CALL REPLAY: CLICK HERE

Topic Timestamps:

- Thesis Overview (2:36 – 11:50)

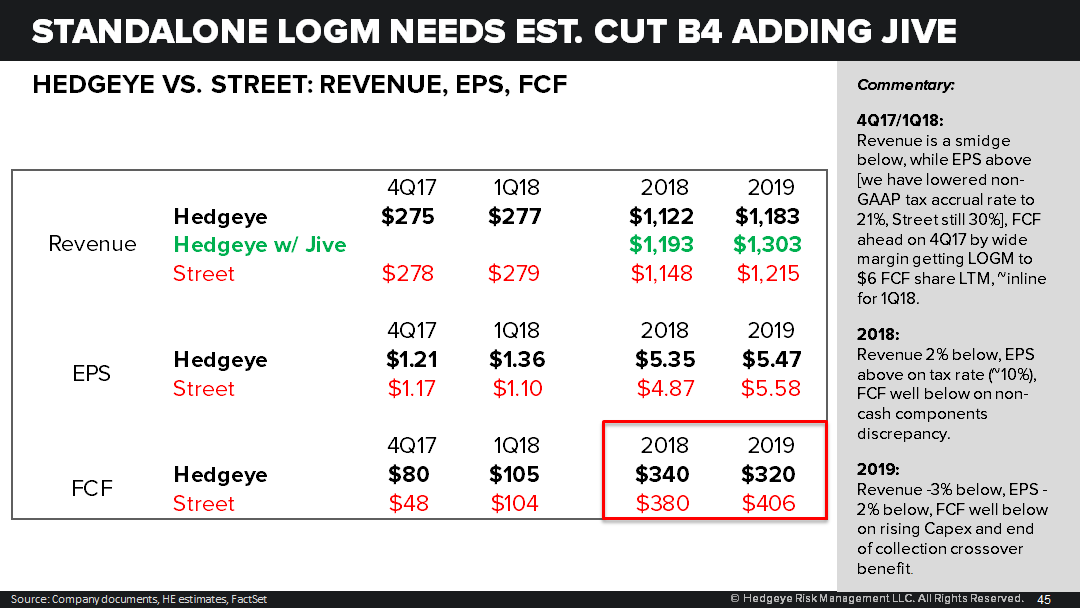

- The Revenue Estimate Cut We Need to See (12:07 – 13:30)

- How Much is GoToMeeting Actually Growing? (14:04 – 17:00)

- Excellent Product Managers (18:38 – 22:20)

- Brilliantly Taking Price on a Declining User Base (22:25 – 27:00)

- FCF Puts and Takes (27:55 – 35:25)

- Why Jive Fits Perfectly (35:25 – 41:50)

- LastPass: the Good and the Bad (42:00 – 45:00)

- Customer Churn and Inconsistent KPIs (45:00 – 49:10)

- Street Misconception on Gross Margin Improvement Potential (49:15 – 53:00)

- Conclusion and Q&A (53:00 – 62:30)

Bottom line for the stock: the addition of Jive raises the sustainable growth rate for the company in the out-years (2019-2020) from ~4.5% to 6%+. Consider that $6 in FCF/share would be worth ~$110 fair value on 5.5% FCF yield (inverse of growth rate). But at a 6%+ revenue growth rate, the same math gets to $150 fair value, and even extends to $170 given we think the growth rate moves all the way up to 6.5%. Translation: all other factors neutralized, it can be good for the stock when Jive really matters.

What happens next?

To get a clean setup we need an estimate cut on standalone LOGM revenue and some disappointment to register that FCF guidance is partly fluff, and that FCF trajectory is flat to down in 2019.