This week Congress passed tax reform. Below is an update to our Twofer note and call on Nov. 21:

ELIMINATION OF INDIVIDUAL MANDATE PENALTIES

In a “who’d a thought” moment in the storied history of ACA repeal, effective end of the individual mandate has moved through the tax reform process on greased skids.

As we discussed in our Twofer! note, it is difficult to say exactly what effective repeal of the mandate means to insurance premiums on the individual market. Since the mandate has been poorly enforced or not at all, most insurers are not counting on it to attract healthy people to their risk pools in CY 2018. The effective end of the individual mandate in CY 2019 probably means not much will change as far as actuarial assumptions go.

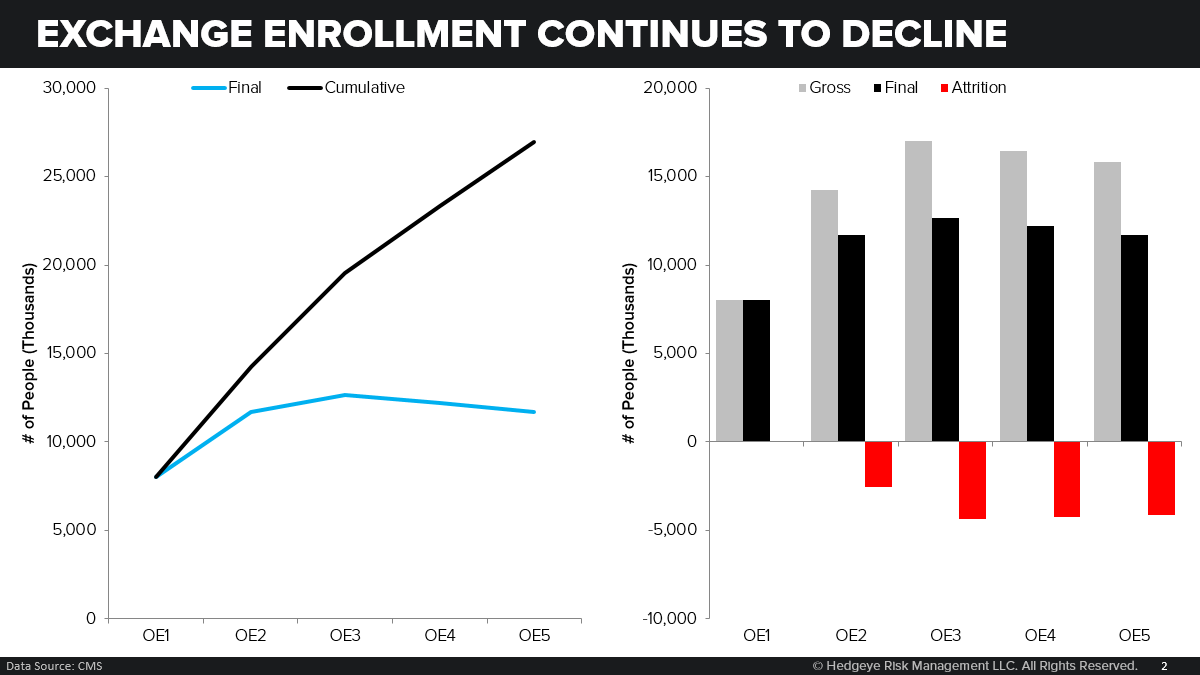

Growth in Insured Medical Consumers has and will continue to slow, regardless. Medicaid is dis-enrolling as states increasingly take responsibility for eligibility checks and tighten the purse strings in the face of less funding from the Federal government. With employment at 4.1 percent, we expect little growth in employer-sponsored insurance. Medicare enrollment reflects demographics and is expected to grow at less than 2 percent.

