MARKET WATCH: What’s Happening? Amazon has entered the grocery market in earnest with its recent acquisition of Whole Foods. Walmart is making deals on Amazon’s turf by scaling up its own e-commerce operations. But which company has the upper hand?

Our Take: While investors are siding with Amazon, it will be a closer battle than most people think. Walmart is larger, more profitable, starting to compete with Amazon online—and is a vastly better value. Moreover, the Millennial shoppers whom everyone assumes are pro-Amazon actually hold Walmart in equally high regard.

Amazon turned heads last month when it acquired Whole Foods for a lofty $13.7 billion. On the exact same day, Walmart made a deal that flew under the radar: The Bentonville-based giant bought men’s clothing e-tailer Bonobos for $310 million.

The timing is no coincidence: As the de facto leaders of U.S. retail, Amazon and Walmart are each spending heavily in an attempt to unseat the other.

Amazon’s Whole Foods deal has been widely interpreted as a defensive move against Walmart’s thriving grocery business. Amazon, however, is also playing offense. The company is going after Walmart’s predominately lower-income customer base by offering a discounted Amazon Prime membership ($5.99/month, down from the sticker price of $10.99/month) to U.S. consumers who obtain government assistance with cards that are typically used for food stamps. (Walmart generated $13 billion in sales last year from consumers on SNAP.)

Walmart, meanwhile, has been even more aggressive. It all started when Walmart bought e-commerce firm Jet.com for $3.3 billion back in 2016. Since then, the company has added several e-tail brands to its portfolio, including online shoe retailer Shoebuy, outdoor retailer Moosejaw, and women’s apparel brand Modcloth.

The company has gone further than merely buying e-commerce upstarts. Walmart is also revamping its delivery logistics: The company earlier this year rolled out free two-day shipping for all orders over $35 (a deal that Amazon soon one-upped), and is testing a pilot program that pays workers overtime for delivering packages on their commute home. Walmart is even barring some prospective tech vendors from building apps on Amazon’s cloud, Amazon Web Services (AWS), instead pushing them toward competing cloud services like Microsoft Azure. There’s more: For-hire truck drivers that do business with Walmart reportedly are being told that they cannot haul Amazon goods on the side.

Each company has scored some direct hits in these opening skirmishes. But which one is positioned to win the war? Let’s examine.

AMAZON: STRENGTHS

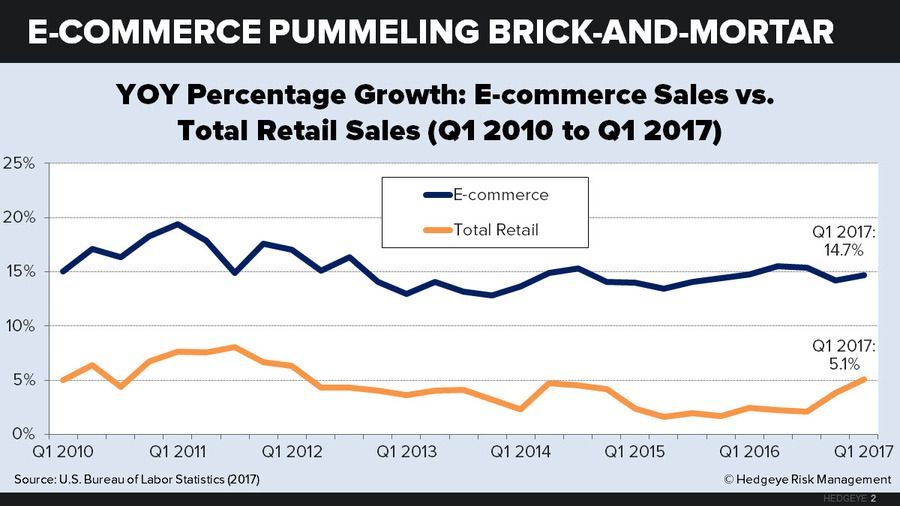

E-commerce domination. Amazon is miles ahead of the pack when it comes to e-commerce—which sets the firm apart in an era when ever-more sales are moving online.

Since 2010, U.S. e-commerce sales have more than doubled as a share of all sales. While retail has been plodding along at a modest clip since the end of the Great Recession (average YOY growth since Q1 2010: 4.3%), e-commerce sales have been skyrocketing (15.2%).

