Across the board the market finished higher on Monday; the S&P 500 closed up 0.7% on the day. The tone was set early with an energy M&A deal where XOM is buying XTO. Also, news that Abu Dhabi will provide $10B to Dubai provided an easing to sovereign debt contagion concerns. While the S&P 500 closed at a higher-high, the financials are still broken on both TRADE and TREND, while Energy is broken on TRADE.

For the balance of the week the MACRO calendar will dominate the news cycle. We are looking forward to several key data points in the next two days, including inflation numbers (PPI on Tues, CPI on Wed), Housing Starts on Wed and the results from the FOMC meeting on Wednesday.

Looking at the Producer Price Index (PPI), the most recent reports have been generally to the upside of expectations. Currently, Bloomberg has a 0.8% MoM number versus 0.3% the month before.

On Wednesday, Consumer Price Index (CPI) for November 2009 will be reported. The consensus estimates for the seasonally-adjusted November CPI is 0.4% according to Bloomberg versus 0.3% in October. Given the implied relative strength of gasoline and food prices in the November retail sales data, an upside surprise to consensus is a better than average possibility.

This is what matters most. A consensus report would boost year-to-year CPI inflation from minus 0.2% in October to roughly a positive 1.9% in November. The November CPI data will officially end the recent period of formal DEFLATION.

The RECOVERY trade was in full force yesterday as the Materials (XLB), Industrials (XLI) and Energy (XLE) were the three top performing sectors. The bottoms three were Financials (XLF), Utilities (XLU) and Consumer Staples (XLP). It’s noted that every sector was up on the day and six sectors outperformed the S&P 500.

Yesterday, the natural gas sector benefited from XOM’s acquisition of XTO. Naturally the transaction increased speculation concerning further M&A activity in natural gas. Materials (XLB) was the best performing sector, with Metals and Mining stocks leading the way.

The Financials (XLF) continue to underperform, after being among the worst performers last week, but managed to end the day with a small gain. C and MBIA were the two worst performing stocks in the XLF.

