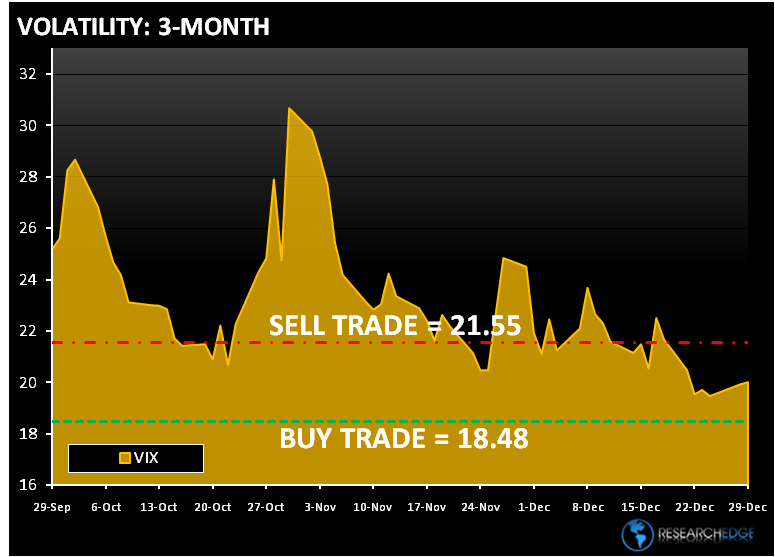

Yesterday, the S&P 500 finished the day with a modest loss, the first one is six days. Again, the internals of the market continue to be characterized by very low volume and volatility trading near the lows for the year. The Dollar index traded up 0.14% yesterday and is trading higher again today.

Yesterday, five of the S&P 500 sectors declined, while four advanced. Of the sectors that outperformed, Consumer Discretionary (XLY) was the best performing, followed by Industrials (XLI) and Consumer Staples (XLP). The XLY and the XLP outperformed on media reports that retail spending held up well during the holiday season and the December consumer confidence reading at 52.9, which was in line with consensus at 53; the November reading was revised upward to 50.6 from 49.5. It should be noted that after the close the ABC consumer confidence number ticked down to -44 from -42 the week before.

With most people out for the holidays no one seems to be paying attention to the fact that yesterday October home price data from Case-Shiller reported the first outright home price decline in six months. The October Case-Shiller was 146.58, roughly in line with the 147 consensus and down 7.28% year-over-year and down from 146.65 last month.

The Airlines continue to be the big losers, with the XAL down 2.2% over the past two days.

The range for the S&P 500 is 21 points or 1.0% upside and 1.0% downside. At the time of writing the major market futures are slightly lower. There appears to be very little corporate news again today. On the MACRO front, MBA Mortgage Applications are due at 7ET; December Chicago PMI is estimated to be 55.1 versus the last reading of 56.1 and the DOE crude oil inventories are to be released at 10:30.

The Asian markets are trading mixed, with China up on a report that new loans in Dec will increase month-to-month. The European markets are trading lower on the day on very light volume

Crude oil is trading higher for a sixth day on the belief that U.S. stockpiles are shrinking, while unrest in Iran sows concerns of a supply disruption. According to analysts, U.S. crude inventories are expected to decline by 1.85 million barrels last week, according to a Bloomberg survey. The Research Edge Quant models have the following levels for OIL – buy Trade (75.37) and Sell Trade (79.91).

Gold fell to a one-week low in London on speculation U.S. economic growth will curb demand. The Research Edge Quant models have the following levels for GOLD – buy Trade ($1,071) and Sell Trade ($1,147).

Copper rose for a fourth day in London to the highest price in almost 16 months. Today, Copper is trading higher on speculation that supplies from Chile, the world’s largest producer, may be disrupted by a mine strike. The Research Edge Quant models have the following levels for COPPER – buy Trade (3.21) and Sell Trade (3.36).

Howard Penney

Managing Director