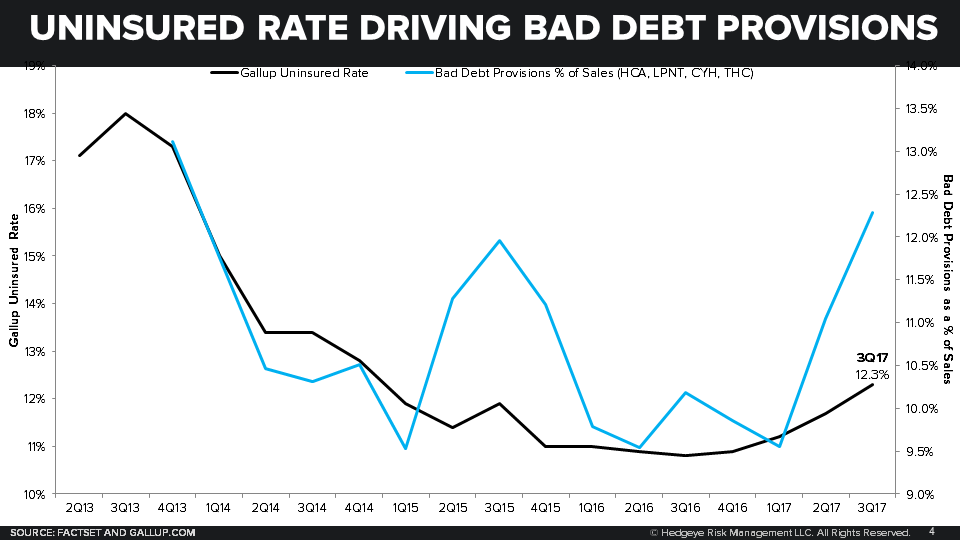

The end to the individual mandate will exacerbate slowing growth in Insured Medical Consumers. It even appears that the mere specter of repeal in the individual mandate has changed behavior. The recently released Gallup-Sharecare Well Being Index indicated an increase in the uninsured rate of 12.3 percent in 3Q 2017, up 0.6 percentage point from 2Q 2017 and 1.4 percent from 3Q 2016.

The Gallup-Sharecare uninsured rate excludes people who have insurance that is not ACA compliant. Short term plans like those sold on the HIIQ platform and association plans like those sold by the Tennessee Farm Bureau would be considered health insurance by survey respondents but would not pass muster with the federal government.

The increase in the percentage of people reporting that they do not have health insurance corresponds with the persistent threats to the ACA, including an end to the individual mandate, throughout the winter and summer of 2017.

