Sony didn’t discover the next new major tech wave. They are not about to unseat Apple and retake their mantle in consumer electronics. They are not even about to really grow all that fast. But the company is in a (very long) process of eliminating under-performing divisions, moving borderline divisions to profit, and smartly allowing a great technology leadership cycle in semiconductor image sensors to play out in their favor, and in favor of the bottom line. Big conglomerates like Sony move slowly, and investors in the story are right to keep a pinch of skepticism around. But the move towards cash and profits is unmistakable and sets Sony on course to exceed profitability levels they have achieved in well longer than a decade. We think, with puts and takes and not in a straight line, that it is reasonable to consider medium to long term upside in Sony’s stock at 30-45%, even from current levels.

As with any conglomerate, not all the factors are knowable. Our review below presents our best effort at putting all the puts and takes together. A simple summary would be:

- PlayStation: +

- Music: +/-

- Movies: -

- Semis: +

- Mobile: - -

- TV: +

Netting all of this out, Sony’s stock is trading at ~14x LTM FCF, ~13x F17, and potentially ~10x F19, with upside revenue or profit potential in multiple segments in the coming quarters and years. The stock is up almost 30% since we introduced the stock to our Long Bench, yet the equity has become even cheaper, and the positives seem to have longer runway than we had originally imagined.

Upside/downside: in a worst-case scenario, we’d see 15x n-t FCF as a best case, or 15% more, with -13% downside risk if next year’s OCF is impaired by mobile restructuring, and if we have miscalculated the incremental capex required for semis. In a base case scenario, mobile restructuring is not an F18 item, and we have not underestimated capex, which would put 6-12 month upside at ~35%. Our F19 profit estimates incorporate mobile restructuring, as well as major losses in TV (our perspective only, no evidence at this point), but we get the semis capex reversal, so net FCF can still rise potentially setting the table for even further upside.

Further, what we imagine as potential negative fundamental catalysts today all have embedded positive twists, namely: semis capex, shutting down the mobile division, and lower Pictures revenue. Capex will keep the semis division in a leadership position in a market they dominate. Exiting mobile (our view, no such message as yet from management), and the one-time cost pain it will imply, is better than never ending liability to remain in that market, and lower Pictures revenue will actually test the budget/streamlining process of the new Pictures management team.

As good as it gets? Let's review:

- Semis get capex in F18 which will hinder FCF and pause incremental profit growth by F19

- Pictures revenue will struggle in F18 – management thinks the bottom line will be fine, a tough test for them to pass, we worry that motion pictures revenue will dip below fixed cost levels

- Music at peak profits due to Fate/Grand Order – a fair point, but even excluding gaming profits, the music business has a growth driver in streaming, that is big enough at 30% of segment revenue to matter, growing over 25% y/y (LTM), and the division is nicely profitable even without games

- Mobile restructuring – this is inevitable (although not in current plans). We guess management will take the pain now that things are good. Expect a 150-170b Y write down in F18. Mostly cash based. Ouch. However, taking the pain now is better than waiting for it to be worse in the future, and the company's operating margin profile will improve further post restructuring.

In sum, none of these items dent the medium term trajectory of rising profits and rising FCF.

Piece by piece updates:

Pictures: we are worried, management is not

- Gross receipts for top films are now tracking flattish y/y as Spiderman box office impact recedes and there is little incremental revenue momentum

- Management believes the new slate of movies have all been built with a more disciplined budget process

- Motion Pictures is ~45% of overall Pictures revenue, which is ~12% of total consolidated Sony revenue

- Have to wonder: how much revenue downside can the segment absorb and keep in the black?

PlayStation: positive drivers in place as long winning cycle extends, large installed base provides rich 3rd party content upsell opportunity, and growing network business helps fund R&D for next consoles, keeping profits in a healthy trajectory.

Music: Grand Order is driving big incremental profits but even x-GO the division is back to m-s-d% topline growth thanks to the growth of streaming music, and h-s-d% operating margins, backing out the games impact.

