While a worse-than-expected 85,000 decline in December nonfarm payrolls weighed briefly on recovery expectations, the S&P finished higher by 0.29% on Friday, closing up 2.68% for the week. Volume declined 16% day over day, so the move on Friday was less convincing; breadth was also week on the day.

ON the MACRO front, nonfarm payrolls fell 85,000 in December vs. consensus expectations for an unchanged reading. However, November payrolls were revised to reflect a 4K gain vs. an originally reported decline of 11K. As expected, the unemployment rate held steady at 10% (largely due to a drop in the participation rate), while the 0.2% gain in average hourly earnings was also in line with the consensus. In general there were not many good things payroll to report.

On Friday the Financials (XLF) were the worst performing sector after rallying sharply for the balance of the week. The banking group (BKX) fell for the first time on Friday, declining (0.2%). The weaker-than-expected December employment report may have spurred some profit-taking in the XLF.

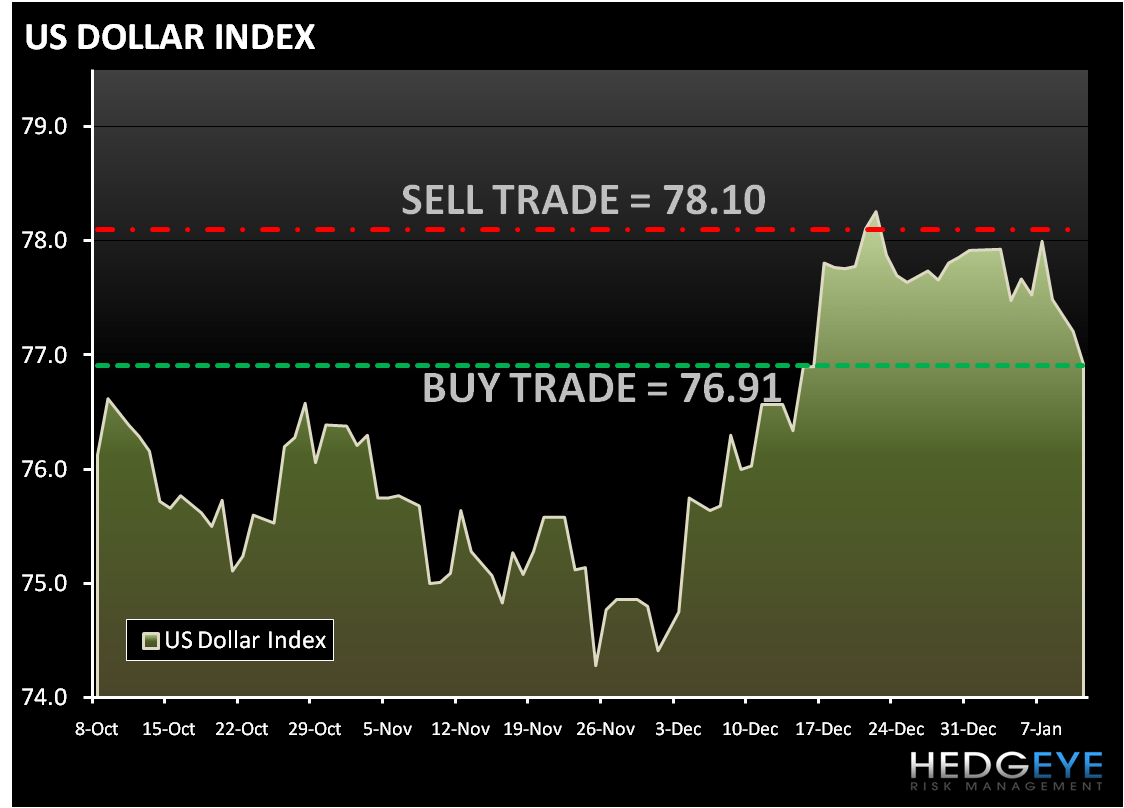

Despite some weakness in the dollar the CRB was basically unchanged on the day. The cold weather helped Orange Juice move up 7%, followed by Copper up 2.1%, Silver up 1.6% and Gold up 1.6%.

The best performing sector was the Industrial (XLI), rising 1.6% on the day. The RECOVERY trade got a lift from upwardly revised Q4 guidance from UPS +4.8%, and continued strength in recovery-leveraged pockets of the market such as steel, aluminum, copper, machinery and multi-industry/conglomerate stocks - GE was up 9.7% last week.

The dampened risk aversion trade was evidenced by last week’s move in the VIX. The VIX declined 4.7% on Friday and declined every day last week (the S&P 500 was up every day last week); and a bullish steepening move in Treasuries reflecting a pushback in tightening expectations.

The Technology (XLF) sector snapped a three-day losing streak on Friday, although the move was without much fanfare. The semis were among the best performers with the SOX +1.5%. Additionally, the memory names resumed their upside trajectory with SNDK up 2.5% and MU up 2.4%.

The range for the S&P 500 is 17 points or 0.4% (1,149) upside and 1.0% (1,132) downside. At the time of writing the major market futures are trading slightly higher.

In early trading today Copper climbed for the first time in two days as a surge in Chinese imports boosted optimism that a global economic revival is under way. The Research Edge Quant models have the following levels for COPPER – buy Trade (3.38) and Sell Trade (3.50).

In early trading today Gold is up for the second day in a row on the back of a weak dollar. The Research Edge Quant models have the following levels for GOLD – buy Trade (1,115) and Sell Trade (1,156).

In early trading Crude oil is trading up 1% to $83.56 a barrel. Last week oil rose 4.2% and has been up for 4 weeks in a row. The Research Edge Quant models have the following levels for OIL – buy Trade (80.91) and Sell Trade (84.34).

Howard Penney

Managing Director