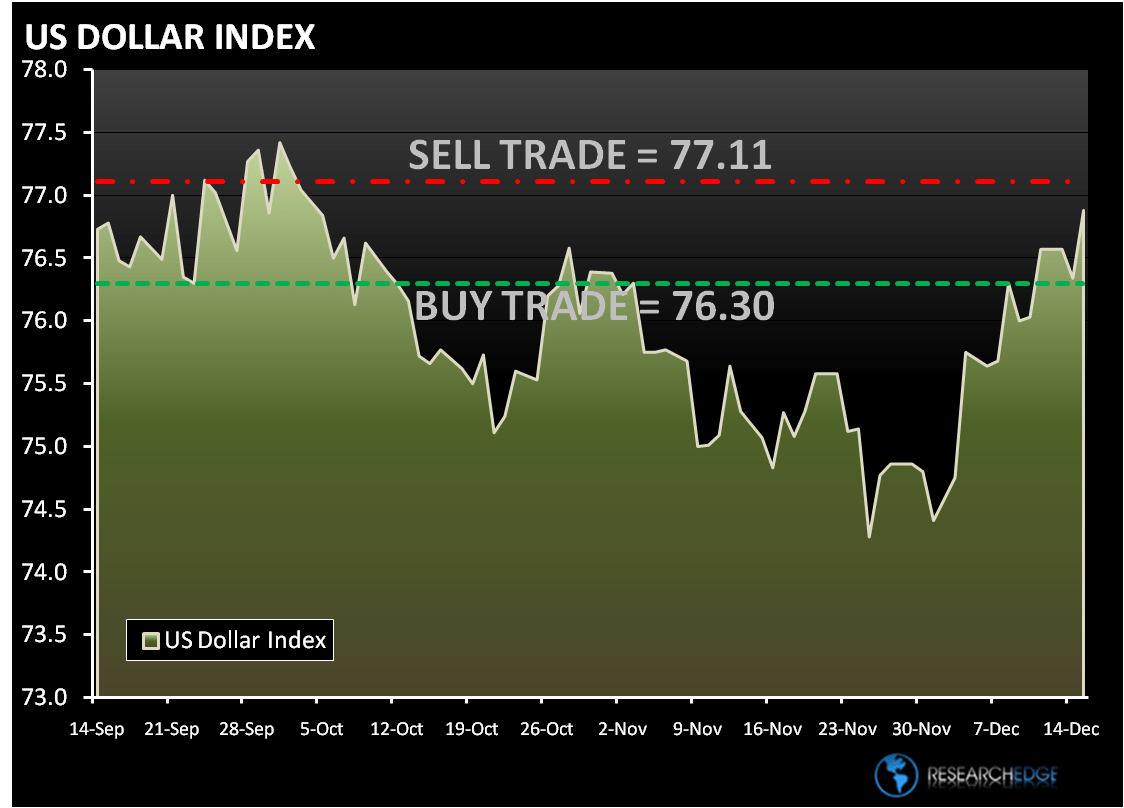

From a risk management standpoint, the ranges for the S&P 500, the Dollar Index and the VIX are seen in the charts below. The range for the S&P 500 is 17 points or 0.5% upside and 1.5% downside. At the time of writing the major market futures are trading slightly lower.

In early trading today, crude oil is trading lower as the dollar is moving higher. The Research Edge Quant models have the following levels for OIL – buy Trade (68.78) and Sell Trade (74.30).

In London Gold is trading lower by 0.7% to $1,118. The Research Edge Quant models have the following levels for GOLD – buy Trade ($1,089) and Sell Trade ($1,148).

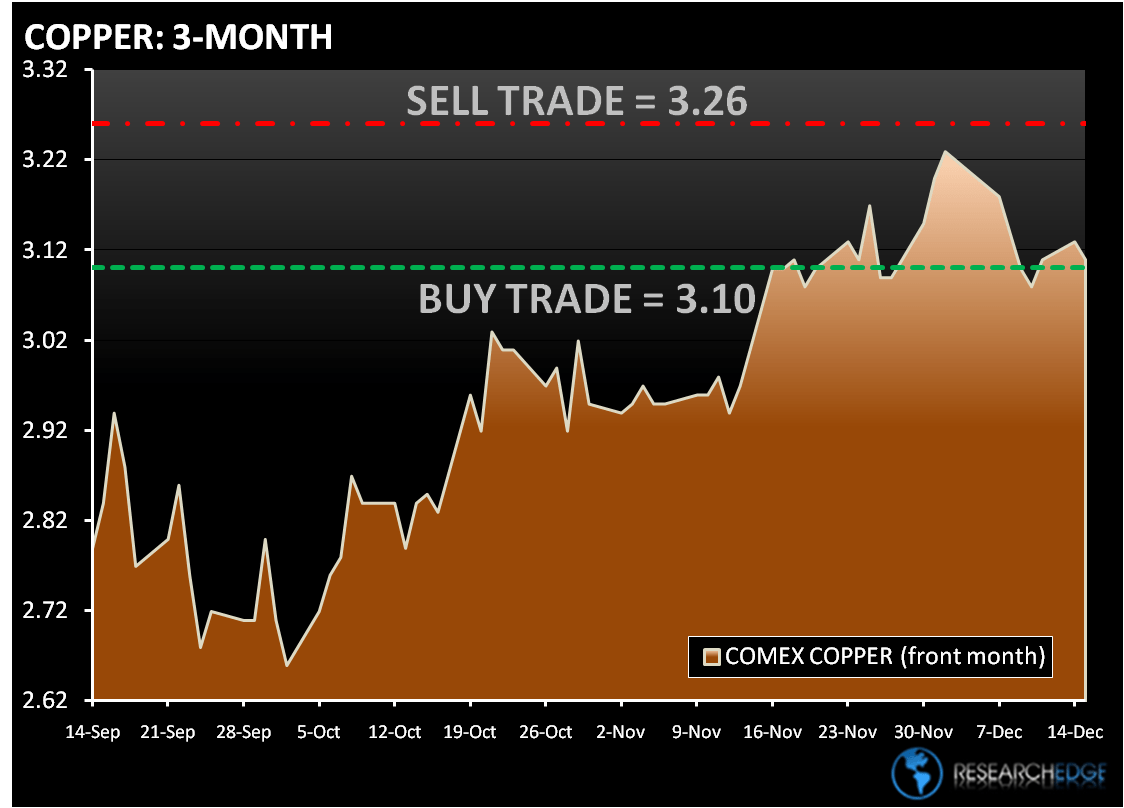

Copper in London is lower as the dollar strengthened. The Research Edge Quant models have the following levels for COPPER – buy Trade (3.10) and Sell Trade (3.26).

In early trading today the US Dollar is up trading at +0.7% amid speculation improving economic data in the U.S. will require the Federal Reserve to signal an exit from easing policies intended to combat the recession.

Inflation is back!

Howard Penney

Managing Director