Below we draw the notable conclusions from our daily monitoring of key pricing and sentiment factors, much of them derivatives-markets based. We publish key conclusions ~monthly in cohesion with shifting conditions. Because many of our internal volatility factors shift daily, this note is intended to be a summary of process.

The message within domestic equities is more of the same: Higher highs with pockets of volatility that have led to widening implied volatility premiums on pullbacks. Volatility markets the last two weeks have been a clear-cut model for this sequencing in perceived market risk.

Other notable call-outs include an all-time high in net long crude oil from the speculative investor pool (non-commercial), continued positive sentiment in the Euro currency, upside volatility dispersion in yield-sensitive consumer staples at the sector level, and the price of volatility within the “value” component of the Russell 2000 index spent the last month creating a spread again to the “growth” component (this spread had peaked back in April).

----------

- Net Futures & Options Positioning: The Net non-commercial long position in crude oil skyrocketed to a new all-time high (aggregated futures and options positioning). Contract positioning increased +39K w/w to net long +622K contracts. The previous all-time high in net length came at the end of February 2017 (+586K).

- Yield-Sensitive Dispersion: When we refer to “dispersion”, we’re referencing the dispersion in volatility expectations for a sector relative to the broader market. The most divergent dispersion this month within U.S. equities is the spread in consumer staples (XLP) implied volatility relative to the S&P 500 (SPY). Like the short positioning in 2yr and 5yr futures contracts heading into November, consensus paid up to hedge downside in yield-sensitive staples.

- Euro Currency Sentiment (Little Marginal Change): Although the net long non-commercial futures & options position has been trimmed from the all-time highs at the beginning of September, volatility markets show that perceived downside risk in the Euro currency remains muted after shifting much more bullish on the margin coming out of French elections in April.

- Russell Factor Preferences: The market had put the largest implied volatility premiums in global macro on top of Russell 2000 and R2K factor ETF realized volatility into this week. The reality is that Russell realized volatility remains near an all-time low so the implied volatility premium expansion was anticipatory of broader market volatility. Investors who paid up for this volatility have been crushed again.

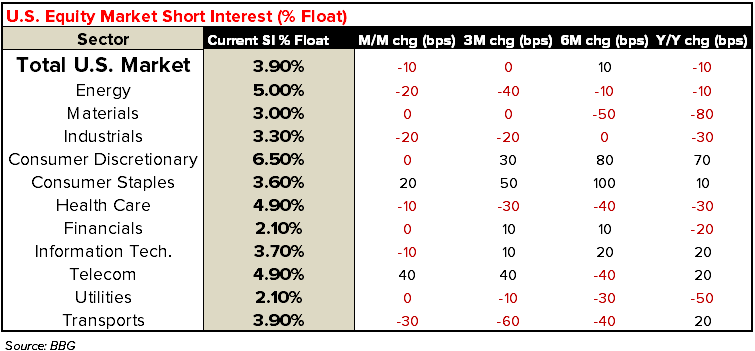

- Updated Short Interest (Telecom): Total U.S. market short-interest declined by 10bps as a percentage of float month-over-month with notable exceptions in Telecom and Consumer Staples. Short-interest in the Telecom sector increased 40bps as a percentage of float from last month.

-----------

Net Futures & Options Positioning

The Net non-commercial long position in crude oil skyrocketed to a new all-time high (aggregated futures and options positioning). Contract positioning increased +39K w/w to net long +622K contracts. The previous all-time high in net length came at the end of February 2017 (+586K).

The net short positioning in 2yr and 5yr treasury futures contracts was extended heading into November. The net short positioning in the 5yr hit an all-time high at the beginning of the month. This set-up mirrors the upside dispersion positioning we discuss below with regard to consumer staples which was at peak dispersion heading into November (still extended). The short positioning in 2yr and 5yr contracts was trimmed substantially the last 2 weeks despite the fact that the 2yr yield continues to make new cycle highs.

Investors have built up short positions in both the Yen and Swiss Franc to the point where both of these contracts have the most extended short lean across global macro (z-score). See the charts below for detail.

Yield-Sensitive Dispersion: When we refer to “dispersion”, we’re referencing the dispersion in volatility expectations for a sector relative to the broader market. The most divergent dispersion this month within U.S. equities is the spread in consumer staples (XLP) implied volatility relative to the S&P 500 (SPY). Like the short positioning in 2yr and 5yr futures contracts heading into November, consensus paid up to hedge downside in yield-sensitive staples.

As mentioned with regard to short positioning in 2yr and 5yr, the volatility dispersion in staples is now a weeks-long trend. As is typically the case, dispersion factor trends are good indicators of crowding. Since the XLP IVOL spread to SPY hit its YTD peak this month, XLP is sitting on +227bps of relative performance vs. SPY MTD.

Euro Currency Sentiment (Little Marginal Change): Although the net long non-commercial futures & options position has been trimmed substantially from the all-time highs at the beginning of September, volatility markets show that perceived downside risk in the Euro currency remains muted after shifting much more bullish on the margin coming out of French elections in April. In addition to the net long position here are a few other market-based indicators of positive sentiment:

- Skew: The price of upside vs. downside exposure in the Euro is nearly as expensive as it’s been the last 5 years (99th percentile). We show both a percentile and z-score view of the price of a risk reversal across multiple contract durations in the charts below. Ultimately the takeaway is that upside call volatility is at its most expensive point of the last 5 years relative to downside put volatility.

- Implied Volatility Premiums: Across a diverse, cross-asset screen of implied volatility premiums, the Euro ranks near the top in global macro with the largest relative implied volatility discount. A "discount" occurs when implied volatility trades below realized volatility on the same time period match (i.e. 30-Day implied vs. 30-Day realized)

- Relative Implied Volatility Premiums (vs. Major FX): Our last visual shows the implied volatility premium/discount for a basket of currencies (Dollar, Euro, Yen, Pound). We show the 60-Day window as an example, but the implied volatility discounts are largest in the Euro across durations.

Russell Factor Preferences: The market had put the largest implied volatility premiums in global macro on top of Russell 2000 and R2K factor ETF realized volatility into this week. The reality is that Russell realized volatility remains near an all-time low so the implied volatility premium expansion was anticipatory of broader market volatility. Investors who paid up for this volatility have been crushed again.

The implied volatility premium expansion set the tone for the +3.0-3.6% w/w rip for IWM, IWO, IWN. The implied volatility premium was again a telling indicator of perceived beta risk.

Just to re-iterate the divergence in “value” vs. “growth” preferences which continued yesterday with “growth” outperformance, the Russell 2000 value ETF (IWN) has also started creating this volatility spread again where implied vol trades at a premium in value vs. growth. We show this dispersion visually below.

Updated Short Interest (Telecom): Total U.S. market short-interest declined by 10bps as a percentage of float month-over-month with notable exceptions in Telecom and Consumer Staples. Short-interest in the Telecom sector increased 40bps as a percentage of float from last month.

Ben Ryan

dty