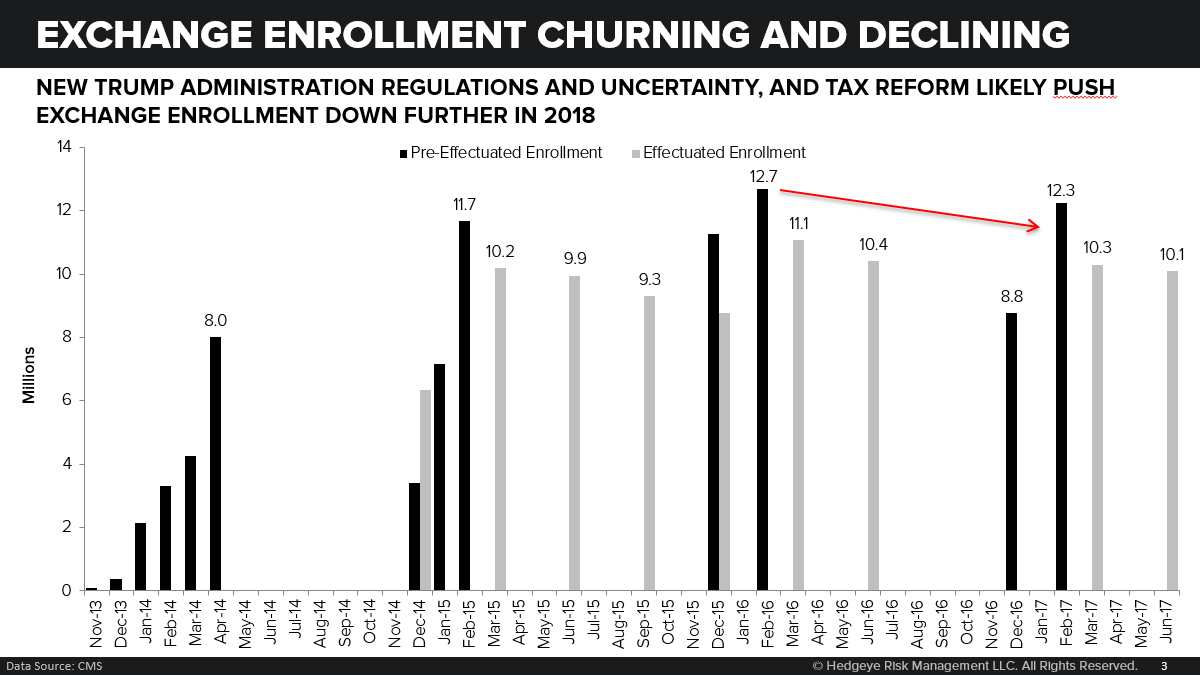

Enrollment in the federal exchange, www.healthcare.gov for CY 2018 also appears to reflect a trend in higher insurance rates. Yesterday, CMS announced 8.8 million sign-ups, a decline of 400,000 from OE 2017.

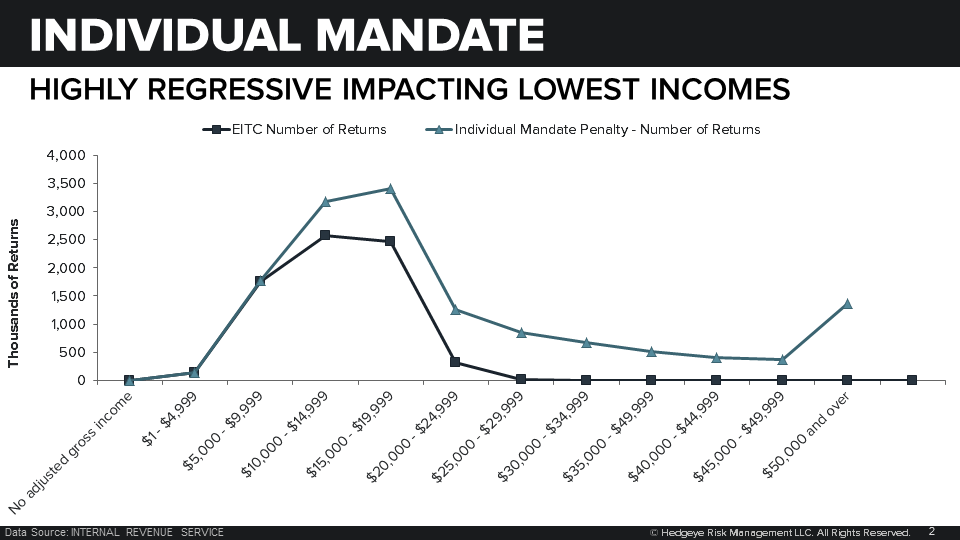

Other factors contributed to the increase in the uninsured rate, of course. The cost benefit analysis for an individual enrolling in a plan on and off the exchange has increasingly argued for simply paying the individual mandate penalty instead of high monthly premiums. For individuals eligible for an Earned Income Tax Credit, the strategy represents no out-of-pocket costs.

Alternatively, individuals without a source of health insurance from their employer or a federal program may elect to purchase non-compliant plans that offer fewer benefits. They too would pay the individual mandate penalty.

With the individual mandate penalty eliminated and with premiums on the non-group market still quite high, there will be more upward pressure on the uninsured rate. How much the end to the individual mandate will contribute to that increase is difficult to say. More uninsured people means more bad debt and charity care for providers.

If the individual mandate doesn’t make people run out and get health insurance, it does drive the politics. CBO scores calling for 23-24 million person increase in the uninsured population and that ultimately sunk ACA repeal last summer, are driven by an insurance coverage model heavily influenced by the individual mandate.

