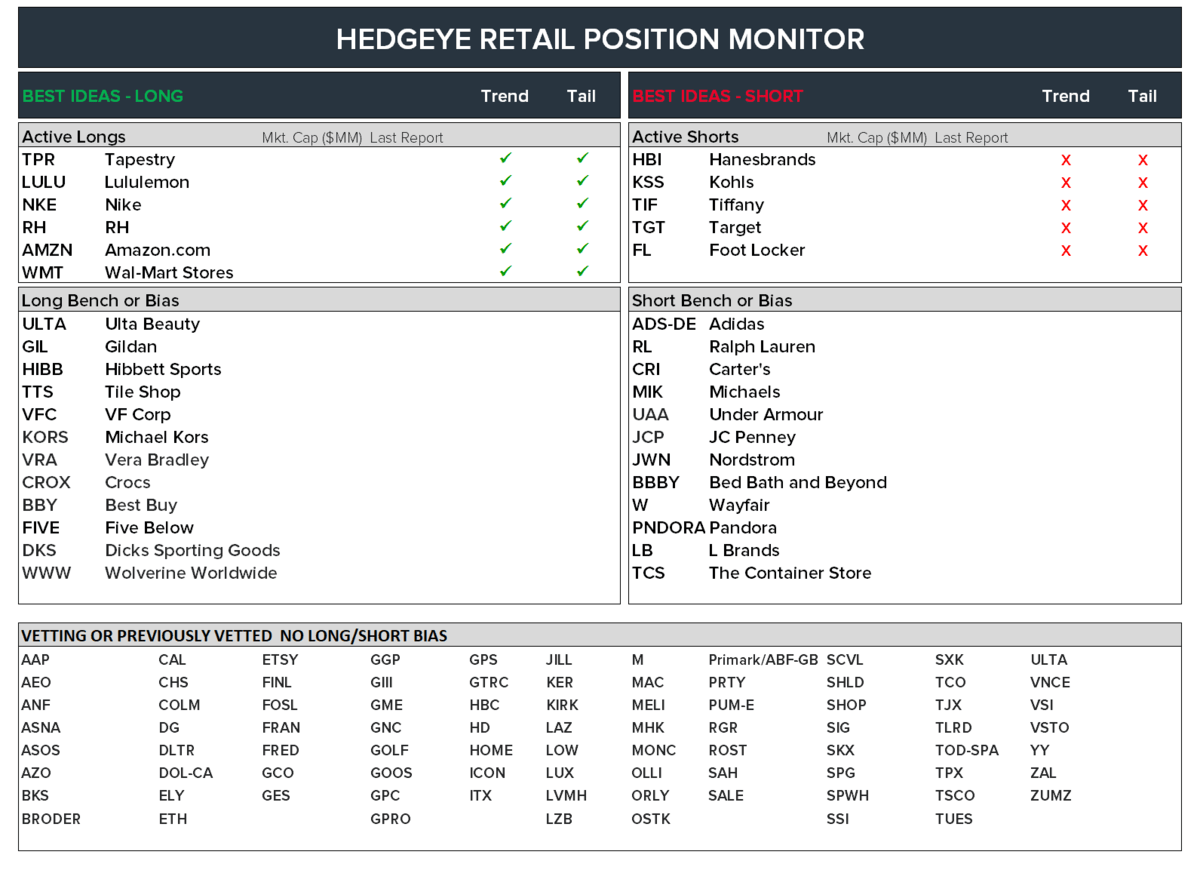

Best Idea Longs (all positive TREND and TAIL).

- TPR: More to like from this week's print than dislike. Higher synergy estimate, reasonable 2Q bar, and the sheer magnitude of license accretion is being grossly overlooked. Top long idea for YE17, and as of now, YE18 as well.

- LULU: This is nearly on par w TPR as our Best Idea Long. The factors that were bad decisions 3-years ago (Ivivva, Men’s, Int’l, No wholesale Model) were ’bad unprofitable ideas’ that have since turned into very good and increasing ROIC ideas (‘cept Ivivva – which is shuttered). Arguably need 100 Men-only stores in the US alone. No wholesale model averts the muck associated w TSA, DKS, M, JWN, etc... If CEO fails, he’s out and Glenn Murphy picks a successor – if Stefan Larssen then $4.00 EPS power comes into play. There’s your $100 stock.

- Long NKE. This is, without question, the most powerful transformational TAIL call I can find in Retail. The TREND however remains painful. Good news is that the 2Q guide is a slam dunk. Third highest conviction long after LULU.

- RH: I still contend that RH will be cheaper at $100 than at $50, $70, $90. New highs likely in 2018 – not just bc 130% of float is short, but bc new store productivity is squarely on track, which will drive the square footage/market share/white space. Analyst meeting this week. We’ll be there with bells on.

