FINL: A Beat Will Need to Come from Costs

Our analysis suggests that in order for FINL to beat numbers like so many others have in recent weeks, it’s going to have to come from somewhere other than the top line.

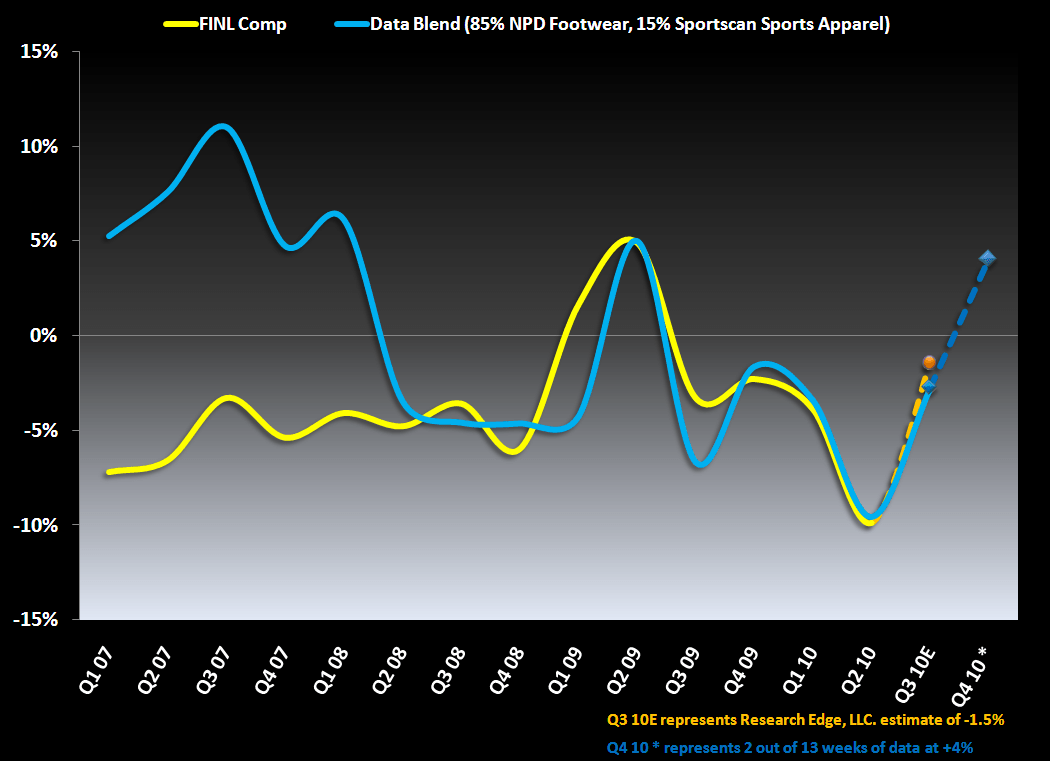

Lining up footwear and apparel POS data with FINL comps suggests that there is little upside to be gained on the top line for the quarter about to be reported. This analysis has served us well, as FINL comp trends have an 85% correlation with a blended combination of NPD footwear data (85% of the blended data) and Sportscan sports apparel figures (15% of the blend) over the last year and a half. Tracking the comp trends to the data blend, implied Q3 10 comps range between -1% and -3%, which compares to the consensus at -0.8%.

On a positive note, the first two weeks of the quarter have definitely stepped up, and appear to be trending +mid-single. But keep in mind that FINL noted on the Q2 call that comps were up 7% in September, which clearly did not hold.

One of the most notable points is that FINL’s sales/inventory spread trajectory is sitting in positive territory for the 6th quarter in a row. Inventories are lean…very lean. In order to prevent erosion, FINL really needs to see an acceleration in sales in conjunction with more commitment to actually beefing up inventory.

We’re modeling a 5.6% sales decline, a -4% EBIT margin, and a loss of $0.11 per share. Could FINL print the Street’s -$0.09? Yes, and they could even beat it. But it will need to come from SG&A – and the cuts there are finite.

We’re not uber-bears on FINL by any means… In fact, this is a space we like a lot headed into 2010. But before ’10, we need to get past this quarter.

Note: FINL reports earnings after the close on 12/22 with the call on 12/23 before the open