In the most recent analysis of the individual mandate, the CBO acknowledged that its forecast model might have some flaws. They reduced their estimate of the impact of repeal of the individual mandate and pledged to undertake more analysis.

Congressional action that induces enrollment in insurance coverage by making it more affordable, for example, will likely result in a CBO score that reduces the uninsured population. That somewhat counter intuitive result makes bipartisan agreement, especially in the Senate, a bit more likely.

States, of course, would be free to adopt a mandate as Massachusetts did when it adopted Romneycare in 2006. However, a state’s ability to implement and enforce such a mandate will depend on the tools they have available. A state without an individual income tax, like Florida, will not have the threat of a tax penalty to assure compliance, for example. California, on the other hand may have more luck, although the idea of the individual mandate is politically unpopular.

In the end though, effective repeal of the individual mandate will probably mark the beginning of the end for the ACA. The individual mandate is in many ways the philosophical core of the ACA, a manifestation of the belief that everyone must have health insurance coverage as part of a social contract. With that underlying tenet gone, other portions of the law, like the onerous benefit regulations, are more easily dispatched.

CORPORATE TAX RATE

Congress determined that the current graduated corporate tax rate will be replaced with a flat 21 percent rate, effective with tax year 2018. Alongside that rate change is a reduction in the Dividends Received Deduction (DRD). Under current law, a U.S. corporation can deduct 70 percent of dividends received from another domestic corporation. In the case of a 20 percent owned domestic corporation the DRD is 80 percent.

The new DRD will be 50% in most cases and 65 percent in the case of a 20 percent owned domestic corporation.

The change in rate from the 20 percent rate approved by each of the House and Senate comes after Sen. Marco Rubio “threatened” to vote no if his proposed increase in the child credit was not included in the final bill. The incremental change in the corporate rate provides sufficient budgetary offsets to fund an increased child credit and please Sen. Rubio.

Unlike the Senate bill, the final verion adopted by Congress elected to eliminate the Corporate AMT which means that pharma and medtech companies that make use of the Research and Experimentation Credit will likely preserve their low tax rates.

Additionally, the change in the corporate tax rate is a tailwind for most US domiciled health care services companies. HCA and THC both report effective tax rates of 29 and 27 percent, for example.

REPATRIATION AND CHANGES TO TREATMENT OF FOREIGN INCOME AND TAXES OF US CORPORATIONS

It is no surprise that the vast majority of provisions designed to restructure America’s economic relationship with the rest of the globe were finalized by Congress. Leadership in both parties did a fine job of diverting attention from this core purpose and, for that reason, the changes to international taxation have been little discussed – present company excluded.

These changes are designed to repatriate stranded overseas income and put an end to practices that encourage its accumulation and other unproductive tax-driven practices. For that reason, the changes to the treatment of foreign earnings must be considered together and in the context of a new, lower corporate tax rate.

Provisions included in final bill:

- Repatriation of Indefinitely Reinvested Foreign Earnings is mandatory and applies to all US corporations with at least a 10 percent ownership of a foreign company even if the foreign subsidiary is NOT a CFC.

- A one-time tax with an effective rate of 15.5 percent on cash and cash equivalent investments and 8 percent on other illiquid assets will be assessed.

- The one-time tax is payable over 8 years in installments

- The Secretary of the Treasury is empowered to make rules to avoid double taxation and to head off strategies to avoid the one-time tax

- Companies with IDFE will be permitted some offsetting deductions so the entire $2.6T held overseas by publicly traded companies will likely be reduced somewhat.

Like us, you are probably thinking that all PFE, for example, needs to do to avoid a 15 or 8 percent tax on the $86B it holds overseas is to move its domicile. Well the bill has a response to that. Any company that expatriates within ten years of enactment of the tax reform bill will be denied any deductions against their IRFE and be subject to a 35 percent tax on the entire amount.