As the clear e-commerce leader, Amazon has been the largest beneficiary of this growth: Nearly half (43%) of all U.S. online retail sales take place on Amazon.com, according to retail consultancy Slice Intelligence.

One key ingredient to this success has been Prime, which now tallies 66 million subscribers—equal to roughly one in five U.S. consumers. For $99/year, consumers can get access to everything from exclusive product deals to unlimited video streaming to one-hour meal delivery. This impressive array of services, now augmented by Echo, Dash buttons, and the like, is becoming a virtual presence in many homes. These services incentivize consumers to become habitual Amazon shoppers.

Where’d that come from? Along the way, Amazon is using its massive scale to build new tech-enabled businesses seemingly from scratch.

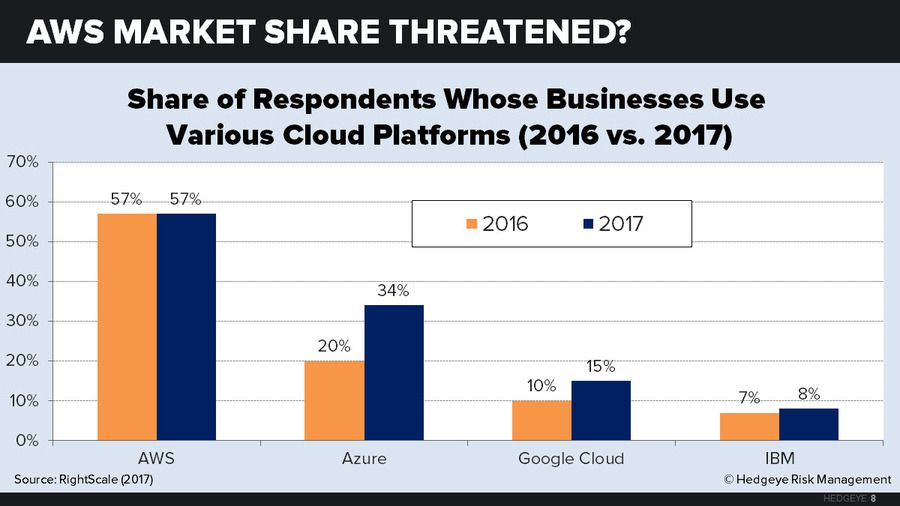

Take cloud computing. In a few short years, Amazon has transformed from a cloud newcomer to the unquestioned market leader. According to a recent survey by cloud provider RightScale, 57% of respondents say that their business is currently running applications in AWS, far ahead of the next-closest service (Microsoft Azure, at 34%).

Cloud computing is just one of Amazon’s many nascent markets. Its home remodeling platform, Amazon Home Services, hosts thousands of construction professionals who can do everything from fix a burst pipe to remodel your kitchen. Amazon is poised to spend $4.5 billion on Amazon Video this year in an attempt to catch up to Netflix. Even its warehouses are bona fide revenue drivers: In 2012, Amazon began renting out its excess warehouse capacity.

Think that markets don’t care about all of these “moonshots”? Best Buy stock recently dropped 6% in a single day on the announcement that Amazon was rolling out its own “Geek Squad” that will set up gadgets in consumers’ homes.

AMAZON: WEAKNESSES

Show me the money. But for all of its success, Amazon has yet to generate much in the way of actual profits.

Amazon cultists insist that Jeff Bezos’ long game has never been about near-term profits, but rather about keeping prices low in order to steadily gain market share—that is, grow faster than its competitors. Clearly, given the company’s insane P/E ratio of 187.8 and its stock price of $1,000-plus per share, investors are on board with this strategy—betting that Bezos will someday choose to earn a hefty profit.

But such a massive bet on deferred earnings is fraught with downside risk.

Let’s use Walmart as a comparison. With a culture of offering the lowest prices around, Walmart is hardly a high-margin profiteer. Its pretax margin is just 4.2%. But that figure is still far and above the 2.9% that Amazon earns in profit on every dollar generated in revenue.

What's more, Amazon is generating way less revenue to begin with: The company makes barely over one-quarter of Walmart’s total revenue ($136.0 billion in 2016, compared to Walmart’s $482.1 billion). Thus, even if Amazon’s 22% YOY revenue growth rate keeps up and the company becomes as massive as Walmart sometime within the next decade, it still will be generating less profit. In fact, keeping margins constant, Amazon would have to grow five and a half times larger than it is today just to generate the profit that Walmart already generates. So even assuming no slowdown in the Amazon juggernaut, it would have to wait nine years to reach profit parity with Walmart.

