Yesterday’s spectacular decline can be credited, in part, to the P.I.G.S. [Portugal, Ireland (or Italy or Iceland), Greece, and Spain] sovereign credit issues. The accompanying dollar strength is exacerbating the pressure on commodities and stocks leveraged to the RECOVERY trade - a different kind of SWINE FLU!

Since the March 9, 2009 low there have only been three other days that the S&P 500 market has fallen 3% or more: 3/30, 4/20 and 6/22. Yesterday’s 3.11% decline in the S&P 500 was a devastating blow to the internals of the market. Volume accelerated by 39% day-over-day and the Advance-Decline number was -2582; you need to go back to 3/5 to see a number that bad. Lastly, there are no sectors positive on TRADE and Healthcare (XLV) stands alone as the only sector positive on TREND.

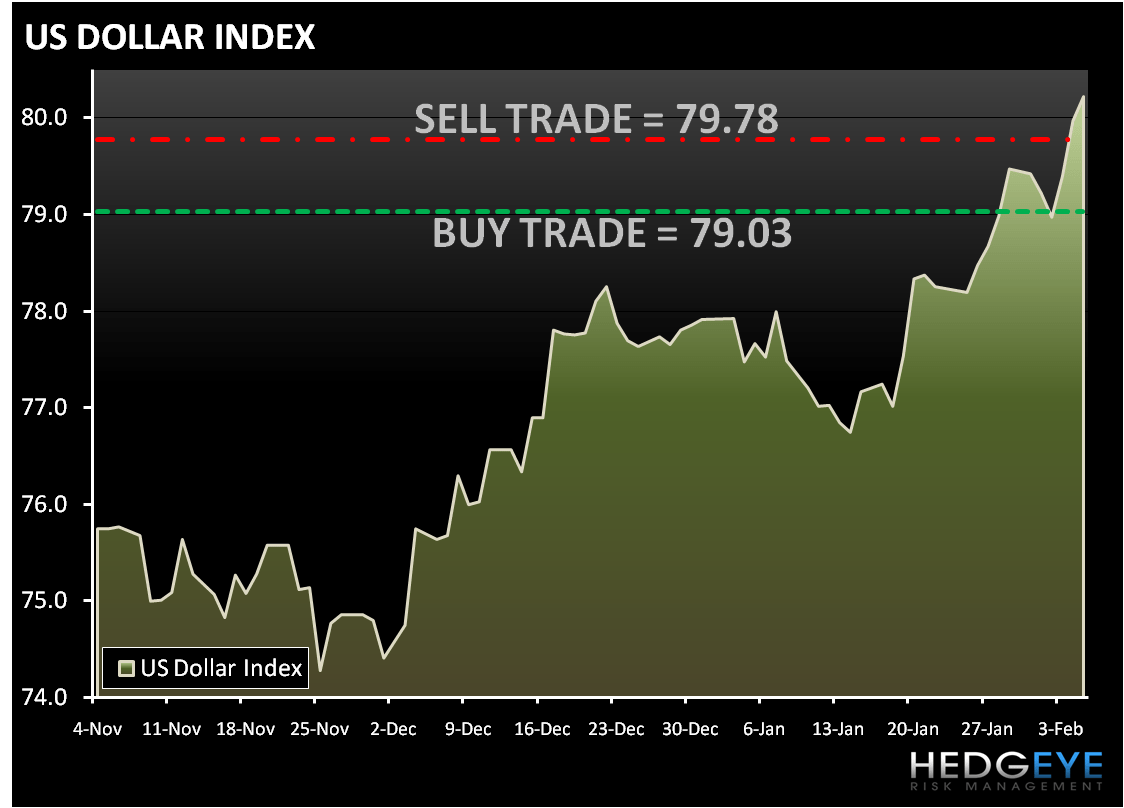

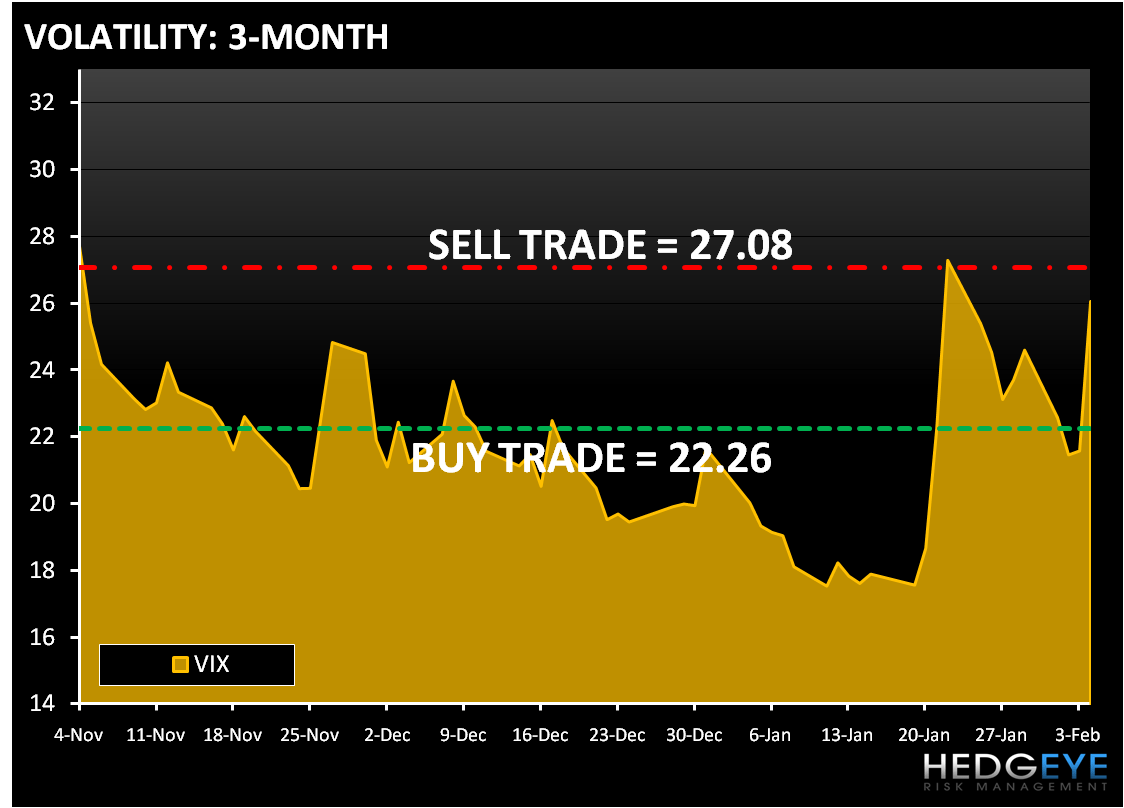

The pickup in the RISK AVERSION trade was evident with the dollar Index being up 0.78% yesterday. The Hedgeye Risk Management model has levels for DXY at – buy Trade (79.03) and sell Trade (79.78). Yesterday, VIX was blown out to the upside by 20.74%. The Hedgeye Risk Management models have the following levels for VIX – buy Trade (22.26) and Sell Trade (27.08).

Yesterday we did some buying/covering shorts. We covered our short positions in the S&P 500 Gold and Oil. Every short position has a time and a price where it’s immediate term oversold. We remain bearish on the SP500 from an intermediate term TREND perspective with resistance at 1,101.

China continues to be a MACRO headwind for stocks with the continued stories highlighting tighter credit conditions.

Another MACRO headwind was the initial jobless claims number, which came in significantly higher than expectations. Initial unemployment Claims came in at 480,000 last week, up from 472,000 last week (revised up 2k). The 4-week rolling average ticked up 12,000 to 469,000 from 457,000 last week. The improvement in this metric since March of last year has been tailwind for the equity market. This metric raised some concerns about tomorrow's release of January nonfarm payrolls.