Ok, now you are thinking that a 21 percent tax rate will still be higher than the effective rates paid by many multinationals, particularly in pharma and medtech, and so keeping money overseas will still be attractive.

The bill has an answer for that too. The Base Erosion Anti-abuse Tax (BEAT) will require US companies that make payments to foreign subsidiaries to make two tax calculations. First, they will use the standard domestic method (using 21% rate) and include deductions for payments made to foreign subsidiaries. Second, the company will calculate taxes without deducting foreign payments but applying a 10 percent rate (instead of the 21 percent corporate rate) to the base. If the second calculation is greater than the first, the corporation will pay the difference in additional taxes.

To keep assets from accumulating overseas again, the final bill provides for a 100% deduction of foreign income received by a US corporation. No foreign tax credit or deduction would be allowed for any taxes paid with respect to any portion of a dividend received. The bill explicitly instructs the Treasury Department that dividends received is meant to be interpreted as broadly as possible.

For multinational health care companies with substantial income earned from intangible assets - namely pharma and medtech - the bill report establishes an effective foreign-derived intangible income tax rate of 13.125 percent for year 2018 through 2025 and 16.406 percent for 2026 and thereafter.

To the extent there are US corporations health care companies with Global Intangible Low Taxed Income (e.g. from intellectual property held by a Cayman Island subsidiary), the effective rate will be 10.5 percent for years 2017 through 2025 and 16.406 percent for years 2026 and thereafter.

Finally, Congress declined not to finalize a provision that would have permitted tax free transfers of intangible assets like brands and patents.

TAX RATE FOR PASS-THROUGH ENTITIES

The full Congress adopted the Senate’s approach of permitting individual taxpayers to deduct 20 percent – lower that the initially proposed 23 percent – of Qualified Business Income from a partnership, S corporation or sole proprietorship, REIT and cooperative.

Qualified Business Income means the net amount of qualified items of income, gain deduction and loss, taking into account only those items included in determining taxable income in a given year.

Excluded from the definition of qualified business are specified service trades that include services performed in the health field (i.e. physicians) in excess of $157,500, indexed.

The income limitation is designed to prevent abuse of the pass-through provisions by high wage earners. That limitation will also limit the effect a lower tax rate will have on pass through entities such as physicians practices and ambulatory surgery centers.

The final bill adopted the Senate’s language that permits an individual taxpayer to deduct 20 percent of qualified REIT dividends, qualified cooperative dividends and qualified publicly traded partnership income. Dividends from health care REITs like SBRA, HCP and HCN will be subject to a 20 percent deduction, effectively lowering the tax rate on these investments.

INTEREST EXPENSE DEDUCTION

The final bill, not surprisingly, included the provision that limits net interest deduction to 30 percent of adjusted taxable income. The Senate bill had defined adjusted taxable income as a corporation’s taxable income computed without regard to deductions for net interest expense, net operating losses and other adjustments as determined by the Secretary of the Treasury. The House version adopted the current law definition which excludes from the calculation net interest expense, net operating losses, depreciation and amortization.

Congress elected to split the difference. The 30 percent limitation will apply to EBITDA for years 2018 through 2021 and to EBIT for years 2022 and thereafter

Amounts that would be disallowed – net interest expense in excess of 30 percent of adjusted taxable income – could be carried forward to future years.

Congress did not adopt provisions that would limit of interest by multinationals that, due to the high corporate tax rate, have incentives to originate debt in the US.

In the short term, the limitation on interest deduction will likely not be felt too broadly while it is applied to EBITDA except for highly leveraged companies. However, highly leveraged companies will need to make some adjustments in anticipation of the limitation’s application to EBIT, when the provision will be more broadly applied. The value of the deduction, will of course be diminished by the effect of lowering the corporate tax rate.

NET OPERATING LOSS DEDUCTION

Beginning with tax year 2018, the Net Operating Loss deduction will be limited to 80 percent of taxable income. Taxable income will be calculated without regard to the NOL deduction. NOLs can be carried forward indefinitely.

