U.S. ECONOMY

- More US #GrowthSlowing data for Q3 > July US Architecture Billings Index (ABI) declines to 50.7 from 51.3 in June

- (Remember the July ISM's slowed in the US as well #data)

- UST 10yr Yield = 2.83%, down 7 basis points in the last month as the Long Bond and its proxies started to outperform

global markets

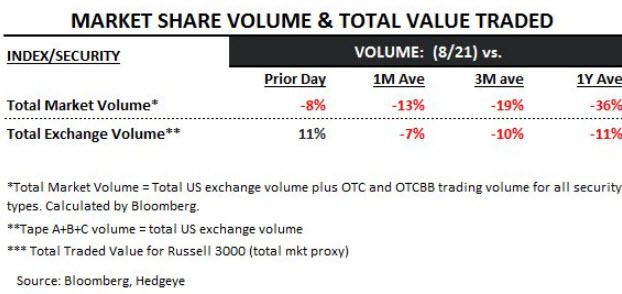

- VOLUME: continued to #decelerate during Day 4 of the US Equity rally

-

LONDON: stocks open up +0.4%, but the FTSE remains in the red for 2018 YTD as Global Growth slows

- GERMANY: having a tough time holding it's bounce to lower highs, DAX +0.08% remains Bearish TREND @Hedgeye

- BRAZIL: no mention by Old Wall Media yesterday, but both its stock market and currency resumed Bearish @Hedgeye TREND ... As the Brazilian 10yr Yield ripped to +12.36% (that's up +136 basis points, in the last month alone)

- JAPAN: Nikkei +0.6% overnight, closing just inside Hedgeye TREND resistance post SPY failing to making an all-time closing high

- CHINA: stocks fail to bounce beyond 2 days, resuming the #crash, down -0.7% overnight and -24% since JAN

commodities

- OIL: +1.3% on the bounce to for WTI but it remains Bearish TREND @Hedgeye as does our 3-6 month outlook on #InflationSlowing

- GOLD: +0.1% at $1196 with an immediate-term @Hedgeye Risk Range of $1170-1217/oz (remains Bearish TREND)

- COPPER: like Chinese Stocks, resuming its #crash this am, -0.6% to $2.69 = Bearish TREND @Hedgeye