The Financials were the worst performing sector yesterday, declining 4.3%. After falling more than 2% on Wednesday, the banks group remained a source of funds with the BKX down 4.3%. A number of Financials are struggling to find the post-crisis valuation level given the uncertainty of what the business models will look like post-regulation. The regional banks also underperformed. As our Financials analyst, Josh Steiner, noted yesterday the heightened employment concerns are a headwind for the financials, as the labor market recovery is a key component of future credit trends.

Rounding out the top three worst sectors were Energy (XLE) and Materials (XLB). Obviously, the XLB and XLE are the two sectors with outsized exposure to RISK/RECOVERY/REFLATION trade. The strength in the dollar and the continued removal of excess liquidity in China are the major macro-leaning headwinds putting pressure on these sectors.

On a relative basis, Technology (XLK) outperformed yesterday on the heels of largely upbeat 4Q earnings. However, inventory build concerns are part of the reason the SOX is severely underperforming.

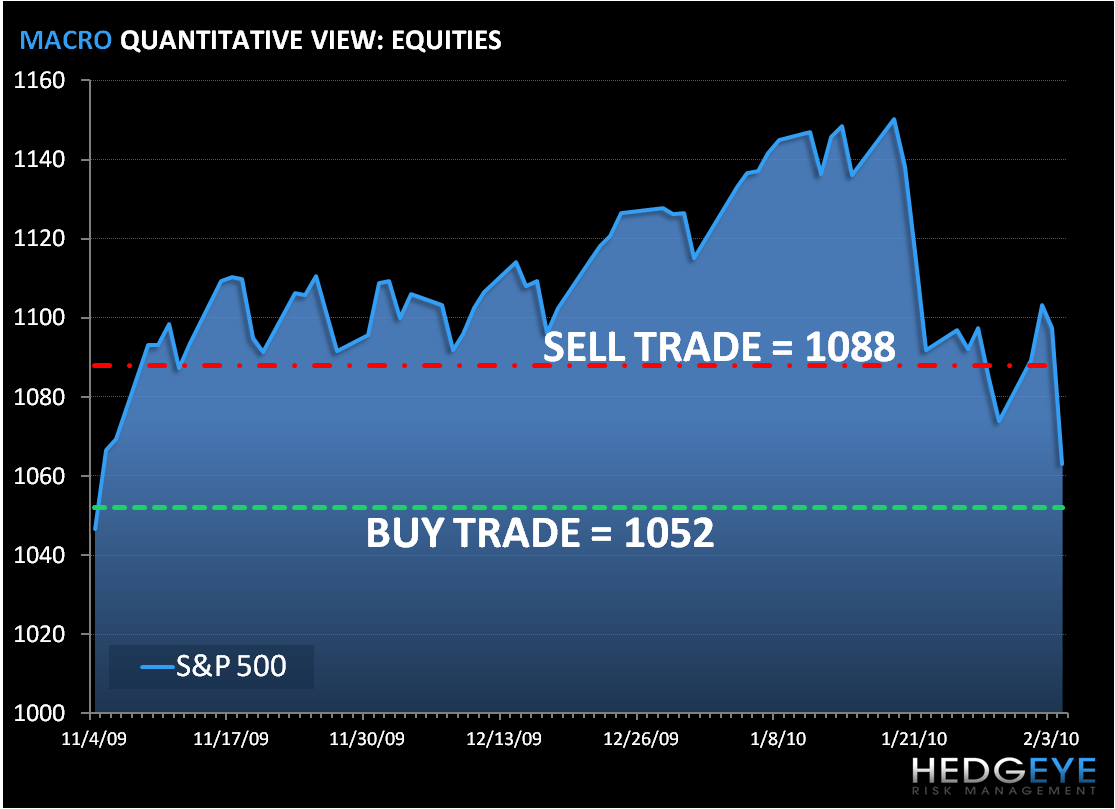

As we look at today’s set up, the range for the S&P 500 is 36 points or 1.0% (1,052) downside and 2.3% (1,088) upside. Equity futures are trading slightly below fair value in the wake of yesterday's painful declines and ahead of today's job's report. Also the there are continued concerns surrounding the P.I.G.S. and their debt issues.