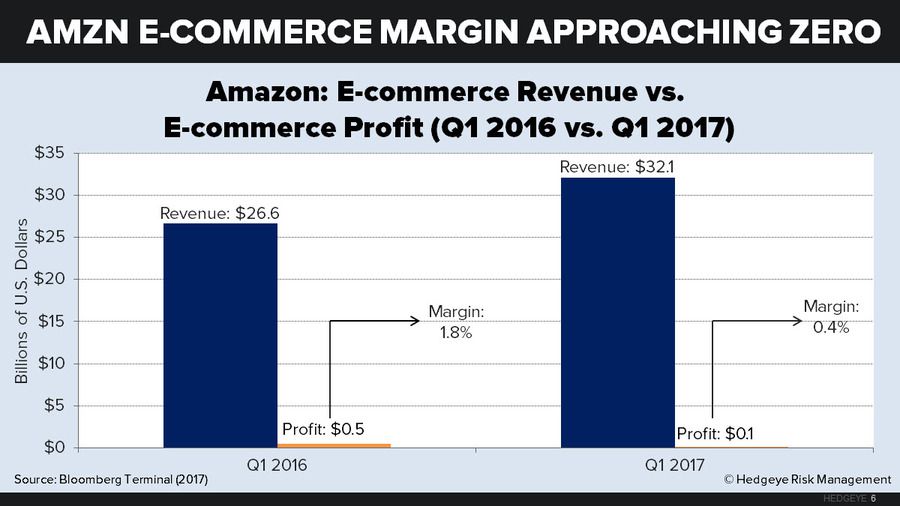

And that’s the optimistic case. If Amazon’s e-commerce operations are to be the company’s main growth driver in the years to come—as most people expect—the timeline will be even longer. This is because Amazon makes only one-quarter of its profits from e-commerce, generating almost no margin in the process (1.8% e-commerce operating margin in Q1 2016, down to 0.4% in Q1 2017). At Amazon’s current rate of growth, how long would it take for its e-commerce profits to match Walmart’s total profits? A bit more than 20 years.

Struggle to grow profit margins. All this should make clear that Amazon’s valuation crucially depends upon the firm being able to grow its profit margin substantially in the not-too-distant future without losing market share. But is that a reasonable expectation?

Amazon is pushing its suppliers on cost just about as hard as it can—and, like Walmart, getting a nasty reputation for it. As for price, there may not be much room to hike. Domestically, it faces a challenge not only from low prices on Walmart’s surging e-commerce division, but also from Apple—#2 in total U.S. e-commerce sales—which is now seeing its Apple Pay catch fire in the cutting-edge world of online mobile payment. Indeed, as we have pointed out before (see: “Apple Leads the Charge in Cashless Payments”), Apple may soon throw its sizable war chest behind Apple Pay.

Globally, Amazon’s prospects will be challenged by Alibaba, which now dominates Chinese e-commerce (57% of all sales). Amazon (stuck at 1% of sales) will likely never be allowed to close the gap. What’s more, Alibaba is now moving out across the demographically promising South and East Asian markets. Jack Ma denies any plan to compete against Amazon on Bezos’ own turf. But the strategic imperative may be inexorable. While AliExpress (Alibaba’s global B2C website) is nowhere up to Amazon in service quality, it soundly beats Amazon on price across a wide variety of products. Europe has been friendlier for Amazon, but if its sales grow much larger, it will have a tough time passing muster with European antitrust regulators, as companies like Google can attest.

Other profit centers? Some Amazon optimists say Bezos’ hidden trump card lies in all the new businesses he is creating. Surely, one of them will catch fire even if the core e-commerce business does not. Let’s pass over the outliers—like home services (little proven scalability) or media content (lately, a supply-glutted business).

The obvious candidate is Amazon’s highly successful cloud computing business—which alone generated 89% of Amazon’s total operating income in Q1 2017. But AWS still accounts for less than 10% of Amazon’s total revenue—and there’s no way that the segment will keep growing 58% annually as it has over the past three years, especially considering the rising level of competition posed by services such as Microsoft Azure and Google Cloud. In fact, Amazon’s cloud market share may already be plateauing: RightScale’s cloud survey shows that the share of survey respondents whose businesses use Azure has jumped by 14 percentage points since last year. AWS has shown zero growth over that period.

