The guest commentary below was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst.

Even as the Federal Open Market Committee raised short-term interest rates last week, the Trump Administration doubled down on trade war to gain leverage in the mid-term elections loom. The markets have not reacted well to the bellicose language coming from the White House, with financials in particularly under-performing the markets. But you don’t need to look very far to understand the travails affecting the US banking sector.

One reason why banks are selling off is the prospect of significant layoffs and operating losses in the mortgage sector. Rising costs and tight production spreads have driven the mortgage industry into the red this quarter, with many shops not even meeting minimum production levels to achieve break even. Rob Chrisman warned in his weekly comment that he expects to see at least one large bank shedding “thousands” of people this summer because of the combination of tight spreads and the over $8,000 per loan cost of new residential originations.

Another, more important reason for fading on the US large cap financials, particularly given the extraordinary run last year, is that the easy growth for the industry is at an end, both in terms of loans and deposits. We had a fascinating conversation last week with Lee Adler, proprietor of The Wall Street Examiner, about the “extinguishment” of reserves as the Fed’s Quantitative Easing treasure trove runs off. Adler contends that the runoff of QE means an end to the easy deposit growth seen by US banks over the past half decade.

“Under QE Fed lent money to Treasury in the form of note and bond purchases,” Adler explains. “By redeeming the notes and bonds as they mature, the Fed is effectively calling in those loans at the pace of $30 billion per month now, going to $40 billion in July, and 50 in October. Treasury pays the Fed off with cash it raises in additional note and bond sales. Investors bought the bonds with their bank deposits."

"Those deposits are extinguished when they are withdrawn from the investors' accounts, go into Treasury account, then from Treasury account to Fed to pay off the maturing paper," Adler continues. "The asset disappears from the Fed's balance sheet, and so does the bank reserve deposit because the bank's customer used it to buy the new bonds. The new bonds now exist, but the money used to purchase them was extinguished when the Treasury used it to pay off the Fed.”

“Deposit growth is slowly grinding to a halt, adds Adler. “It should go negative in the next couple months, especially if ECB makes more cuts in QE. Some of the ECB QE money was flowing instantly to US. Since ECB went from 60 to 30B QE their deposit growth has also slowed and less money flowed to US to buy bonds and stocks.”

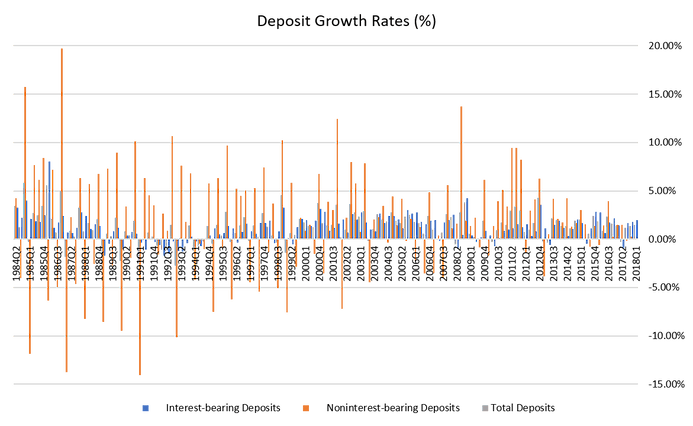

And sure enough, Alder’s prognosis is confirmed by the data from the FDIC, which shows that bank deposit growth has basically dropped to near zero over the past year. The chart below shows quarterly deposit growth rates going back to the mid-1980s. Notice that even during the years of aggressive Fed asset purchases, bank deposit growth rates were modest after the initial fear surge in non-interest bearing deposits after the 2008 debacle.

Of course, weak loan demand is another reason why deposit growth has been relatively restrained in this cycle. What demand has existed was focused on the hotter metro markets, which are starting to evidence late stage buyers fatigue. And as we’ve noted previously, bank regulators have been tapping the breaks on residential and multifamily credit for several years now. We also are reminded once again that there is no national market for residential real estate in the US. The folks at Weiss Analytics, in fact, confirm that with their latest data.

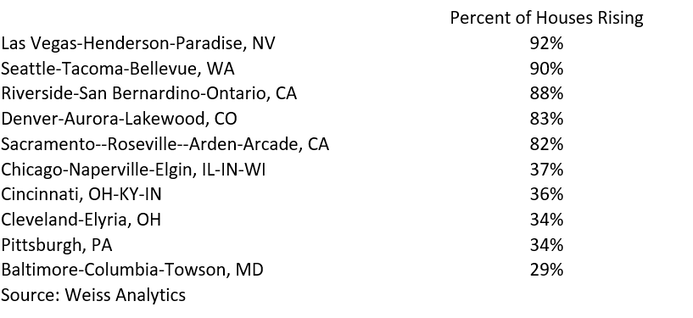

Weiss Analytics reports that red hot metros such as Las Vegas, Seattle-Tacoma and Denver-Aurora are starting to see a decline in the number of transactions with rising home prices. In 2015-2016, these markets were at one stage showing virtually all home sales with rising prices, a measure of the enormous asset price distortions caused by the FOMC in the real estate sector. Just by coincidence, credit costs of the decidedly prime residential loans owned by US banks bottomed in 2015.

Performance of first-lien mortgages remained unchanged during the first quarter of 2018 compared with a year earlier, according to the Office of the Comptroller of the Currency’s (OCC) quarterly report on mortgages. But what the data from Weiss Analytics suggest is that the heady sellers market of 2016 is rapidly changing two years later. The table below shows the percentage of sales in different markets where prices were rising.

If our colleagues at the Fed and OCC want a list of markets where banks are likely to face credit challenges in the next few years, they could do well to ponder the list above, which features some of the highest price volatility numbers of any residential asset markets in the US. And notice that the exurbs north of Washington DC are in a state of collapse, a sure sign that these recession proof venues are about to flop into a tenants market.

We’ll bet dinner at 21 Club that the loss given default (LGD) for these hyperbolic residential markets is close to zero or lower, as is the case currently with bank-owned multifamily exposures. With LGDs nationally for US bank owned residential exposures still in the 20% range vs the long-term average of 65%, it is pretty clear that credit costs in residential will rise in the future as the Fed continues to tighten credit and the US economy slows.

EDITOR'S NOTE

This Hedgeye Guest Contributor piece was written by Christopher Whalen, author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington. This piece does not necessarily reflect the opinion of Hedgeye.