Editor's Note: Below is a brief excerpt from a recent note written by veteran Retail analyst Brian McGough announcing his decision to move Nike (NKE) to his Best Idea list as a short. If you would like more information on his call (including access to his deep dive Nike Black Book call on May 23rd, please email sales@hedgeye.com).

I’m taking Nike to a Best Idea Short – for the first time in my 24-year career. I still think that the TAIL call (3 years or less) is one of the best in retail – but recognition of that will likely take an extra 1-2 years. I’m taking down numbers – potentially a quarter early – but think this is dead-money at best, and has 3-1 down/up.

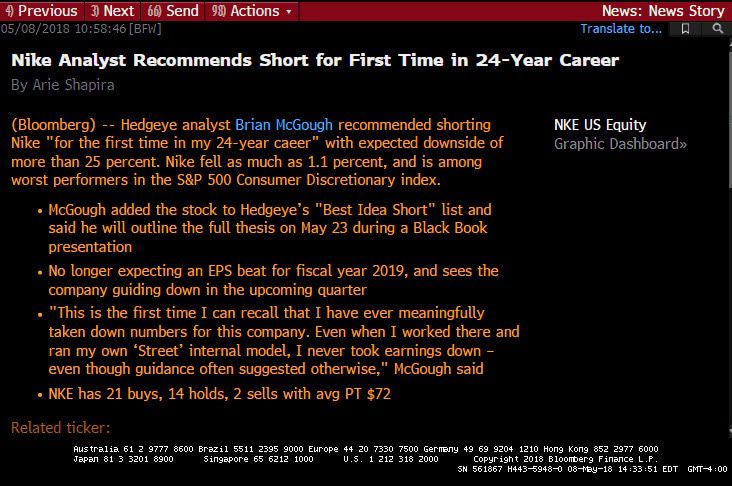

This is the first time I can recall that I have ever meaningfully taken down numbers for this company. Even when I worked there and ran my own ‘Street’ internal model, I never took earnings down – even though guidance often suggested otherwise.

I could be early, but with this name trading at an all time high, at 26x earnings and 19x EBITDA, a 2.5% FCF yield when it’s barely shorted (2% of the float) AND it’s getting ready to miss the consensus for only the second time in 13-years, I can get to far more downside than up. Would I like to short it with a $7-handle? Yes. But looking out over a 6-9 month horizon, I get to a bull case of $75, and bear case downside near $50. That’s down/up of 3 to 1.

In the end, to buy this today you have to believe the stock is going to $80+. Good luck with that. All in, I think it’s a low risk short, and dead money at best.

I’m hosting a Black Book on May 23rd – a week before quarter-end – to outline my full thesis. Mark your calendar.

-- McGough