It’s rare that Keith reaches out to us and says “XYZ Ticker looks awful” (based on his multi-factor models). Well, yesterday he said just that on ARO. At last count there were 34 published sell-side ratings on Aeropostale. Wow, that’s a crowded debate! That puts the “coverage” smack in the middle of the 23 analysts following GE and the 40 following Google. So what does ARO do aside from selling cheap teen apparel to deserve all this attention? Over the past year, the company has arguably been the biggest beneficiary in specialty apparel retailing from a confluence of positive events. Let’s look at the facts:

- The company’s highly promotional marketing approach and value pricing resonated well with the core 14-17 year old consumer over the past year. Same store sales are up 10% YTD on top of an 8% increase in 2008. With an average unit retail of around $11.80, there is no question that ARO’s price-driven merchandising strategy is working as higher priced competitors American Eagle and Abercrombie continued to lose share. It’s no coincidence that Old Navy, Rue 21, and other deep value apparel retailers also outperformed.

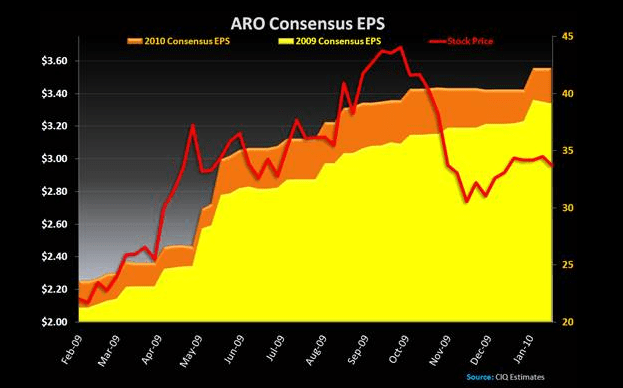

- Along with the topline, came an outright breakout in the company’s profitability. With the fiscal year essentially over, ARO’s EBIT margins expanded by 400 bps in 2009- ending the year somewhere around 17.2% (beyond peak). That puts ARO in the upper quartile of all vertically integrated specialty retailers, eclipsing JCG, GPS, ANF, and pretty much every other mall-based retailer on the planet. Very rarely, if ever, have we seen a high-teens margin structure exist at a company that plays the in the value arena. COH, ANF, CROX, DECK have all been there at one point or another, but these are all brands with price points substantially higher than ARO…

- With 950 stores, ARO is no longer a growth driven story. In fact, the core store base is pretty close to maturity. As a result, same store sales leverage is huge. A fixed cost infrastructure pumping more and more units (180-190 million annually) through the same number of boxes is surely going to yield outsized upside. This is especially true if you consider that one-third of the store base is approaching 10 years old and rents are probably pretty good in those locations. Add to that some recession-driven cost cutting, and the formula makes a ton of sense. Customer traffic increases (helped by the economy, supported by ARO’s aggressive marketing efforts) and throughput have been key to the strength in 2009. But can this continue? And for how long?

Now let’s look at some concerns:

- While still in its infancy, the company’s key growth vehicle of the future is P.S. by Aeropostale, a concept aimed at a 7-12 year old consumer. This makes a ton of sense longer term, as it’s probably cost effective to merchandise the brand as a “takedown” of the older original. However, any ramp on growth will be a negative based on mix alone. It’s near impossible for a chain of 40 or so stores to approach company average margins without greater scale. Yes, it is still early to make a call on the concept’s eventual success, but nonetheless it’s both risky and margin dilutive in the near term.

- Management cites the company’s past history when AUR’s were closer to $14-$15 vs. $11.80 today. This is an opportunity according to management, and it surely seems like one on the surface. However, raising prices (even if done the right way through better quality, trims, features) seems counter to what has been driving the business over the past two years. Given the company’s strength in driving price driven purchase decisions, it seems unlikely that taking prices higher will be well received. Yes, adding more fashion product into the mix has been in part a reason to command a higher ticket, but this also adds inventory risk. ARO has historically been a fashion follower, which makes it hard to believe that they can successfully transition into a fashion leader.

- Co-CEO’s will take the helm in 2010. The combination of an operating executive and a merchandising executive makes sense on paper, but this combo rarely works. Before you email us with examples of how this has worked in the past, Aeropostale is no Ralph Lauren.

- The shares have generally stopped responding positively, to positive news. Even with continued upward earnings revisions, driven by outsized same store sales it appears that even the most aggressive assumptions are already discounted in the stock. Yes, the shares appear cheap at 10x this year’s earnings, but the reality of slowing comps and potential EBIT margin contraction is likely to keep a lid on the shares at a minimum. Any hiccups along the way with management’s transition and potential inventory build and this suddenly becomes one of our favorite shorts…

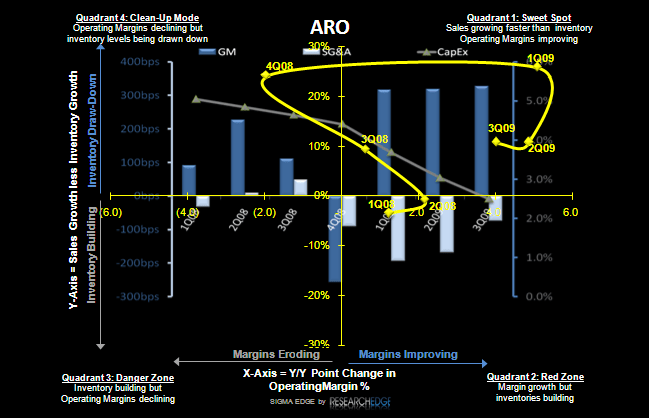

- Finally, our latest SIGMA analysis suggests that the peak may have already occurred. Sales are still outpacing inventory growth, but the spread is narrowing. Margin compares begin to increase meaningfully in 1Q. With such a heavy reliance on selling more and more units, it’s becoming harder to envision a third year in a row of outsized same-store sales without a commitment to more inventory and/or higher price points. Both prospects would suggest higher incremental risk…

Eric Levine

Director