Today, the second revision to 3Q09 Gross Domestic Product was released and showed a downwardly-revised annualized real growth rate of 2.2%, reduced from the second estimate of 2.8% and the initial estimate of 3.5%. This followed a 0.7% decline in reported 2Q09 GDP. The vast bulk of the growth comes with a significant cost to tax payers and remains dependent on short-lived stimulus programs, like housing.

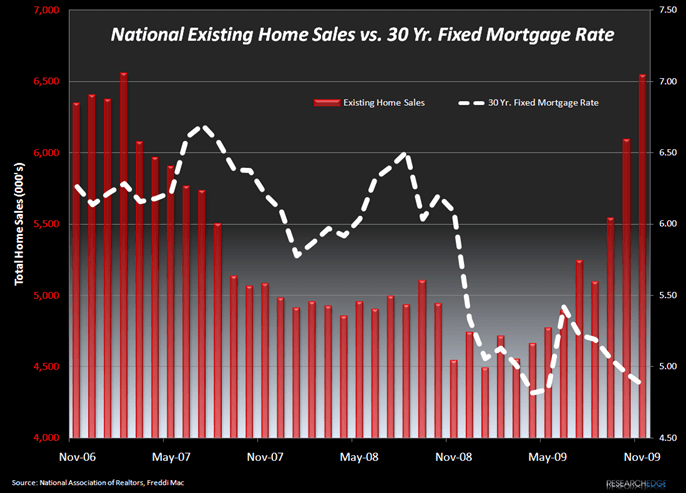

Consumers, like the “piggy bankers,” are benefitting from the free money policies of the FED and the government stimulus programs. The NAR reported today that sales of existing U.S. homes rose to the highest level since February 2007. Existing home purchases increased 7.4% to a 6.54 million annual rate from a revised 6.09 million pace the prior month. The median sales price declined 4.3%. A sustained recovery in housing and the economy depends on low interest rates and a resumption of job growth.

As you can see from the chart below, lower mortgage rates have helped sales of existing homes! But that could change!

Right now, yields on mortgage securities have climbed from 3.9% on November 30th to 4.5% today, the highest level in four months. The implications are that the market is responding to the acceleration in housing despite the fact that rates are rising. It’s possible that higher rates will slow the housing numbers down.

We continue to argue that the FED is behind the curve and that interest rates are likely headed higher in Q1. At the very least, the FED will be altering it official “verbiage” that will signal rates are headed higher.

Looking ahead, the "advance" estimate of 4Q09 GDP growth is scheduled for release on January 29th. Consensus estimates are for continued, positive quarter-to-quarter real growth of 3%. For 2010 the consensus has GDP growth of 2.6%. How the 4Q09 estimates hold up will depend on initial reporting of December employment, retail sales, industrial production and housing data due to be released in January.

While some parts of the economy are showing some bottom-bouncing, if you eliminate the non-recurring, short-lived spikes from temporary stimulus measures, there is little or no GDP growth. The upturn in real GDP growth reflected the following three factors; all are a result of temporary stimulus measures:

- Spending for new cars and trucks was particularly strong, reflecting the federal “cash for clunkers” program that was in effect during July and August.

- Export and inventory investment also contributed to the upturn. The three week dollar rally will slow this factor down.

- Residential housing rebounded due to the home buyer tax credit. The current program expires April 30, 2010.

Despite all of this good news, the Rasmussen daily Presidential Tracking Poll is reporting that the Obama Presidential Approval Index stands at -21, the lowest approval Index rating for Obama since he has become president.

The market is making a new high today on the strength of the economy and more people disapprove of the way Obama is handling things. What is wrong with this picture!

Howard W. Penney

Managing Director