“Have I got the score right?”

-Bill Belichick

Welcome to 2018! The aforementioned quote comes from a book I started reading this weekend called The Education Of A Coach, by David Halberstam. Belichick’s follow on question to his assistant coaches was “then what the hell are they trying to do?”

En route to the New England Patriots 3rd Super Bowl victory in 4 years, the Patriots were up 24-14 and Belichick couldn’t understand why the Philadelphia Eagles were letting the clock burn out. He thought the score on the scoreboard was wrong.

Ultimately, it wasn’t. The point of the story is that the best Coaches and Portfolio Managers in the world are constantly questioning their premise. Whether it supports their position or not, no detail of The Game is ignored. Confirmation biases are constantly checked.

Back to the Global Macro Grind…

Day 1 in a new season is always my favorite work-day of the year. The score resets at zeroes. Other than lessons learned, nothing about the score in the year prior matters anymore. The only thing that matters to me is how we react to incoming data and market signals.

Looking back at the last week of 2017 is no different than looking back at any other week. We’re tasked with analyzing last week’s macro market moves within the context of intermediate-term @Hedgeye research TRENDs.

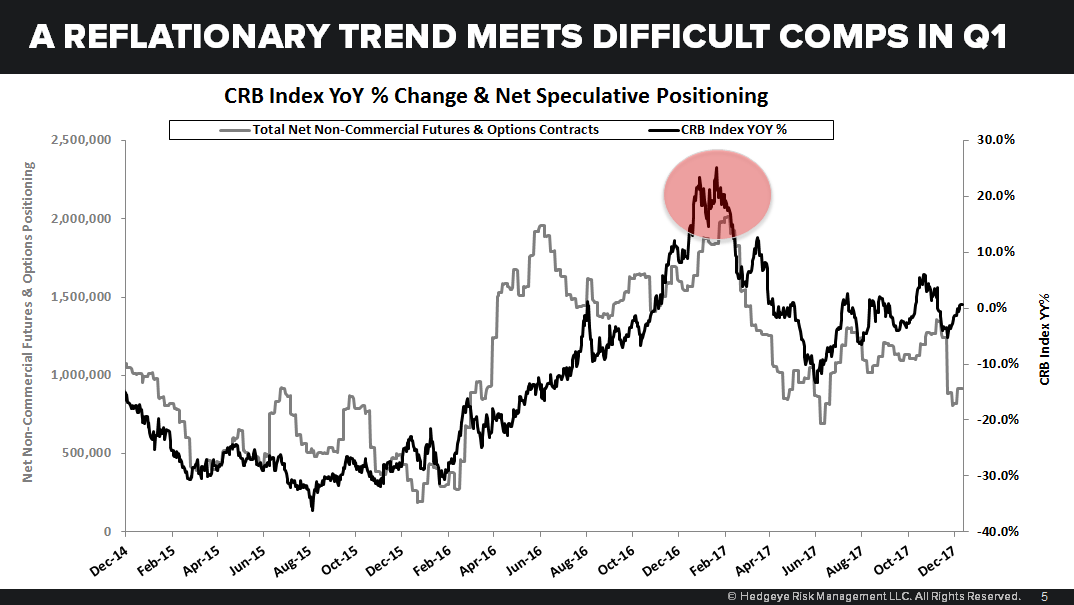

In terms of Currencies and Commodities, last week was a reflationary one (in Dollars):

- US Dollar Index broke intermediate-term @Hedgeye TREND support, dropping -1.3% on the week

- EUR/USD broke-out above @Hedgeye TREND resistance of $1.19, rising +1.2% on the week in kind

- British Pound rose another +1.1% vs. USD and remained Bullish TREND @Hedgeye

- CRB Commodities Index ramped +3.2% on the week = Bullish TREND @Hedgeye

- Oil (WTI) broke out to fresh 3 month highs, +3.3% on the week = Bullish TREND @Hedgeye

- Natural Gas ripped +11.1% on the week (-20.8% YTD) getting it back to a NEUTRAL @Hedgeye TREND

- Copper tacked on another +1.9% to its 2017 Reflation = Bullish TREND @Hedgeye

- Nickel was up another +5.2% to +25.1% in 2017 = Bullish TREND @Hedgeye

- Coffee reflated +4.8% on the week to -15.6% YTD = Bearish TREND @Hedgeye

- Silver bounced a big +4.3% on the week to +5.2% YTD = Bearish TREND @Hedgeye

While the FX and Commodities moves in the aggregate were reflationary, the problem with headline (reported) inflation is that the DEC-FEB compares get meaningfully more difficult than SEP-NOV year-over-year comparisons were. This makes for an interesting juxtaposition.

If you ask Mr. Bond Market, he wasn’t too concerned about “reflation” last week:

- UST 2yr Yield pulled back from its 2017 highs, closing down 1 basis point on the week but still Bullish TREND @Hedgeye

- UST 10yr Yield corrected -8 basis points from the prior week and remains Bullish TREND @Hedgeye (bearish for UST Bonds)

- US 5-year 5YR Forward Break-evens were only up 1 basis point to 1.99%

The way I read this (for now) is that the market has it right. The SEP-DEC move was reflationary but reflation is setting up to make lower-highs vs. those we saw on a reported CPI and PPI basis in the 1st half of 2017. Break-evens are running close to our inflation forecast too.

In terms of Global Equity market read-throughs last week:

- US Dollar sensitive EM markets like Brazil liked the reflation, closing up 1.6% on the week to close out 2017 at +26.9%

- European Equity markets do not like strong Euro vs. USD (Germany and Spain were down -1.2 to -1.4% on the week)

- US Equities saw Utilities (XLU) +0.4% and Energy (XLE) +0.4% beat Tech (XLK) which finally corrected -0.9% into year-end

From a US Equity Style Factor perspective:

A) High Beta Stocks led losers last week, dropping -0.7% to close out 2017 at +20.4%

B) Large Cap Stocks corrected -0.4% last week as well to close out 2017 at +23.4%

Both the Tech and Style Factor corrections were what we call counter-TREND moves so you’ll have buying opportunities in both this morning. I’m going to stay with US Tech (XLK) and Consumer Discretionary (XLY) as our favorite 2 sectors vs. Utilities (XLU) as one of our least liked. I still like US Growth LONG vs. Southern European Equities SHORT too.

These views may very well change as we roll through the first 3-6 months of 2018. Instead of making grandiose establishment sounding “calls” with useless “year-end price targets”, I’ll stay with my process and read and react to The Game as it changes.

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND views in brackets) are now:

UST 10yr Yield 2.35-2.52% (bullish)

SPX 2 (bullish)

NASDAQ 6 (bullish)

DAX 125 (bearish)

VIX 9.14-11.51 (bearish)

USD 91.55-93.26 (bearish)

EUR/USD 1.18-1.20 (bullish)

GBP/USD 1.33-1.35 (bullish)

Oil (WTI) 56.77-61.08 (bullish)

Nat Gas 2.52-3.03 (neutral)

Copper 3.10-3.35 (bullish)

Best of luck out there this year,

KM

Keith R. McCullough

Chief Executive Officer