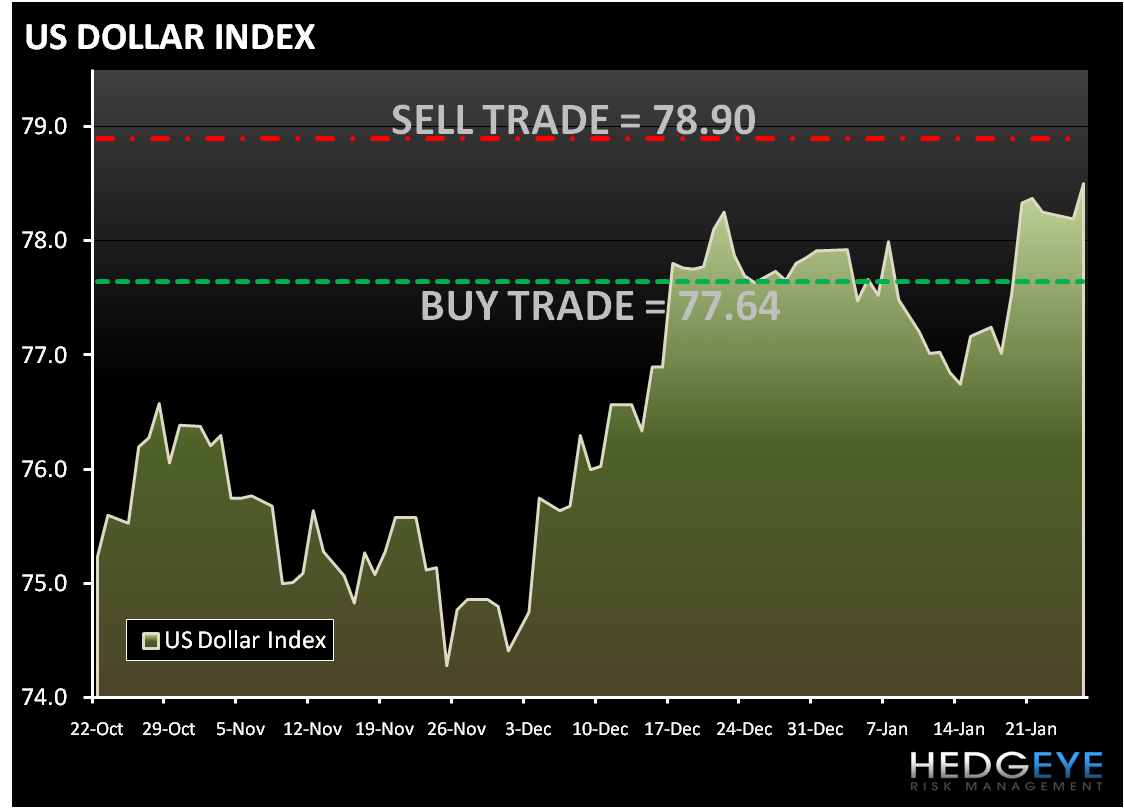

The S&P 500 finished slightly higher yesterday, +0.46% - on very light volume. The government sponsored volatility that weighed heavily on the market last week remained largely on the front-burner. The risk aversion trade showed some signs of relief with the VIX trading down 6.96% on the day. The Hedgeye Risk Management models have the following levels for VIX – buy Trade (22.51) and Sell Trade (29.54).

Some optimism did return as the prospects for Fed Chairman Bernanke's confirmation looked a little more like he would remain as the Chairman of the Federal Reserve.

On the MACRO front, December existing home sales disappointed, dropping 17%. I agree that the December existing home number is a statistical aberration, but that is not the point. The issue remains that the current trend in joblessness is still a big drag on the economy and the government can’t prop up the housing market forever.

The Materials (XLB) was the best performing sector yesterday after being the worst performing sector last week with some unwinding of the RECOVERY trade on concerns about an accelerated tightening schedule in China to combat bubble fears. Within the XLB, steel stocks recovered a bit of last week's 10% decline following the better-than-expected Q4 results out of AKS.

The second best performing sector was Technology (XLK), rising 0.8%. The outperformance was driven by the semi space with the SOX rising 1.4%; TXN was one of the notable gainers ahead of its Q4 results after the close. Memory names were another bright spot with SNDK and MU outperforming on the day. Lastly, AAPL was up 2.7% and a standout in the hardware space ahead of its December quarter results, which blew away expectations.

