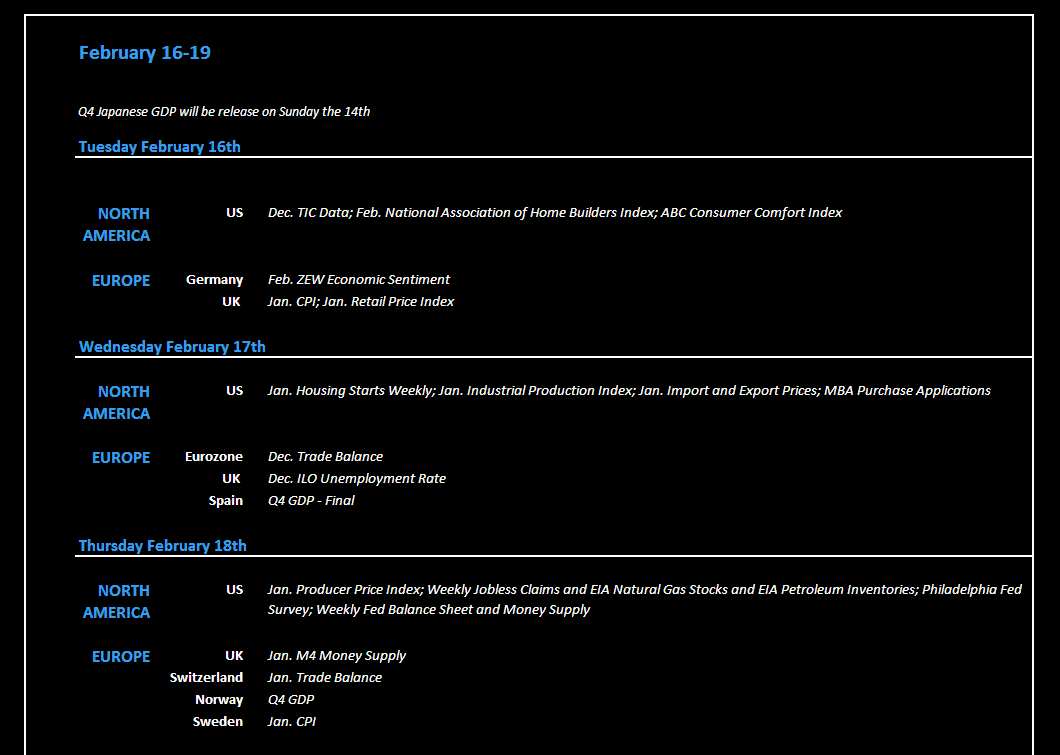

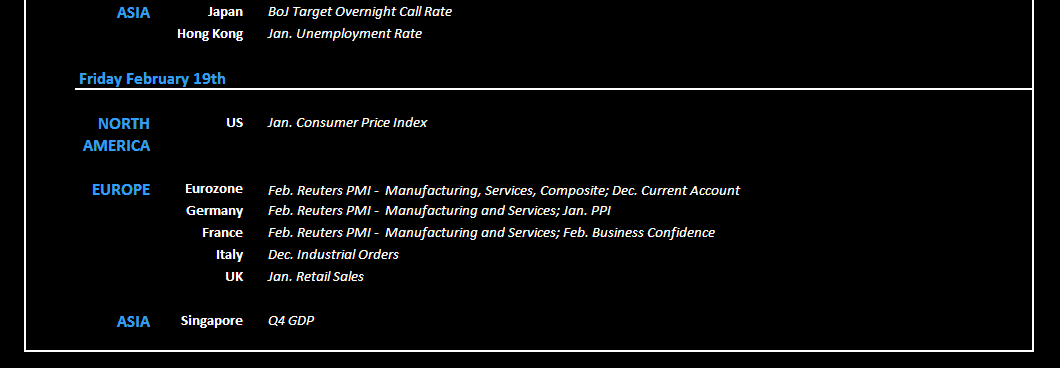

The Economic Data calendar for the shortened week of the 15th of February through the 19th is full of critical releases and events. This Sunday marks the beginning of the Chinese New Year; additionally many markets globally are closed Monday for holiday. Attached below is a snapshot of some (though far from all) of the headline numbers that we will be focused on.