THE HEDGEYE EDGE

The “Amazon of Real Estate” was how Redfin CEO Glenn Kelman described his company, the real estate services that popped 45% on the day of its IPO on July 28 and as of today has run up 82.7% from its opening price. We agree with the assessment that it is like Amazon- in that it gets a valuation like the tech giant.

While we do see Redfin as a company with strong technological roots, they themselves maintain that they are in fact a real estate broker- something that would necessitate a valuation closer to peers Realogy and Re/Max. To put this in perspective, Redfin trades at ~20x the valuation of Realogy from a market cap/market share perspective, with Redfin market share hitting its all-time high of 0.71% last quarter.

We believe that the underlying model assumptions for Redfin on the Street are misaligned to what the company really is: a technologically-derived traditional broker. This is not a model that can scale as easily as investors would hope. To grow brokerage transaction volume requires a near-linear agent growth à la a traditional real estate brokerage business- an expensive headwind that constricts RDFN’s opportunities to generate operating leverage.

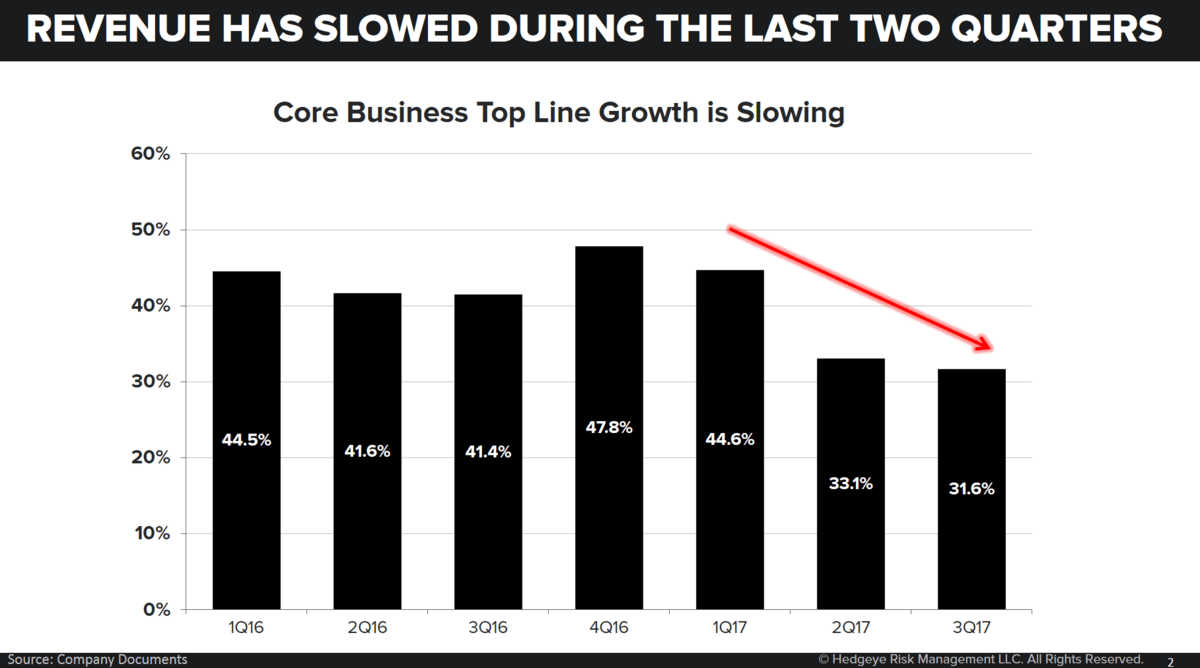

And at the top line, Street revenue estimates suggest ongoing years of 30% annual growth; and yet we are already starting to see quarterly growth slow on the margin, with 3Q17 core brokerage revenue growth decelerating 980bps from 3Q16. If this trend of deceleration were to continue, expectations will have to adjust accordingly, opening risk to multiple compression going forward.

INTERMEDIATE TERM (TREND)

In their most recent earnings call, Redfin announced that they are dabbling in “experiments” to improve the business efficiency. For instance, worsening affordability in the larger, most competitive markets has lowered Redfin’s close rates. In turn, they are spending more than usual on customers who don’t close on the home, plus the compensation for contractors and agents involved in the dealing. As such, their solution is to experiment with allocating fewer homebuyers per agent in order to create a more personal touch.

While higher close rates should lead to gross margin improvements, Redfin’s strategy of fewer homebuyers per agent runs the risk of lower revenue opportunity per agent should close rates not improve- note that management does not expect gross margin improvements until 2019 earliest.

Additionally, lock-up agreements pertaining to Redfin’s IPO are set to expire on January 23. After such date, up to an additional 70.75 million shares of common stock will be eligible for sale in the public market- with approximately 20.1 million of those shares held by insiders

LONG TERM (TAIL)

Although there are tailwinds for the broader housing complex, RDFN will face difficulties maintaining their growth in the face of affordability pressures and the inventory crunch. 69% of RDFN revenue is isolated to their top-10 markets, many of which are some of the fastest price appreciating markets in the country.

Buyers in these markets, while still eager to buy a home, are struggling to find what they are looking for given high home prices and limited options available. These areas are also unsurprisingly the most competitive in the country, forcing Redfin to source new market share gains from the middle of the country where competition is lessened and average prices are lower. On the margin, this will reduce the revenue per agent, slowing their growth further,

The reality of the situation is that they are not the only real estate service taking up technology in their business. Realogy, having already purchased ZipRealty for $166m in 2014, launched a new era for the company with the announcement of Ryan Schneider as the new CEO in succession of Richard Smith. Schneider, coming from a 9-year tenure as the President of Capital One’s Card division, has strongly emphasized his desire to bring Big Data, analytics and technology to Realogy in order to spark its future. Combined with Realogy’s already strong tech spending, we believe it to be a question of when Realogy, for instance, catches up to Redfin’s tech, and not if. So it begs the question: why pay the premium for Redfin?

ONE-YEAR TRAILING CHART