- AMZN: Though this food deliver gaffe is worse for AMZN than the inevitable data breach, the fact is that this is evolving into the biggest consumer roll-up in 20-years – until a better one comes along. The ‘steamrolled by Amazon’ buzzword is getting old and stale. The call on retail now is how brands can partner with AMZN – even at a margin and working capital hit – to save themselves after a decade’s worth of ecom underinvestment. I won’t pick a magic multiple on AMZN, but this story is evolving in a high/asset turn way that will be tough to now own. Though it has to make money at some point – lets face it.

- WMT: Biggest problem with AMZN is that it has 400 stores. It needs 4,000. WMT has 4,300. The spread between WMT and AMZN – strategically – is converging. And WMT management is better than AMZN – yes, I just said that. This is a 2-horse race, and don’t count out WMT.

Best Idea Shorts (all negative TREND and TAIL).

- HBI: 10-years of mis-aligned incentives manifest itself today in a series of revenue misses, margins going from 14% to 6-8%, cash flow downward revisions, and revaluation to 6-7x EBITDA. There’s your single digit stock. The company still has yet to accept my challenge for a public debate.

- KSS: Did three sell-side firms actually upgrade KSS this week? The Street can talk about KSS being cheap all day. But who cares about $0.03 per share in EPS from UA, when the $1.70 in credit just cracked? And that ignores the $1.25 in incremental gross profit from the people that drove credit income w COF. Also ignores the most egregious lease profile in Retail – locking in KSS to a perpetual comp melt not unlike an ice sculpture in Tuscon in August. This is a bagel.

- TIF: I have ZERO problem going against activists – especially those w such little skin in the game. Tiffany has a BIG brand problem – similar to what RL had 5-years ago – and just did not know it. Jana can put the best CEO in the game at the helm, but the reality is that this company needs brand investment, a LOT of people, and renewed success in $200-$500 entry level price points to recapture the 20-something consumer. Maybe TIF gets bought/sold? But at this over-earning margin structure and valuation to match? Maybe Jana is orchestrating some kind of deal w De Beers or some other cross-border transaction I’m not smart enough to think of. But fundamentally this is evolving into a less relevant brand with eroding economics. If it can’t comp when Gucci, Moncler, LVMH, and even the GOOSer are crushing it, then when can it? Only lux brand not getting it done is Bulgary, who’s former CEO is one of the TIF activists.

- TGT: Strong likelihood of missing 4Q due to WMT and AMZN promotions in tandem with looking $0.30 EPS hit from latent wage increase. Not sure I have a massive edge on this one. But for a mega cap with; a) weak management that b) has to (but won’t) close 20% of it’s stores, c) is unikely to ever grow again d) is inversely just as likely to miss the fourth quarter after e) anniversarying 4 qtrs of ‘better than decent’ beats, with a call option on f) doing a large dilutive deal for the CEO to save his job…I’m thinking that that in itself is all I need to know.

- FL: This Nike launch into AMZN is horrible for FL. Nike telling FL it’s a ‘small deal’, And it is until AMZN redesigns the UI to offer consumers the best shopping experience out there – in store, on line or both. As FL deleverages occupancy and SG&A I’m at $2.40 in EPS vs the Street at $4.50. DO NOT OWN THIS NAME, and pick your points in adding short side.

SHORT Bench (Negative TAIL with questionable TREND)

- Adidas, momentum is slowing – though still on fire. Momentum is from Heiner – who’s track record is simply bad. Now Rorsted is inheriting a fashion push when he’s tasked with Swiss-Engineering a German-Engineered company. TREND is clearly bullish, and maybe even the early part of our TAIL duration - -but ultimately this is Bob Eckert/AMT and or Bill Perez/NKE all over again. The management call is super ‘out of consensus’. Never met a PM that does not love ‘em.

- Ditto on RL. Brand problem bigger than TIF, and perhaps harder to fix. Louvet’s stock does not fully vest until Ralph is pushing 85 years old. P&G execs simply don’t work in a fashion business. Growth here is like a volatile and ‘more over-earning’ version of TGT.

- CRI: I’ve been short and wrong. TREND is going it’s way. I still don’t think doing a deal, moving to Canada and launching co-branded stores is a sustainable strategy when management can’t fully explain why it’s core has slowed – an otherwise very defendable business. The other half of the biz competes w everyone from Old Navy, to Nike, to WMT/ Amazon private label.

- MIK had a tough month due to #oldwall downgrade. But that downgrade is likely right, and might not be bearish enough. Model needs to exist, but not at either a) 1350 stores, or b) a 13-14% EBIT margin. One prob drives the other. At peak margins it’s already 3.2x levered. At a 9% margin, this thing earns $1.10 instead of $1.80. If $175 in productivity at a 9% margin, it’s down to $0.75 – or a buck miss. Then it’s at almost 30x earnings today instead of 9x on the Street numbers. And yeah…in that scenario MIK levers up to 5.5x.

