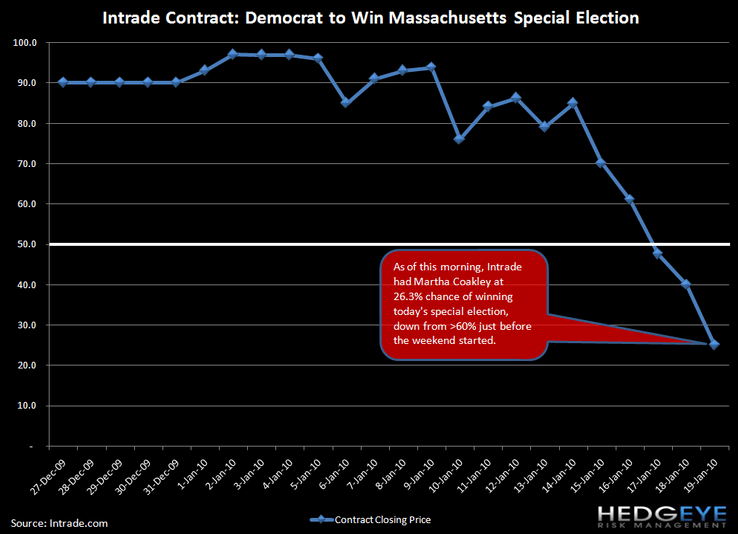

While tight elections are always just that - tight - we thought it was worthwhile to point out that over the weekend the Intrade contract on this election sank like a stone. The expectations that Democratic candidate Martha Coakley will win fell from over 60% going into the weekend to 23.6% this morning.

As our prior post explains, the outcome of the Massachusetts Special Election has significant ramifications for the performance of the Financials sector, as it will likely play a major role in determining the outcome of Financial regulatory reform.

Joshua Steiner, CFA

Financials