The final bill repeals two year carrybacks except in the case of certain agricultural losses and in the case of property and casualty companies.

The limitation on NOL deductions will have an immediate impact. First, and most obviously, the deduction itself will be reduced from 100 percent of taxable income to 80 percent. Secondly, the value of the deduction will be reduced as a result of the new, lower corporate rate.

Companies like MDRX that do not and have not paid cash taxes in a few years will have to write down the value of NOLs due to the new tax rate. Going forward, the benefit will be reduced due to the change in deductibility.

Companies that generate a NOL beginning in 2018 will not be able to carry those losses back to the previous two years and reduce the tax liability in earlier years.

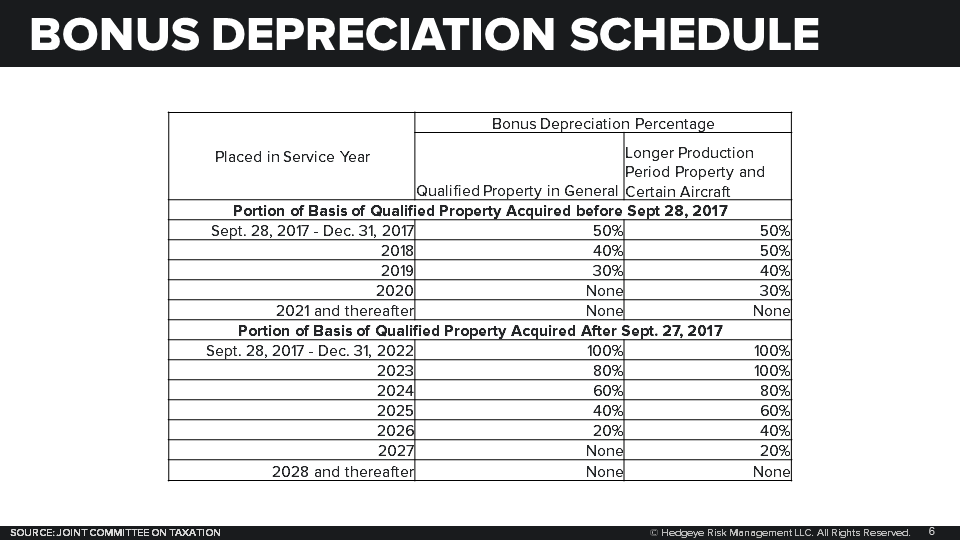

COST RECOVERY

The full Congress adopted the Senate’s treatment of additional depreciation with one very important difference. In the final bill, bonus depreciation can be applied to new and used property.

The new depreciation schedule is as follows:

Eligible property includes tangible personal property with a recovery period of 20 years or less under MACRS and certain off-the-shelf computer software.