WALMART: STRENGTHS

So what’s the argument for Walmart?

A combination of size, profitability, and affordability. First, Walmart is still a much larger company, with revenues of nearly half a trillion dollars—nearly four times Amazon’s. That scale alone enables it to put a much bigger squeeze on suppliers than Jeff Bezos. Consider that, during the latest Amazon Prime Day, Walmart was able to offer many of the lowest prices around.

Second, Walmart generates a large profit—and generates it today. Its 4.7% pretax margins translate into $32.8 billion in EBITDA. No bet on deferred earnings is necessary here.

Third, with a P/E ratio of 17.0, Walmart is a better value proposition than the majority of the S&P 500 (average P/E of 21.6). The company is also a reliable dividend machine: Walmart plans to pay out dividends of $2.04 per share in 2018, marking the 44th consecutive year of dividend growth.

Brick-and-mortar domination. Walmart’s main revenue driver is its brick-and-mortar retail business, which continues to gain steam amid a collapsing retail space.

According to Credit Suisse, 2,800 U.S. brick-and-mortar retail stores closed up shop in Q1 2017, a record full-year pace. Commercial real estate firm CoStar reports that U.S. retailers must eliminate 1 million square feet of brick-and-mortar space just to grow their sales per square foot back to where it was a decade ago.

In this low-margin environment, cost efficiency is key—and nobody does cost efficiency better than Walmart, a company that uses its clout to negotiate favorable deals with suppliers and finance its “Everyday Low Prices.” The company recently told suppliers that it wants to offer the lowest price on 80% of the products that it sells, a feat that would require some suppliers to shave 15% off of their rates—or more. While many suppliers will likely drag their feet, most will eventually acquiesce. After all, this is the way that Walmart has always done business.

This frugality has clearly paid off. While mall anchors like Macy’s and JC Penney continue to announce store closures and scale back their brick-and-mortar presence, Walmart plans to add 10,000 retail jobs and 59 new/renovated properties by the end of the fiscal year.

WALMART: WEAKNESSES

Cultural handicap. For all of its size, Walmart has managed to keep its distinct small-town identity intact. The company was founded—and still keeps its headquarters—in Bentonville, Arkansas, a city with a population of less than 50,000. What’s more, Walmart’s operating philosophy has not changed in the half-century that it has been in business: Methodically acquire physical scale, eschew any cost that doesn’t add value to the consumer, and use that scale and efficiency to grind out the highest profit.

But Walmart’s culture is self-defeating in two ways. First, its management may not be capable of thinking and operating like a fast-acting, dynamic Silicon Valley tech giant. For all of its e-commerce dealings, Walmart retains plenty of long-tenured C-suiters who don’t want the company to abandon the strategy that made it into a global leader. Retail expert Mark Cohen is bearish on Walmart’s about-face for this very reason: “You’re talking about the changing of the tide, and not just from the product development point of view. Walmart has thousands of stores and thousands of people.”

Second, critics say that a 50-plus-year reputation as small-town penny-pinchers may prove to be a fatal handicap in attracting young, hip, tech-savvy new consumers. People simply don’t associate a brand built on old-economy principles with the digital, networked America of the twenty-first century. Aren’t Walmart’s handful of e-commerce acquisitions just a phony add on?

Thin brick-and-mortar margins. Unlike Amazon, Walmart doesn’t have an alternative business line to lean on if the whole retail sector flatlines.

Perhaps no sector is being hit harder by narrowing margins than the U.S. grocery business. Walmart in many ways was the first company to commoditize groceries—but new competitors from abroad are going to squeeze the margins even tighter. German discount chain Lidl recently opened its first U.S. outposts, and its fellow German competitor Aldi is planning a massive $5 billion, 900-store U.S. expansion. This could be bad news for Walmart, whose U.K. arm, Asda, has already been sidelined by these German giants. In fact, Asda has been the worst-performing U.K. supermarket brand over the past two years.

Amazon’s Whole Foods acquisition will further turn up the heat, joining a brand known for the kind of high-quality fare that today’s consumers want with a company that has huge expertise in scaling up and acquiring a customer base. Of course, it bears mentioning that middle-market firms like Target will likely be hit harder than Walmart.

