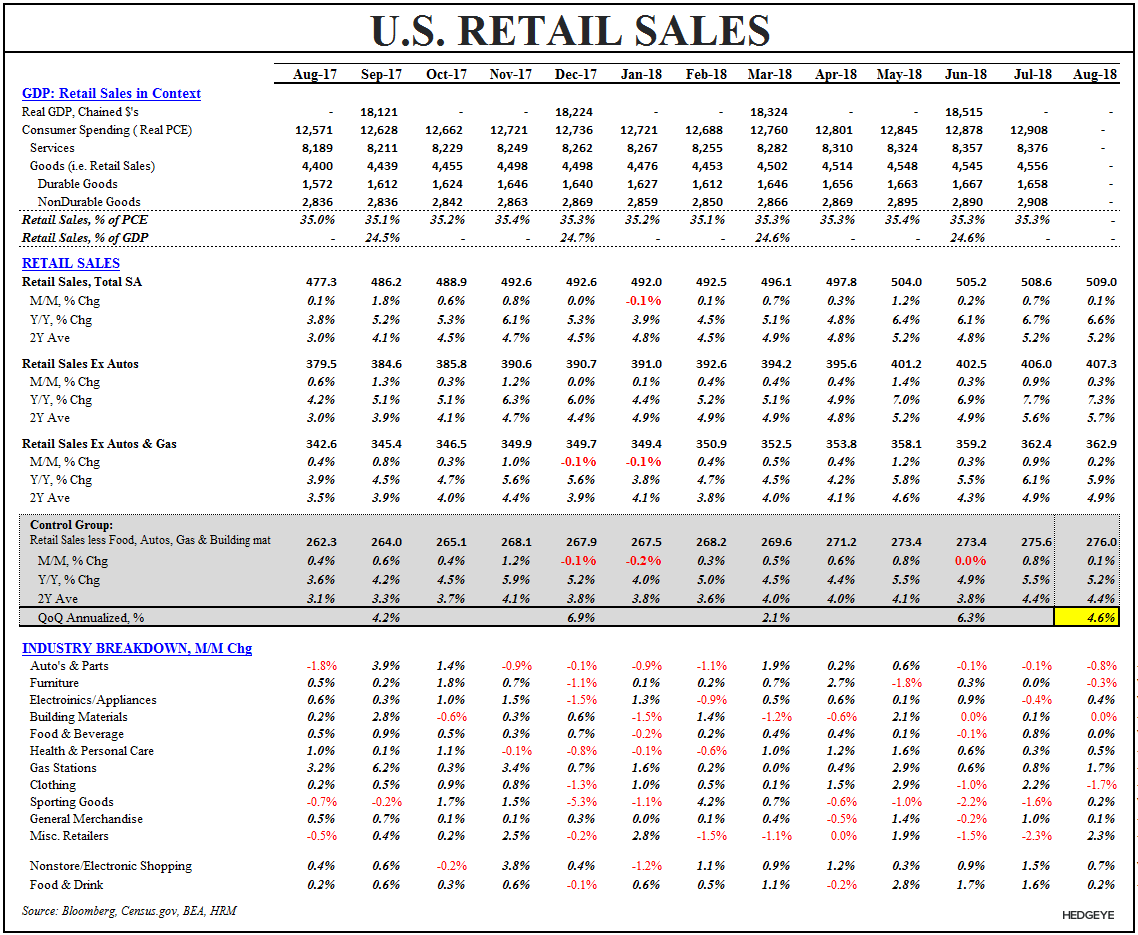

We got our first score on domestic consumerism this morning with August Retail Sales and, on balance, it accords with the cycle highs in wage growth and consumer and small business confidence reported over the past week.

Headline Retail Sales, Retail Sales ex-autos and Control Group Sales (GDP input) growth came in at +6.7% Y/Y, +7.3% Y/Y and +5.2% Y/Y, respectively, on the back of significant positive revisions to July estimates.

Juxtapose that with Eurozone Retail Sales at +1.1% Y/Y (as in O-N-E) and falling …. And which Draghi himself told you are probably headed further southward … particularly against the hardest comp in 3 years in September.

There’s not a lot of positive number space below 1 and valuation is still not a catalyst when causal fundamental factors are trending the wrong way.

Translating all that to allocation decisions: After doing not a lot in RTA the past few days, here’s how Keith led off the Top 3 Things this morning:

Post a 4-day bounce (ex-China), lots to do this morning in terms of macro re-positioning, gross and net …

- US DOLLAR – most of the moves I’d be making this morning are inversely correlating with USD which is signaling immediate-term #oversold within its $94.30-95.60 @Hedgeye Risk Range – shorting Euros, Pounds, and pretty much any EM currency whose country is in Quad 3 or 4; also a good spot to start re-shorting your fav Emerging Market Equity shorts

There’s a certain cadence and clustering to dynamic risk management. Being still and doing nothing are not the same thing.

And missing a beat (trade) is not the same as losing the rhythm (trend).

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND views in brackets) are now:

UST 10yr Yield 2.84-3.00% (neutral)

SPX 2 (bullish)

RUT 1 (bullish)

NASDAQ 7 (bullish)

Utilities (XLU) 53.23-55.03 (bullish)

REITS (VNQ) 82.62-84.40 (bullish)

Industrials (XLI) 76.08-78.90 (bearish)

Shanghai Comp 2 (bearish)

Nikkei 224 (bullish)

DAX 117 (bearish)

VIX 11.79-15.29 (bullish)

USD 94.30-95.60 (bullish)

EUR/USD 1.15-1.17 (bearish)

YEN 110.46-111.95 (bearish)

GBP/USD 1.28-1.31 (bearish)

Oil (WTI) 66.80-70.80 (neutral)

Nat Gas 2.70-2.91 (bearish)

Gold 1194-1213 (bearish)

Copper 2.56-2.71 (bearish)

Corn 3.49-3.63 (bearish)

AAPL 216.70-230.75 (bullish)

AMZN 1 (bullish)

FB 154-174 (bearish)

GOOGL 1150-1229 (bearish)

NFLX 334-378 (bearish)

TSLA 261-304 (bearish)

Bitcoin 5 (bearish)

Keep dancing out there,

Christian Drake

U.S. Macro Analyst