|

"For the first time in a decade, the world's major economies are growing in sync, a result of lingering low-interest-rate stimulus from central banks and the gradual fading of crises that over years ricocheted from the U.S. to Greece, Brazil and beyond." |

That's from a Wall Street Journal article published in late August. Translation? The global central planners have fixed everything. But aside from U.S. growth, which bottomed in the second quarter of 2016 and continues to accelerate, the outlook for China and Europe looks particularly disconcerting.

Here's why...

EUROPE Slowing

In sharp contrast to the 4.2% year-over-year Retail Sales growth in the U.S., here's a smattering of recent European growth slowing data:

- Swiss GDP came in at 0.3% in Q217 = lowest rate of change since 2009

- Italian Retail Sales came in at 0.00% y/y (those are zeroes) in July vs. +1.5% in June

- France’s Retail PMI dropped down to test “contraction” zone at 50.4 in August vs. 54.1 in July

You see, because countries like Spain, Italy, France, etc. don’t have sustainable real growth, they really only have cyclical hopes of the illusion of growth (commonly called central bank manufactured inflation).

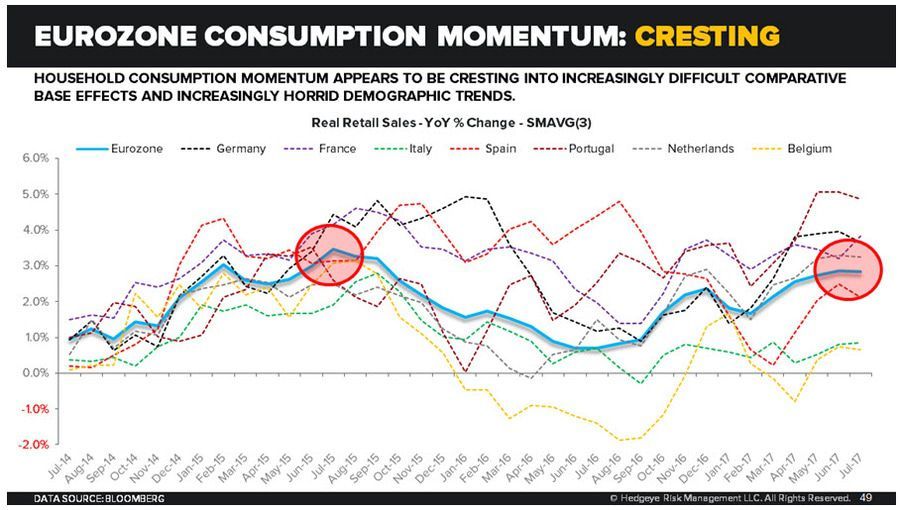

After about three years of accelerating growth, Europe is bumping up against some tough number in reporting year-over-year growth. Just look at the European retail sales chart below. Add in Europe's slow moving economic disaster and forget about it.

China Slowing

And now China... the economy is slowing. Below are some key data points to watch:

- Chinese property prices continue to disinflate. Average House Prices – Tier 1 Cities: 8.4% YoY vs. 10.0% in JUN

- Amid the real slowing, the PBoC pumped a net +470B yuan into the mainland financial sector last month.

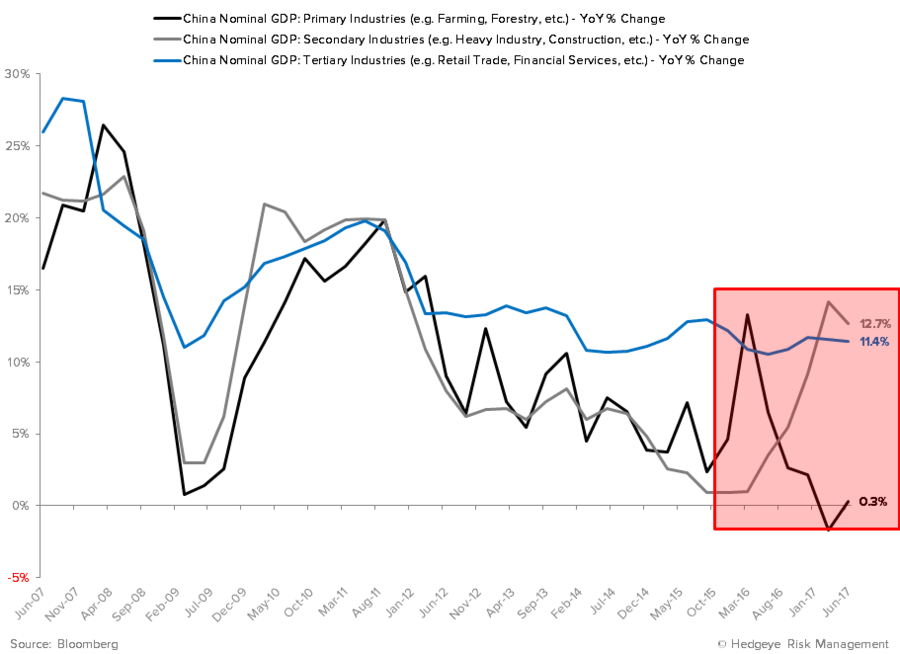

- While GDP held steady at +6.9% year-over-year growth, the manufacturing sector decelerated from its Q1 cycle-peak of +14.2% year-over-year to +12.7% year-over-year in the Q2 of 2017.

While this seems trivial, the manufacturing sector’s trailing twelve month contribution to broader Chinese economic growth remains at an historically unsustainable rate of 46.5%, versus a trailing 10-year average of 34.8%, writes Hedgeye Senior Macro analyst Darius Dale.

Bottom Line

Does this seem like global economies are "growing in sync"? We're sticking with our call for U.S. growth to continue to accelerate.