In reality, groceries are a bellwether for brick-and-mortar retail in general, where (as discussed above) store closures are poised to hit new highs as “retail Armageddon” continues to wreak havoc on company bottom lines. This doomsday scenario, in which brick and mortar is ground zero, hurts Walmart more than it hurts Amazon.

CHOOSING A WINNER

So what does the future hold? Amazon certainly has the look and feel of a winner in the digital age. The company epitomizes a blue-zone, mold-breaking, Silicon Valley mindset. Its leaders aren’t afraid to spend big today to solve tomorrow’s problems. Walmart, on the other hand, was founded in the deep-red, lower-middle class Bentonville, and was built upon the paradigm of extreme cost cutting—a philosophy of scarcity, not abundance. This is hardly the type of company that inspires praise as a forward-thinking leader.

But this line of thinking may be off the mark.

Walmart’s path forward may be easier. For one, the recent moves of Amazon and Walmart indicate that each sees the ideal retail format as a blend of online and brick-and-mortar. As TechCrunch columnist Sarah Perez correctly notes, “Amazon wants to become Walmart before Walmart can become Amazon.” Yet the fact is that it may be easier—and cheaper—for Walmart to become Amazon than the other way around.

The difference between acquiring tech know-how and acquiring a massive presence on the ground is a huge one. And Walmart has already shown that it is committed to the former. One of the biggest drivers behind the Jet.com purchase was not the company itself—but the expertise. That’s why Walmart promptly installed former Jet.com CEO Marc Lore as the president and CEO of Walmart’s U.S. e-commerce arm.

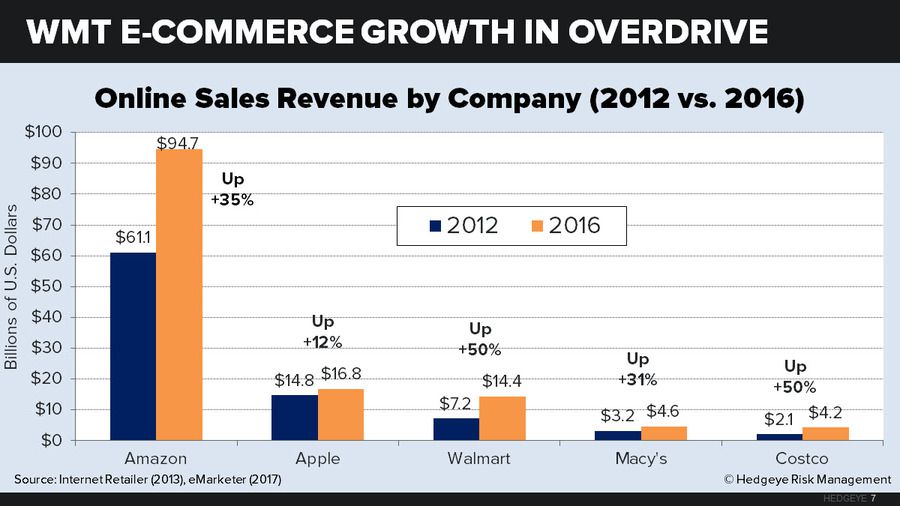

Walmart’s e-commerce efforts are already starting to pay off: The company’s online sales shot up 63% YOY in Q1 2017, with officials claiming that most of this growth was organic. The firm now sells 50 million first- and third-party items online—up from just 34 million a year ago. Yes, Amazon’s online sales in the United States still outpace those of Walmart by about 6:1, but even that is an achievement considering that Walmart is new to the game.

By contrast, it would be a lot tougher for Amazon to become Walmart, a company that has 5,000 stores and 1.5 million employees in the United States alone. Amazon’s physical presence to date includes less than 500 unintegrated Whole Foods stores plus a handful of its own brick-and-mortar bookstores. In other words, if the future is to be a blend of physical and online, Amazon is way behind.

The political crosshairs are shifting toward Amazon. We’ve already established that Amazon must grow much bigger to be able to generate Walmart-scale profits. But such growth may encounter political headwinds. Judging by Donald Trump’s tweets, the President already doesn’t like Amazon at its current size.

