The guest commentary below was written by Dr. Daniel Thornton of D.L. Thornton Economics.

In several previous essays, here, here, and here, I pointed out that the Fed’s enormous balance sheet has had the unintended consequence of producing an enormous increase in the money supply. Specifically, the M1 money measure (currency plus checking deposits) has increased by over $2 trillion since August 2008.

This is an enormous increase by any standard.

Moreover, the money supply will continue to grow rapidly as long as the Fed’s balance sheet remains large. I’m amazed that current and previous members of the Federal Open Market Committee (FOMC) don’t understand the money supply process that is taught in an undergraduate Principles of Economics course. They cling to the misguided belief that the Fed can control the money supply because it pays banks an interest rate (the IOER) to hold excess reserves.

Indeed, former Fed Chairman, Ben Bernanke, recommends that the Fed maintain its large balance sheet indefinitely (here). It would be ok if they acknowledged that the large balance sheet was causing an explosion in money growth, but they were not concerned because inflation remained subdued. But they don’t seem to understand that this is happening. Read this essay and you’ll be smarter than the FOMC.

Figure 1 shows total reserves held by banks and excess reserves, i.e., the reserves that banks hold in excess of what the Fed requires each bank hold to meet its statutory reserve requirement. The reserve requirement is based on the amount of each bank’s checkable deposit liabilities. Total reserves and excess reserves increased by nearly the identical amount when the Fed began increasing reserves following Lehman Bros.’ announcement.

Because all of the reserves the Fed supplied were initially excess reserves, banks began to finance their lending from the reserves supplied by the Fed. Consequently, required reserves (the gap between total reserves and excess reserves) became progressively larger. Required reserves (shown in Figure 1 as the gray line with the scale on the right-hand axis) increased from $44 billion in August 2008 to $173 billion in February 2017.

“Is this a large increase?” No. It’s enormous.

Required reserves moved up and down during theperiod from January 1975 to August 2008 due to changes the Fed made to reserve requirements and other factors but averaged $45.4 billion, slightly more than they were in August 2008.

“What caused the large increase in required reserves?”

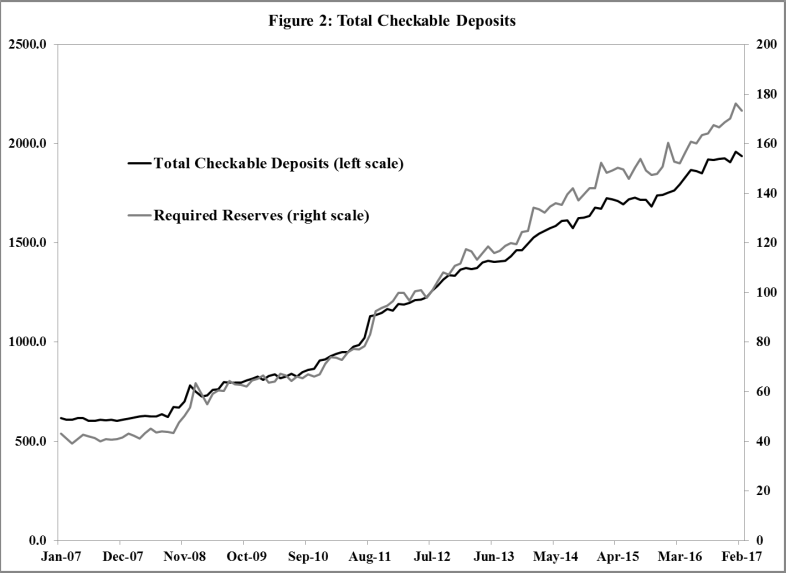

Required reserves are based on a percent of checkabledeposits held by banks. Consequently, required reserves increased because banks’ checkable deposits increased. This is shown in Figure 2, which shows total checkable deposits of banks and banks’ holdings of required reserves. The figure shows that the $129 billion increase in required reserves was accompanied by a $1.3 trillion increase in total checkable deposits. Hence, the average ratio was 10 to 1.1

“Is this a large increase?” No, once again, it’s enormous.

Total checkable deposits increased from $110 billion in January 1959 to $624 billion in August 2008. Since August 2008 checkable deposits have increased by 2.5 times more than it did during its previous history.

“Why did checkable deposits increase so much?"

They increased because when banks make loans they create checkable deposits. “But this must happen all the time.” Yes, but checkable deposits increase only when the Fed increases the supply of reserves. When the Fed doesn’t increase the supply of reserves, banks finance their lending from funds borrowed from the public. For large banks, this is done mostly by selling large negotiable certificates of deposit. Prior to Lehman’s announcement, only a tiny fraction of banks’ lending was financed by reserves supplied by the Fed. Because the funds for lending were borrowed from the public, there was no massive increase in checkable deposits and money.

The Fed’s massive purchase of securities changed that. Banks had so many reserves that they no longer needed to borrow from the public to make loans. Indeed, since September 2008 banks have made essentially all of their loans from reserves and will continue to do so as long as excess reserves remain abundant.

“But I’ve heard economists say that banks are holding excess reserves because of IOER, which is now 1 percent.”

This is true but misses the point. Because bank reserves, like Treasuries, have no default risk, Bernanke, and many other economists, and some on the FOMC argue that banks are indifferent between holding excess reserves and holding Treasuries. But this is not quite correct.