According to Bloomberg News, Copper stockpiles jumped in Shanghai to the highest level in almost six years this week. Copper traded down 3.1% yesterday and is down nearly 14% this year. The Hedgeye Risk Management Quant models have the following levels for COPPER – Buy Trade (2.81) and Sell Trade (3.13).

Gold is trading a three-month low in as the dollar’s rally hurts gold’s appeal as an alternative investment. The Hedgeye Risk Management models have the following levels for GOLD – Buy Trade (1,052) and Sell Trade (1,110).

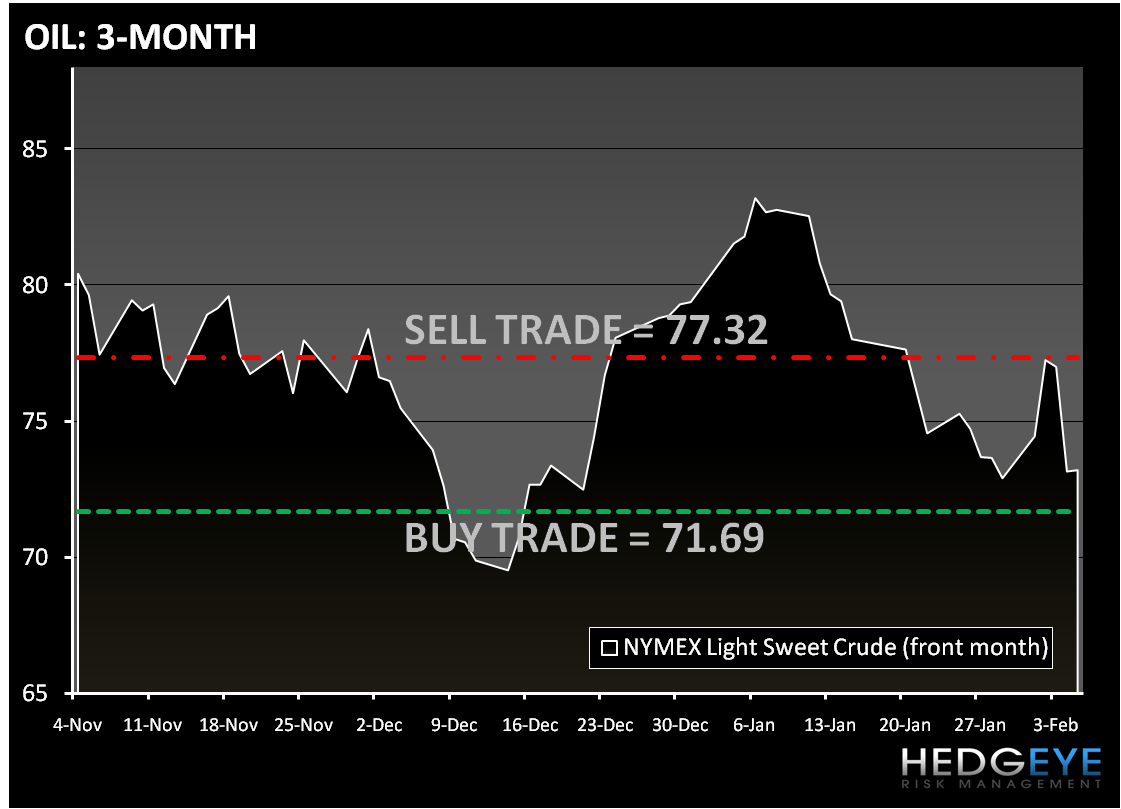

In early trading crude oil is trading flattish following its biggest decline in six months, as decline in the equity markets and a strong dollar are putting pressure on the commodity. The Hedgeye Risk Management models have the following levels for OIL – Buy Trade (71.69) and Sell Trade (77.32). Yesterday, we covered our short in the US Oil Fund (USO).

Howard Penney

Managing Director