A decade or two ago, Walmart was widely criticized for underpaying its workers and decimating communities with bargain-bin consumerism. (The Wikipedia page "Criticism of Walmart" has 181 footnotes.) But Walmart has recently moved to silence its detractors by enacting expensive cross-the-board wage hikes (up to a $10/hour minimum last year) and by ushering in an ambitious pro-environment "sustainability platform." Indeed, today the script is flipping: Amazon is becoming the new target for many of those same consumer advocates. They say that its e-commerce dominance—powered by robot-filled warehouses—is not just underpaying workers. It's actually killing retail jobs. Meanwhile, progressive Democrats steamed about corporations not paying their taxes can't help but target Amazon: From 2007 to 2015, according to The Washington Post, Amazon's total tax rate covering federal, state, local, and foreign taxes was 13.0% versus Walmart's 32.1%. Here's one issue where Bernie and the Donald think pretty much like bros.

In an era when consumers pride themselves on buying local to support their community (see: “The New Localism”), Amazon represents a faceless global entity without roots, a “citizen of nowhere.” Walmart, by contrast, is a community institution whose employees may well know your family and go to your church. Come the next natural disaster, which company is most likely to be passing out free water and batteries in your neighborhood?

Even Millennials—a left-leaning, dream-big generation that for all intents and purposes should be overwhelmingly pro-Amazon—show strong support for Walmart. According to YouGov BrandIndex, Walmart ranks as the fifth-favorite brand among Millennial consumers—just one spot behind Amazon and ahead of brands such as Netflix (#6) and Apple (#8). Why? Community-oriented Millennials likely appreciate the value of a company that employs 1.5 million workers—and are won over by its ultra-low prices.

The next recession will favor Walmart. What about the looming possibility of a recession or bear market sometime over the next couple of years? Clearly, a downturn would favor Walmart over Amazon. Walmart specializes in consumer staples, a category that is virtually recession-proof (people have to eat, after all). And few Walmart shoppers are directly impacted by the S&P 500. While Amazon has been trying to beef up its menu of everyday household items, the company still deals mostly in the sale of upscale discretionary, which lives or dies with the consumer confidence index. Walmart is the very definition of a low-beta stock—just as Amazon is the very definition of a high-beta stock.

THE FUTURE

What does all this mean for consumers?

In the years ahead, the emergence of this dueling duopoly will likely benefit consumers who are already saving big on deals and discounts. For instance, in February, shoppers had to buy $49 worth of Amazon goods to qualify for free shipping. Today, that same perk costs just $25. All the bells and whistles that Amazon continues to add to its Prime service in order to encourage signups carry a massive marginal benefit for consumers who, just a decade ago, were paying $79 a year nominally for free shipping alone. Likewise, Walmart.com shoppers can now save up to 5% on more than 1 million items through in-store pickup.

As this competition heats up, it could have a deflationary impact on prices. Just look at Big Soda. Coca-Cola and PepsiCo have long been a duopoly, together controlling roughly three-quarters of soda sales. This cutthroat competition has helped to keep prices lower: The CPI for carbonated beverages has risen less than half as quickly as the CPI for all food since the early 1980s.

And what about investors?

On balance, in our opinion, the long-term economic prospects of these two firms are about evenly matched. Amazon has the obvious edge in tech know-how, visionary leadership, business diversification, and near-term growth momentum. Walmart has the edge in size, scale, community building, and actual profitability. We’ll even concede that Amazon may have the overall edge.

But the fact that the two companies are in the same discussion means that Walmart is the vastly better long-short play. Reason? Valuation. Amazon is arguably the most overvalued member of the S&P 100, and Walmart is among the most undervalued.

According to one analyst firm, New Constructs, Amazon’s price, assuming no future growth in economic earnings, should be $82, about 90% lower than its current price ($1,001). Alternatively, Amazon’s current price assumes earnings growth of at least one percent faster than the economy average for the next 100 years. And Walmart? Assuming no future growth in economic earnings, it should be $113, about 50% higher than its current price ($76). In other words, Walmart is a buy even with zero nominal earnings growth.

The takeaway: Walmart and Amazon may both well outperform the broader retail market in the years to come. But don’t be too surprised if Walmart eventually emerges on top. And even if the homely Bentonville retailer does no more than stick around, that makes it a big long-short winner relative to its bleeding-edge Seattle-based rival.