- UAA: No way I could be bullish on this. It’s at 4-year lows, but no reason it can’t hit 5-year lows. I took this off my Best Idea short list after the implosion to $16 — w a long bias. Then I dug deeper to answer whether this is heading the way of Nike or Reebok. As of today, I’m in the Reebok camp. If this rallies on ‘hitting the quarter by accident’ I’ll likely short again without a drop to the single digits or a BIG change in the research call.

- M: -- Off my short list. We all know it’s a dinosaur, but it’s close to being at the level where it shouldn’t cut anymore stores. Mostly A and B locations with real beachfront property value. There is no way there’s a REIT call here. But if 50% of EBIT growth is driven by sporadic real estate sales, I don’t want to be short this name when it comps by accident, the street is already looking for 20% EPS decline in 2019, and 19% of the float is short.

- JCP: If there’s one thing you need to keep in mind on JCP, is that when RonJon forced JCP to get that $1.8bn loan from Goldman in April 2013, it was securitized with the owned stores that were actually worth anything. In other words, there’s no asset value folks – at least not for JCP. This is a donut – if you can find the borrow.

- PVH: Don’t like management, the company, and brand positioning outside of select parts of CK. But that’s no edge, it’s a bias. And I hate bias. I have no call here.

- JWN: Yes, JWN over-earning by 300-500bps. But this is a bigger consensus short than KSS — only the business has a reason to exist, there’s terminal value, and I have a tough time modeling a dividend cut. The deal has fallen apart and stock is near 52 week lows. I have zero edge as to why it should go lower other than the group ‘stinking’. Ruling out a LBO meaningfully de-risks the short. Moving down to Short Bench.

- Pandora (jewelry company) on bench with initial short bias. The core – or what was the core – is now a commodity. Brand not strong enough to profitably grow otherwise – espec with mismatched distribution dynamics.

- PRTY down 13% in a month, 25% yy… short worked arguably faster than the fundamentals have eroded. Taking this one off Short Side.

LONG Bench (Positive TAIL with questionable TREND)

- ULTA moved to the highest name on our Long Bench.Stock down 20% yy, down 30% in last 6mo. PE mult gone from 35x to 22x since June. It’s going through that ‘hyper growth multiple beating by a lesser magnitude re-valuation.’ But likely sub 20x on the REAL EPS number. One of the best models in retail w/ one of top 3 management teams.

- VFC: From Short to long TAIL. Kind of a mediocre conviction Long – I hate those. Management not as good as it used to be — not by a long shot. Brand portfolio is average at best with best division slowing in core market. Won’t ‘restock’ at WMT w basics. But VFC likely surprise on upside after a 6 year hiatus of not doing deals. With the best wave of new business models we’ve seen in a generation coming to market, VFC will be at the forefront? Long term targets are a stretch. But near-term expectations doable, and FX no longer a headwind.

- No Way I can still be short HIBB when Nike needs it to survive – and it will. Down to sub-$300mm in cap. Good luck being short that – along w the 20% of the float that is betting on a BK.

- CROX on long bench — research continuing with a long bias, but early enough that I could easily come out other side. I can’t believe I’m actually looking at this name again.

- TTS on Long Bench. Gotten smoked, but it’s a good concept w a clear competitive advantage. Did the right thing in clearing out inventory in 3Q. People are throwing this away with the likes of TCS (container store). It’s 100% not.

- FIVE Added to bench. Risk on the quarter is low, and can’t make a valuation call on a company that can triple it’s store base without blinking an eye.

- I can’t believe i’m saying this, buy KORS is higher on vetting list despite move last week (I already turned incrementally bullish two weeks ago and wasn’t fast enough in vetting it further). The ‘space’ is flip flopping with athletic — i.e. athletic been solid for 5-years while accessories are in the tank. I think we’ve got the opposite today. Choo deal was expensive, but should work. If I’m as right as I think I’ll be on COH long, KORS ain’t going down.

- VRA: I don’t make ‘getting bought’ calls (except KATE) but like KATE, this individual business is likely worth buying – if you can go micro cap.

AAP is down ~45% yy. Auto is on the top of the vetting list, work being done here. We should have some great survey data re AMZN/Customer Type/FICO/Market. We’ll clearly get some good conclusions – just no sure which side. ORLY, AAP, AZO.

StitchFix on vetting list. No such thing as a ‘long vs short’ vetting list’. We’re vetting it and will have a deck out this week ahead of pricing. Deal prices Thursday. We have a deck and Presentation this coming Monday.