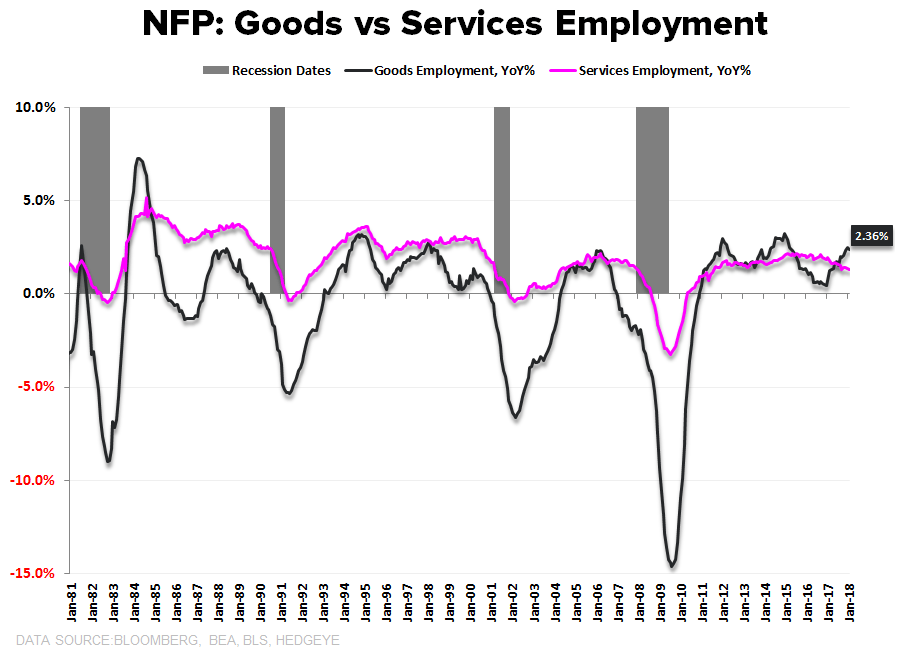

THE GHOST OF NFP FUTURE? ..... This month’s Labor data was a quintessential preview of both what needs to happen and what has become increasingly likely to happen over the next segment of the cycle.

For the expansion to progress durably, what needs to happen is relatively straightforward. The simplicity, however, shouldn’t dilute the significance:

- Payroll growth will continue to slow. It did in January. Check.

- Wage inflation needs to accelerate (and will need to continue doing so to offset the payroll slowdown). It did in January –> at +2.9% Y/Y = strongest growth since May 2009. Check.

- Accelerating wage growth and decelerating payroll growth need to net positive such that Aggregate Income Growth can accelerate and the baseline, forward view on consumption can remain favorable. Check (kinda)

Some clarifying context on point #3. Aggregate Hours growth (payroll growth + ave weekly hours growth) slowed more than average earnings growth accelerated which implies that aggregate private sector income growth decelerated in January. This is likely a false read. The deceleration in aggregate hours growth was due, primarily, to the fall in average weekly hours.

Now, it could be that employers toggled work hours lower in the face of increased minimum wage pressure. It’s equally likely, however, that weather effects acted to distort that figure lower. Workers ‘Not At Work Due to Weather’ increased to +496K alongside the Bomb Cyclone to start the year. This is up from 126K last month and 395K last January.

Policy, Prices & Forward Prospects .... The policy read-through is obviously hawkish, something the bond market and bond proxies have been conspicuously front-running as have policy expectations with the probability of a March Rate Hike sitting at 99% into the print.

Recall, most of the 18 state minimum wage increases began in January. The change to tax withholdings hit paychecks for the first time this morning and bonuses will be distributed in the coming month(s) so the upward pressure on ATI will persist next month. And not all of those impacts are captured in the wage data by the BLS (the BLS wage series doesn’t capture non-recurrent bonuses, for example) so the increase in reported wage growth will understate the impact to disposable income.

In other words, improved consumption capacity is likely to characterize the collective consumer nearer-term. And, as we’ve highlighted, if minimum wage increases, tax law changes and a corporate bonus bonanza can buy the economy some rate-of-income-growth buffer while the labor market continues to tighten over the next year, there exists a higher probability that organic wage inflation could then take the hand-off.

There have been many false dawns vis-à-vis wage growth over the last 4 years. This one appears more harbinger than head-fake.