The Federal Reserve left interest rates unchanged on Wednesday. As expected, the central bank also announced it will begin to let assets, like Treasuries and mortgage-backed securities purchased under its quantitative easing program, roll off its $4.5 trillion balance sheet. This will begin in October.

All of this has been carefully telegraphed and covered in reporting yesterday. What the media missed, however, was the Fed's abysmal forecasting track record. Our research shows that Fed forecasts are wrong about 70% of the time.

Meanwhile, for the better part of 9 months now we've been telling subscribers that U.S. economic growth is accelerating. In February, we warned that inflation is slowing alongside the U.S. growth acceleration (called "QUAD1" in our four quadrant Growth, Inflation, Policy model).

Investing Implications

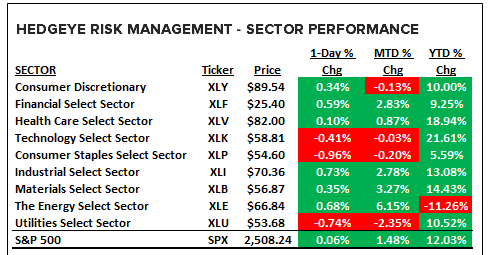

This outlook has been driving financial market returns, and our favorite investing conclusions, for some time now. We've been saying buy assets most tethered to an uptick in U.S. consumption, Tech shares, and stay away from assets tied to falling inflation, Energy shares. That's working in the year-to-date:

- Technology (XLK): +21.6% year-to-date

- Energy (XLE): -11.3% year-to-date

THE FED (FINALLY) STARTING TO AGREE WITH HEDGEYE

Here's Hedgeye CEO Keith McCullough writing in today's Early Look and recounting what happened to the Fed's forecasts yesterday:

|

First, let’s review the “incoming-data” that changed Janet Yellen’s Fed forecasts, on delay:

Yep, nice and linear and tidy – 20 basis points up here, 20 basis points down there – and, voila, you generate a REAL growth surprise to the Fed’s prior REAL growth forecast. |

Bottom Line

The Fed is finally getting in line with the Hedgeye Macro view, even if they are 6-7 months late. Better late than never.