“A rising tide lifts all boats…”

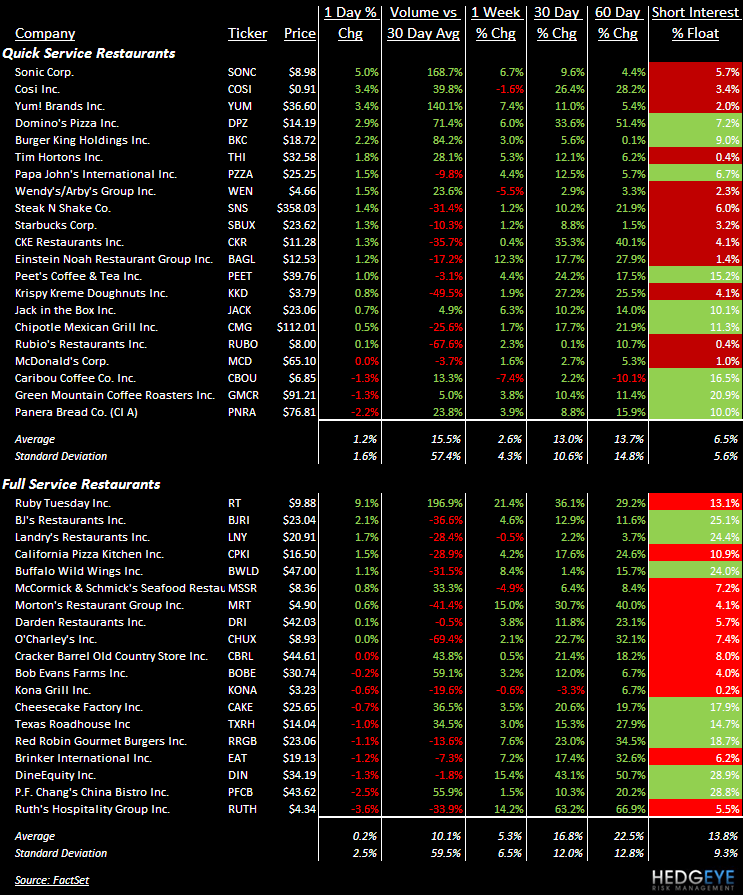

SONC was the best performing stock on big volume yesterday only because the “group” was rallying (SONC has significantly underperformed the QSR group over the last 6 months). Or maybe someone knew an analyst upgrade was coming this morning.

Today, we learned that SONC guides Q2 system-wide same-store sales to a decline of 12-14%. SONC attributed the decline to “unusually cold winter weather conditions combined with a decline in consumer spending in Sonic's core markets.” Same-store sales at partner drive-ins declined approximately 15% for the same period. There is no mention that management tried to gauge the consumer with aggressive pricing a few years ago and trends have never fully recovered since, particularly at partner drive-ins. Time for a management change?

BKC missed by a wide margin yesterday and it moved higher too.

Yesterday, YUM got a “vision” upgrade and a better multiple applied, in part to its US business. The issues that BKC and SONC are seeing are not limited to those concepts. YUM’s US business is one of the worst positioned of the large cap restaurant companies. Taco Bell is ok, but KFC and Pizza Hut are in secular decline.

On the full-service side, RT moved higher on better sales trends despite the weather. Although a nearly 10% move seems extreme, short covering was likely a significant factor. At 7.3x NTM EV/EBITDA, there does not appear to be much upside from these levels for RT.

Howard Penney

Managing Director