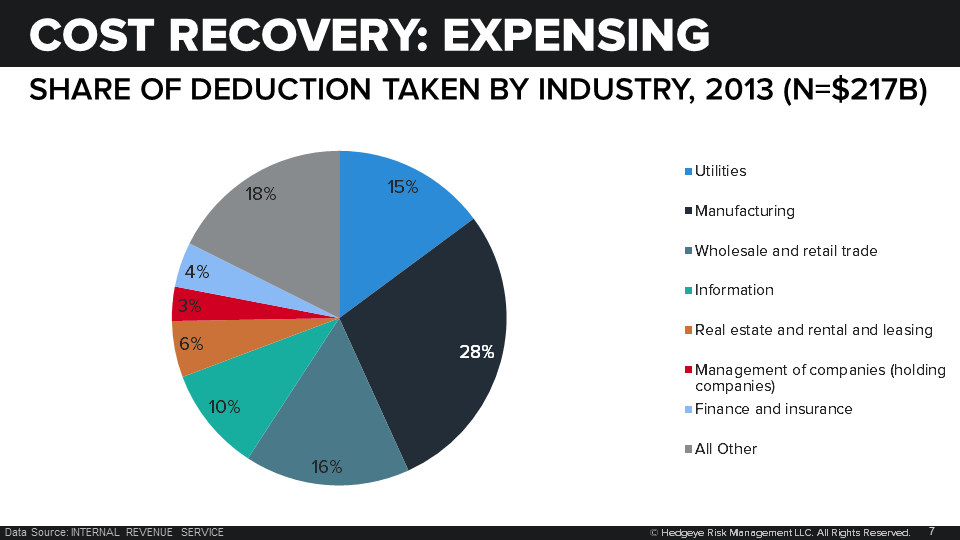

The intent of the provision is to encourage investment. At least in theory, the change in cost recovery rules should be a tailwind for equipment manufacturers like HOLX. However, the health care industry has not historically taken advantage of the additional depreciation like other capital-intensive sectors including manufacturing and utilities.

In 2013, when bonus depreciation was 50 percent, the primary beneficiaries were manufacturing and utilities:

ORPHAN DRUG TAX CREDIT

The House version of tax reform calls for complete repeal of the orphan drug credit. The credit is available to research organizations for up to 50 percent of qualified expenses. The Senate version simply reduces the credit from 50 percent to 27.5 percent.

Congress elected to reduce the credit to 25 percent but eases the restrictions on deductibility of clinical testing expenses designed prevent a double tax benefit.

Congress also opted not to adopt a Senate provision that would have limited use of the orphan drug credit. Under the Senate bill, the credit would not apply to testing a drug if the drug has previously been used to treat any other disease or condition, and if all diseases combined affect more than 200,000 people.

Do not consider Congress's decision abandon efforts to rein in the orphan drug credit's application to secondary indications, as an end of the conversation. FDA Commissioner, Scott Gottlieb has already indicated he will be taking a look at use of the credit.

MEDICAL EXPENSE DEDUCTION

In a deal with Sen. Susan Collins, the Senate version includes a restoration of the pre-ACA threshold for deducting medical expenses to 7.5 percent from 10 percent of Adjusted Gross Income for two years.

This provision was included in ACA repeal bills throughout the summer in both the House and the Senate so there is very little disagreement among Republicans about its inclusion.

AMORTIZATION OF RESEARCH AND EXPERIMENTATION

In a little discussed provision, the bill ends the deduction, effective on Jan. 1, 2022, for Research & Experimentation expenses and requires that they be capitalized and amortized over five years (15 years for R & E conducted overseas).

In effect, Congress is ending the practice of deducting R & E expenses from pre-tax income before feasibility has been determined. Instead ALL R & E would be charged to a capital account and amortized.

The provision would apply to any company that spent money on R & E except in the case of land development and property improvement (as in the case of EXAS’s new laboratory in Wisconsin) and for the exploration of ore and mineral, including oil and gas.

Interestingly, the bill explicitly includes software development in the provision – as if Congress wanted to be sure there was absolutely no ambiguity.

The implications of the change are not immediate due to the effective date and even then, it will vary by company. As technology sector head, Ami Joseph pointed out in a call earlier this week, FB will likely pay considerably more taxes because today they capitalize very little of their R & E expenses.

For the HCIT sector, the implications are more muted. For companies that are profitable and pay cash taxes, like Cerner (CERN), the R&D tax treatment would offset approximately 40% of the benefit of a lower tax rate, all other things being equal. CERN’s effective tax-rate would be higher than the 21% corporate tax rate, because R&D expense would be added back to taxable income.

What is likely to change in the near term are R & E investment decisions. Marginal projects are not as likely to be initiated in anticipation of the required capitalized in 2022.

Passage of the tax reform bill is not the end but the beginning of a long process of implementation that will keep your loyal policy analysts busy. Also, a technical corrections bill may be a very real possibility given objections to certain of the repatriation provisions being raised by the EU. So, get comfortable and as always we will be here to help.

A very warm and happy holiday to each of you.

Emily Evans

Managing Director

Health Policy

@HedgeyeEEvans