PCLN

The street appears to be grasping for a narrative following PCLN's 3rd consecutive miss on its room-night (RN) guide; the two prevailing themes are 1) PCLN is facing emerging structural industry headwinds and/or 2) PCLN is impeding its own RN growth by shifting ad budget away from performance marketing toward brand advertising. On the first point; the only structural headwind is that the sell-side hasn't given PCLN any breathing room in its guide since they don't understand the law of large numbers. On the second point, PCLN is just increasing its brand advertising mix after pulling back there in 2H16. Further, PCLN doesn't appear to be pulling back on performance marketing in aggregate, just on meta. For context, the slowdown in PCLN's performance marketing spend in 3Q17 is comparable to the slowdown in TRVG's net revenue growth (both in $ terms); ~85% of which came from PCLN in the L9M. Combine that with the deceleration TRIP saw in its referral revenue growth, and it appears that PCLN is just allocating more of its performance-based spend to SEM (e.g. Google). In short, the new narrative is just noise. We're in the process of vetting consensus 2018 RN estimates; maybe they'll finally let us in next year.

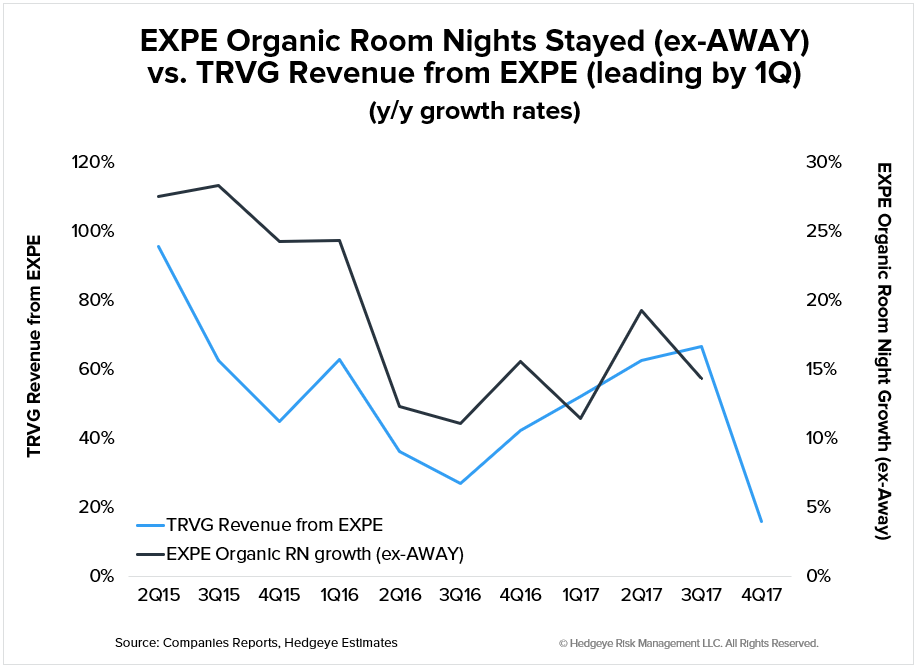

TRVG

TRVG's model is now structurally defunct now that PCLN is pulling away. The two central tenets of our analysis of its model 1) TRVG is hostage to PCLN & EXPE and 2) its inventory is tethered to its ad spend. TRVG's 3Q17 results confirm that PCLN has started pulling back on Trivago ad spend, so TRVG can't continue to acquire (pay for) traffic at aggressive rates since it's won't know how much of it would be able to resell (PCLN represented over 70% of its net revenues in T9M). Further, TRVG suggested the 3Q17 pressure came in the form of CPC rates, so for all we know PCLN is now bidding less for TRVG's traffic than what TRVG has to bid to acquire it. Note that this dynamic creates a downward spiral (for lack of a better term) since TRVG's ad budget/inventory is ultimately funded by the revenues it collects in the preceding quarters. So if PCLN is paring back its ad spend, then TRVG may not have the budget to drive inventory growth in subsequent quarters, and so on so forth…

TRIP

TRIP's issues are more self-inflicted as opposed to TRVG’s which are almost exclusively out of their control (i.e. PCLN). We learned off that last print that mgmt sharply pivoted on its 2017 objective from maximizing revenue growth to managing toward EBITDA instead. In turn, TRIP chose to fund its TV ad budget by cannibalizing its online ad budget rather than putting its EBITDA to work. But in doing so, TRIP shifted the mix of its traffic toward mobile (couch surfers) rather than desktop (legitimate hotel shoppers); leading to heightened pressure in revenue per hotel shopper (RPS) since OTAs bid less for the former as it monetizes at a fraction of the desktop rate. Further, it appears that dynamic is getting worse since its online ad spend appears to have declined in 3Q17, leading to slowing growth in total hotel shoppers, which mgmt suggested is now running flat y/y as of October. Mgmt expects this dynamic to continue through 1H18 (i.e. until it comps past the introduction of its TV campaign). But note that TRIP isn't immune from the PCLN meta headwind either; the deceleration in its RPS growth is greater than what would have been expected by its mobile shopper mix (comparable to 2Q17 levels), suggesting PCLN is bidding less for TRIP's ad inventory as well. TRIP is dead money at best for the time being.

EXPE

EXPE used the 3Q print to bring down 2018 expectations. It suggested AWAY EBITDA was going to be lower than the $350M target it had set out when it acquired it, and alluded to total 2018 EBITDA growth in the low-teens range. The one area where EXPE didn't rebase expectations was on room-nights, in fact almost alluded to the improving trends since it expects to invest heavier in performance marketing next year. However, there are a few problems there. 1) EXPE is also planning to beef up marketing spend around AWAY, which in itself may become increasingly reliant on customer acquisition to drive booking growth now that AWAY is in the later inning of model migration. For context, AWAY's 1.5M online bookable listings is greater than the number of total listings it had when it was acquired. 2) We also have to consider that TRVG may not remain a source of room-nights growth for EXPE since TRVG can't continue to aggressively acquire traffic (inventory) now that PCLN has lost its appetite for it. 3) EXPE may be facing increasing competition for room nights since PCLN may be accelerating its performance-based ad spend as well (see PCLN bullet). Ultimately, EXPE could be facing single-digit RN growth rather than the low- to mid-teens that consensus is expecting through 2018.

Let us know if you have any questions.

Hesham Shaaban, CFA

Managing Director

@HedgeyeInternet

Todd Jordan

Managing Director

@HedgeyeSnakeye

Sean Jenkins

Associate