Adibok Getting Toned?

Reebok is Looking Hot in the Toning Category. Does it Matter?

Adibok is shipping every pair it can get its hands on to take advantage of this trend – which will make ‘Easy Tones’ tough to comp against next year. If the company sees any acceleration in backlog or sales in the US near-term, we’ll question the sustainability big time.

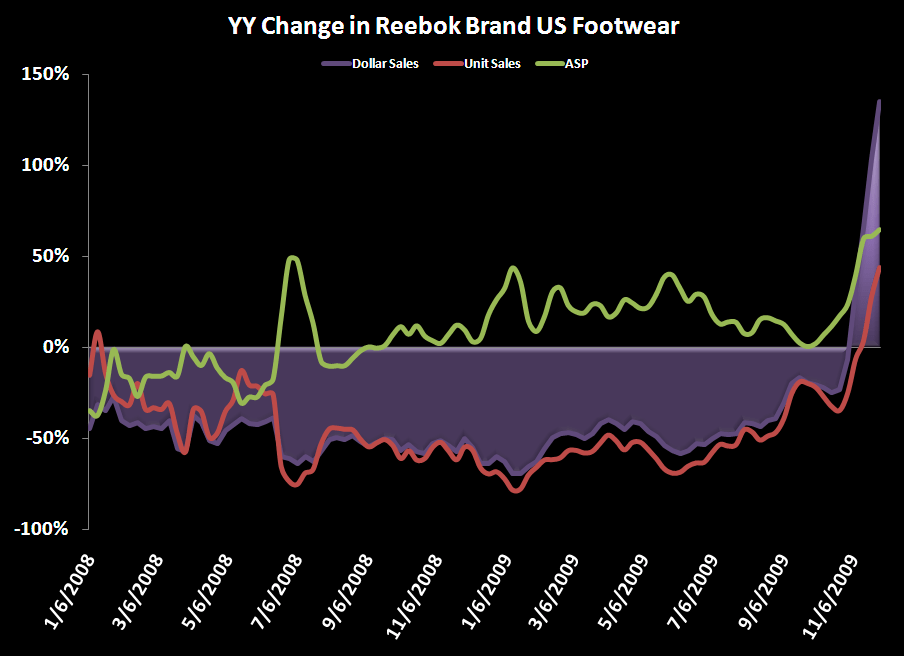

Reebok is staking its claim on the growth we’re seeing in the toning footwear category (MBTs, Shape-Ups by Skechers, Avon’ s Curves, etc…) with its Easy Tones product. How meaningful, you might ask? After comping down 50% for the better part of 2 years, recent weeks have spiked to +125%. No kidding. As much as we continue to believe that Adibok is a sinking ship, we won’t ignore the facts. Could the recent performance help right buouy the boat? After going the math, the answer is ‘probably not’.

Here’s the math: 1) Reebok is 20% of total Adidas Group, 2) 45% of Reebok is footwear, 3) 45% of Reebok revenues are in the US (the focus of the toning trend), and Easy Tones are 35% YTD of NPD’s Reebok footwear (60% over that last 6 weeks). The math says that the Easy Tones could be between 6-9% of Reebok, and 1%-2% of total Adidas group. Reebok is getting a boost on both the top and bottom line as these toning shoes, like Skechers Shape Ups, sell north of the $100 mark which is driving total ASPs through the roof (ie 50%+).

The bottom line here is that this is a positive near term. There’s no doubt about that. But Adibok is shipping every pair it can get its hands on to take advantage of this trend – before either a) it goes away, or b) it gets so crowded that prices come down and margins take a hit. Either way, the ‘Easy Tones’ will be tough to comp against next year. If the company sees any acceleration in backlog or sales in the US near-term, question the sustainability.

Zach Brown

Analyst