The Financials (XLF) was up in line with market yesterday. The banking group was also higher on the day, though underperformed the S&P 500 by 30bps. The XLF is bearing the brunt of the government sponsored volatility following last week's proposal by the Obama administration to disallow proprietary trading and hedge fund and private-equity investing on the part of any financial institution that owns a bank. The more defensive leaning trust names were mostly higher on the day, while the large-cap and regional banks were mixed.

As we look at today’s set up the range for the S&P 500 is 45 points or 1.5% (1,080) downside and 2.6% (1,125) upside. At the time of writing the major market futures are trading lower on the day.

Copper is trading lower in London trading on speculation that China will curb lending. The Hedgeye Risk Management Quant models have the following levels for COPPER – buy Trade (3.32) and Sell Trade (3.45).

In early trading today Gold is trading lower, as the whole commodity complex is trading lower on the day. The Hedgeye Risk Management models have the following levels for GOLD – buy Trade (1,081) and Sell Trade (1,104).

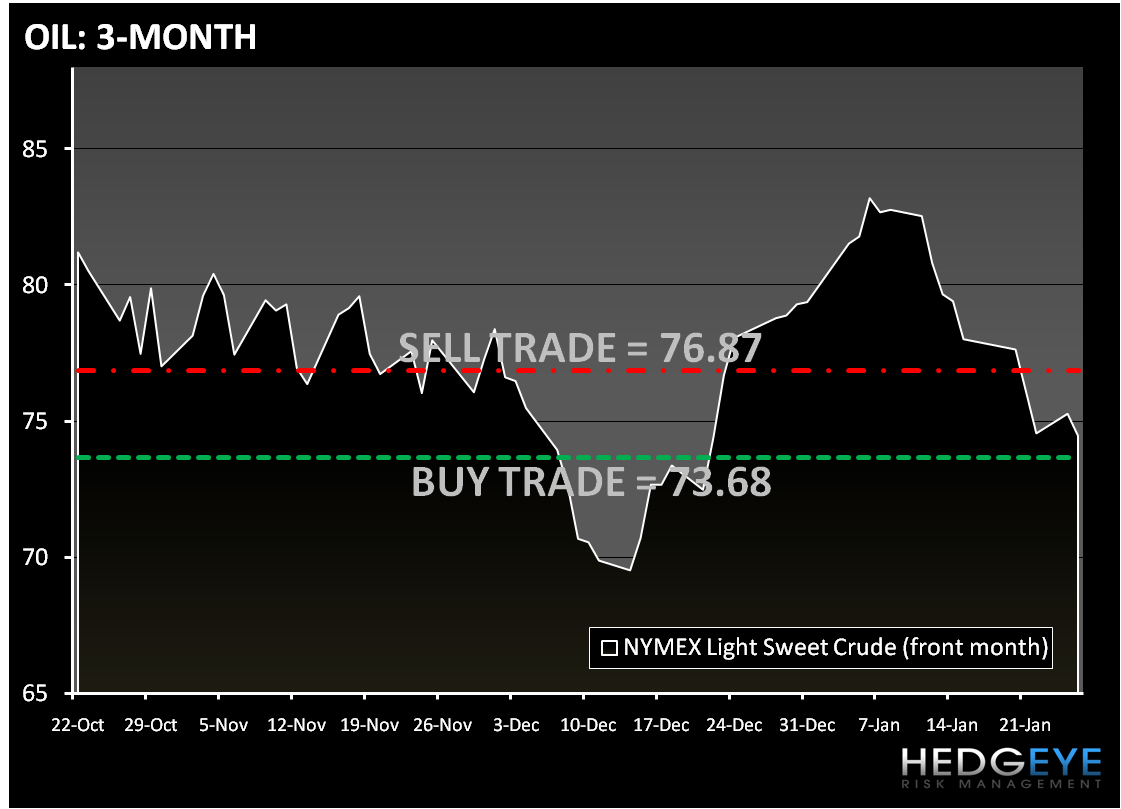

Crude oil is trading down on speculation that oil stockpiles are very high worldwide, while concerns persisted that China will tighten credit and slow growth. The Hedgeye Risk Management models have the following levels for OIL – buy Trade (73.68) and Sell Trade (76.87).

Howard Penney

Managing Director