“Heading into tomorrow's US jobs report, I don't want to carry as much very short-term rate risk... Why? Simple answer: more late cycle US Wage Cycle inflation is probable and the market can easily react hawkish to that “news.””

That’s how we annotated covering TBT in RTA yesterday into today’s employment report.

Of course it’s disingenuous to claim I-told-you-so credit with respect to the acceleration and upside surprise in wage growth in August when, by self-admission, convictedly timing an exact print wherein some kind of conspicuous step-function increase in wage inflation will manifest is quixotic.

That said, we’ve been increasingly diligent in highlighting the rising probability for late-cycle wage inflation to (finally) begin percolating more discretely in recent months as the preponderance of high and lower frequency domestic labor data were signaling as much and as we (finally) transitioned through labor tightness levels historically associated with nonlinear changes in compensation growth.

An acceleration in domestic wage inflation holds all manner of consequential macro implications, not the least of which is further propagation of the prevailing growth and policy #Divergence dynamic and the attendant implications for the $USD, EM contagion risk and EBIT margin erosion domestically (see, for example, Jump Conditions In Wage Growth Are Right Around the Corner).

Here, suffice it to reiterate that layering fiscal stimulus atop an already taut, late-cycle economy is anomalous and presents an interesting, somewhat anomalous potentiality as households could see improved consumption capacity at the same that both headline growth and inflation (domestically and globally) are slowing and yields are making lower highs. Coupled with further downside in the savings rate (post the wholesale NIPA revisions in July), improved real purchasing power could buoy the current consumption cycle a touch beyond what one might otherwise expect.

That (wild-card) potentiality is also why we haven’t gone explicitly negative on consumer discretionary yet and also probably why the sector is going lonewolf today, flirting with positive performance in a decidedly red tape.

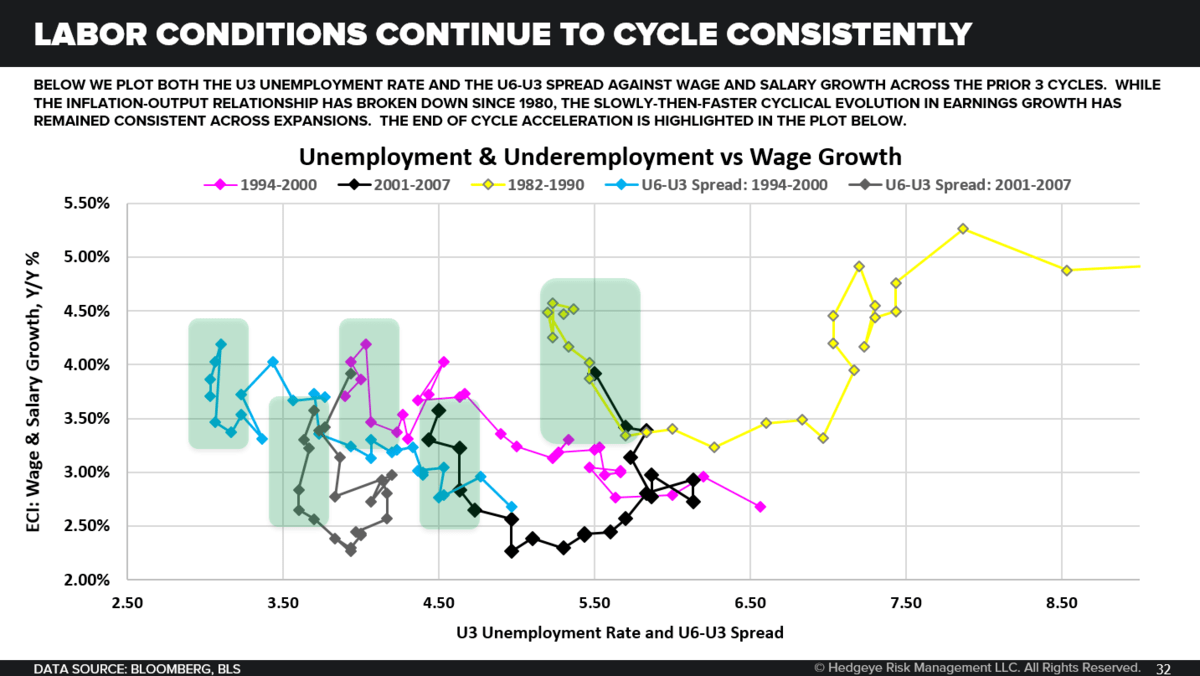

Anyway, the aim here on Friday afternoon isn’t for a macro analytical epiphany. It’s simply to provide a quick visual compendium of wage related indicators (to do the grind work for you). Again, one needn’t be a slope savant to discern and internalize the prevailing, collective 2nd derivative reality.

Indeed, this is what late-cycle labor and macro conditions are supposed to look like.

Have a great weekend,

Christian B. Drake

@HedgeyeUSA