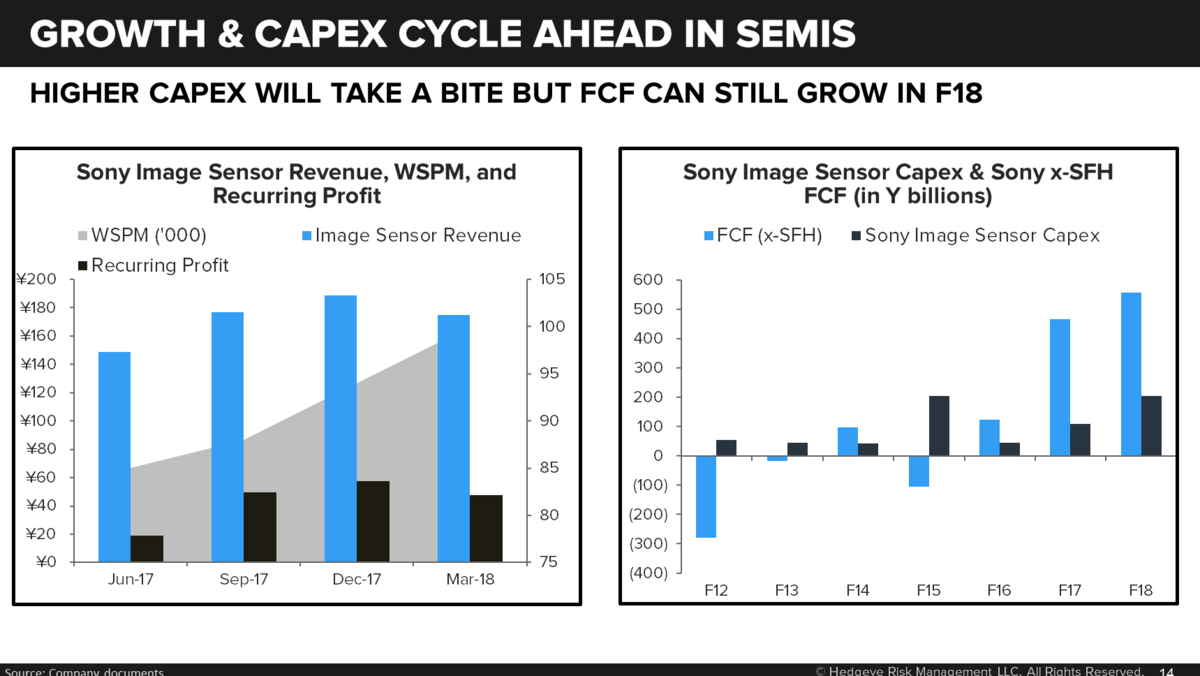

Semis: the company has line of sight to 100k WSPM by the end of March (from 88k wspm in October), implying chunky growth in the category through F2Q18 (Sep-18 Q). From there the company has ~20-30% of incremental supply growth that can be squeezed out of current fabs via efficiencies. But then that’s it. Which means that by March the company has to make a decision on another big semis capex year. Last time around this meant a ~160b Y incremental investment. Some of that seems to have already been absorbed in this year’s guided ~75b Y step up. A 90b Y increase in capex next year would hurt (425b Y trailing FCF today) but not kill F18 FCF, as F18 FCF could actually still increase next year with flattish profits and working capital reversal off F17.

Mobile: biting the bullet will cost some money. Take out your pencils: assuming a 25% gross margin, which is likely mostly variable cost by now (please), you are still netting a ~150-170b Y charge to solve out the OPEX (assuming a one year cost hit, in keeping with JP norm).

TV: TV revenue is up ~18% in 1H FY17 (y/y %) in spite of flattish units, and operating margins are a little bit better. Our data indicates the trend continues with units slightly up y/y and ASP up mid to high s-d%. The division has found a way to 'find a way', for now, and it is impressive. Without more resources or strategic focus from top management, neither of which they will get, the division will continue to at-best avoid disasters rather than be a sustainable long term force.

Netting all of this out, you have a company trading at ~14x LTM FCF, ~13x F17, and potentially ~10x F19. The company is finally being run for profits and cash flows. It is a major change in the nature of the company.