Greece continues to make headlines this morning—the European Commission said in a report today that “severe irregularities” exist in the nation’s statistical data, which put into question the reliability of the previously released government deficit figure of 12.7% of GDP.

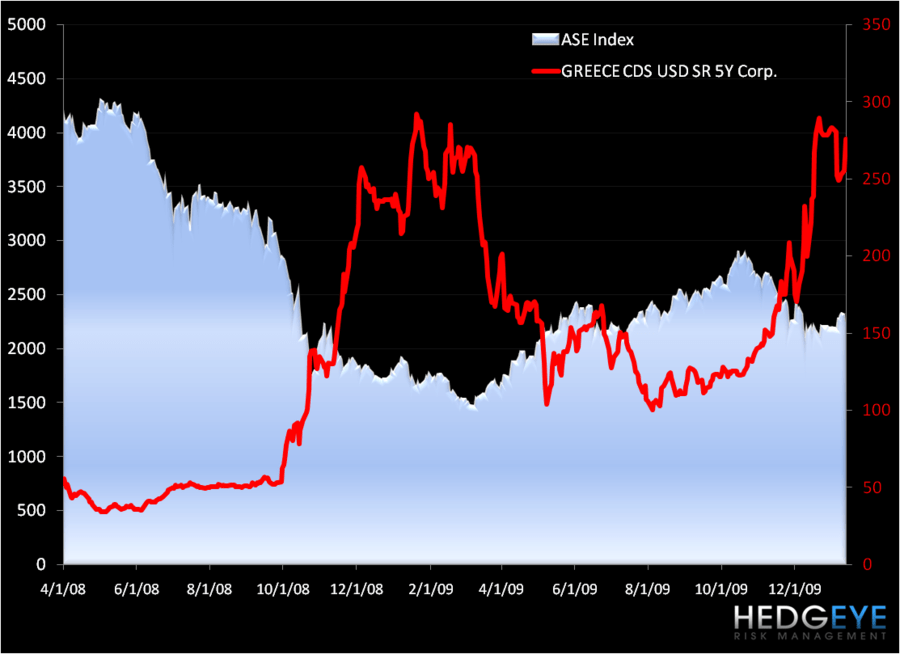

As the credibility in Prime Minister George Papandreou’s government continues to crumble, we’re seeing (and as expected) CDS run up, and the equity market tick down, while Greek bonds fall as investor demand increased yield. The spread between the Greek 10-year Bond and the German Bund blew out another 17bps today to 233bps (see charts below).

As Keith noted in his Early Look “Roll On” this morning, we’re seeing massive amounts of sovereign debt being rolled out globally. As countries refinance their debt, we’ll have our EYE on those that are simply finding near-term solutions rather than practical longer-term ones to repair their financing cracks and, in some cases, craters. Certainly, the inability of governments to pay off debt obligations is a credible threat, one we could see in the near term if supply outstrips demand despite compelling yields.

Matthew Hedrick

Analyst