“What is correct?”

The correct marginal condition, as economists refer to it, is banks will be indifferent between holding excess reserves and any loan or investment that has a risk-adjusted rate of return equal to the IOER. Hence, banks will make any loan or make any investment with an expected risk-adjusted interest rate higher than the IOER. The prime loan rate is currently 4%—3 percentage points above the IOER. Other loan rates are much higher. Loan default rates are typically low. Hence, it is hardly surprising that banks funded their lending out of excess reserves that only yield the IOER.

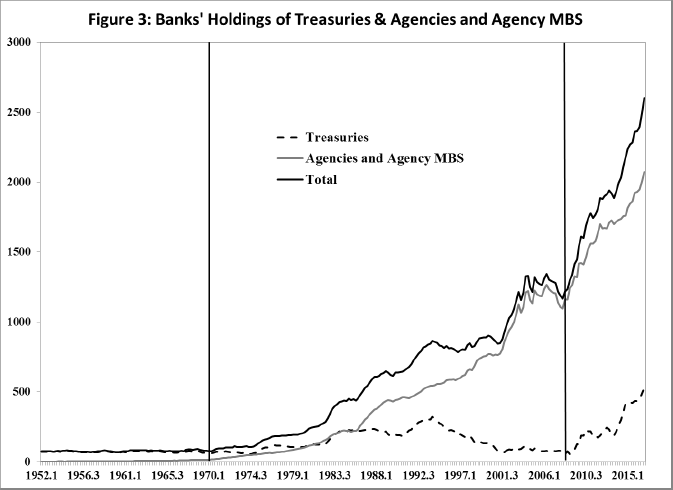

Banks have significantly increased investments for the same reason—the risk-adjusted interest rate on investments is significantly higher than the IOER. Figure 3 shows banks holdings of Treasuries and agenciesand agency-backed mortgage-backed securities (MBS), quarterly from 1952.1 to 2016.

The first vertical lined notes 1970 when the Freddie Mac began. Freddie Mac is a government-sponsored agency (GSE) that assumes the default risk of mortgages by purchasing mortgages and bundling them into mortgage-back securities that it resells. The GSE assumes the default risk. Note the marked increase in banks’ holdings of agency and agency MBS beginning in 1970. Banks holdings of agency-backed MBS increased dramatically because they were free of default risk.

The second vertical line denotes 2008. The massive increase in reserves supplied by the Fed caused banks to accelerate their purchase of agency debt and GSE-guaranteed MBS, increasing their holdings by $900 billion. Banks also increased their holdings of government securities by about $500 billion or a total of $1.4 trillion.

Banks will continue to increase their holdings of such securities as long as the risk-adjusted rate on suchinvestments is higher than the IOER. As is the case with making loans, purchasing securities with reserves also increases total checkable deposits and, hence, the money supply.

“Why haven’t banks made enough loans and purchased enough securities to reduce their holdings of excessreserves to essentially zero?”

The reason is there are not enough loans or investments that have expected risk adjusted rates of return higher than the IOER in order to convert all of the excess reserves into required reserves. Excess reserves are currently about $2.2 trillion. At a ratio of 10 to 1, banks would have to make about $22 trillion of new loans or investments in order to convert all of the excess reserves into required reserves.

There simply are not enough assets with risk-adjusted returns higher than 1% to do that. After all, the entire U.S. debt is $20 trillion; half of which is foreign-owned or held by the Fed. Consequently, banks are holding massive amounts of excess reserves because:

- The Fed has forced banks to hold them by keeping its balance sheet large, and

- There are simply not enough safe investments that yield interest rates higher than the IOER.

Nevertheless, banks will continue to make all of the loans and investments that have returns higher than the IOER and the money supply will continue to increase accordingly. The gap between total and excess reserves, shown in Figure 1, will continue to widen.

Checkable deposits and M1 will continue to increase rapidly. Indeed, they will continue to grow until the balance sheet is shrunk to a level where excess reserves are tiny (they were between $1.5 and $2 billion before the Fed expanded its balance sheet) and, therefore, no longer asource of funds for bank lending.

Furthermore, as I point out here, increasing the IOER will not halt the expansion of the money supply because interest rates on loans and investments tend to increase lock-step withthe IOER. The only way the Fed can prevent the money supply from expanding is by reducing the balance sheet to the level where excess reserves are trivial or by increasing reserve requirements to 100%.

The latter requires amending the Federal Reserve Act. The Federal Reserve Act sets a limit of 12% on reserve requirements. The massive increase of M1 has yet to produce a corresponding noticeable increase in inflation or other problems. But we are in unchartered waters. Real money balances—the purchasing power of money—have increased from$643 billion in August 2008 to $1.4 trillion in April 2017.

There is no way to predict whether the continuous increase in the money supply will be benign or cause great havoc. That the FOMC is unaware of the massive increase in M1 and that the money supply will continue to expand rapidly as long as the banks are holding high levels of excess reserves is frightening. We can only hope that the FOMC doesn’t get blindsided again.

EDITOR'S NOTE

This is a Hedgeye Guest Contributor piece written by Dr. Daniel Thornton. During his 33-year career at the St. Louis Fed, Thornton served as vice president and economic advisor. He currently runs D.L. Thornton Economics, an economic research consultancy. This piece does not necessarily reflect the opinion of Hedgeye.