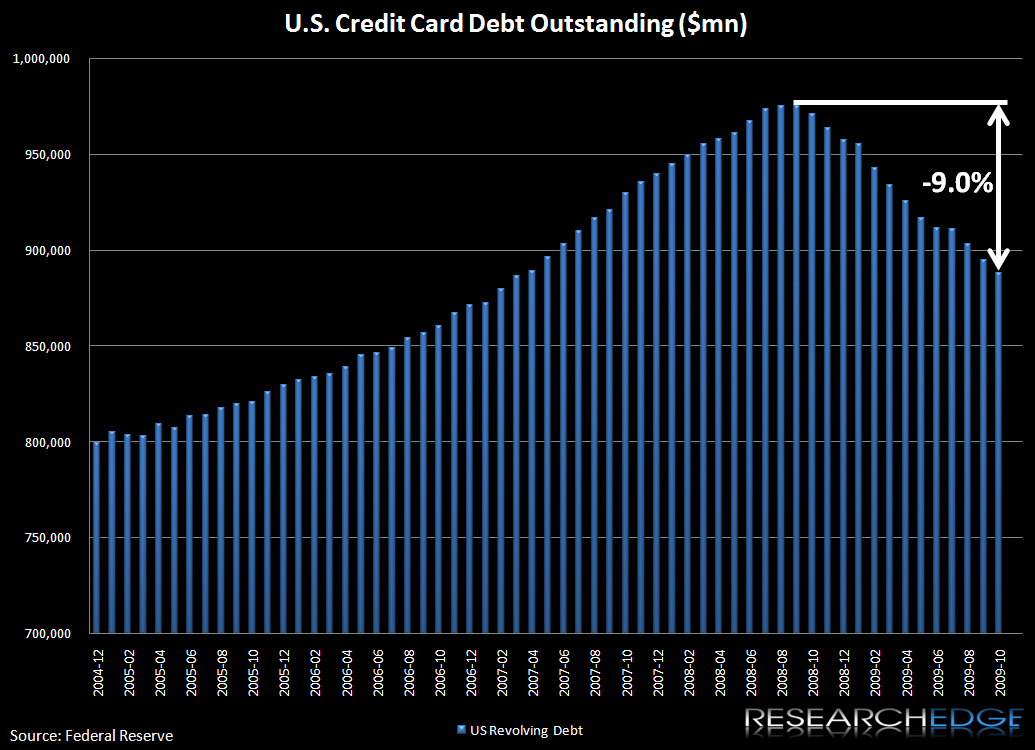

Last night’s release of the government G-19 data shows a consumer continuing to delever at an orderly, but unrelenting pace. Aggregate card debt outstanding declined $8 billion in October to $888 billion, making this the 13th consecutive month in which credit has shrank. Peak to trough decline is now up to 9% ($87 Billion).

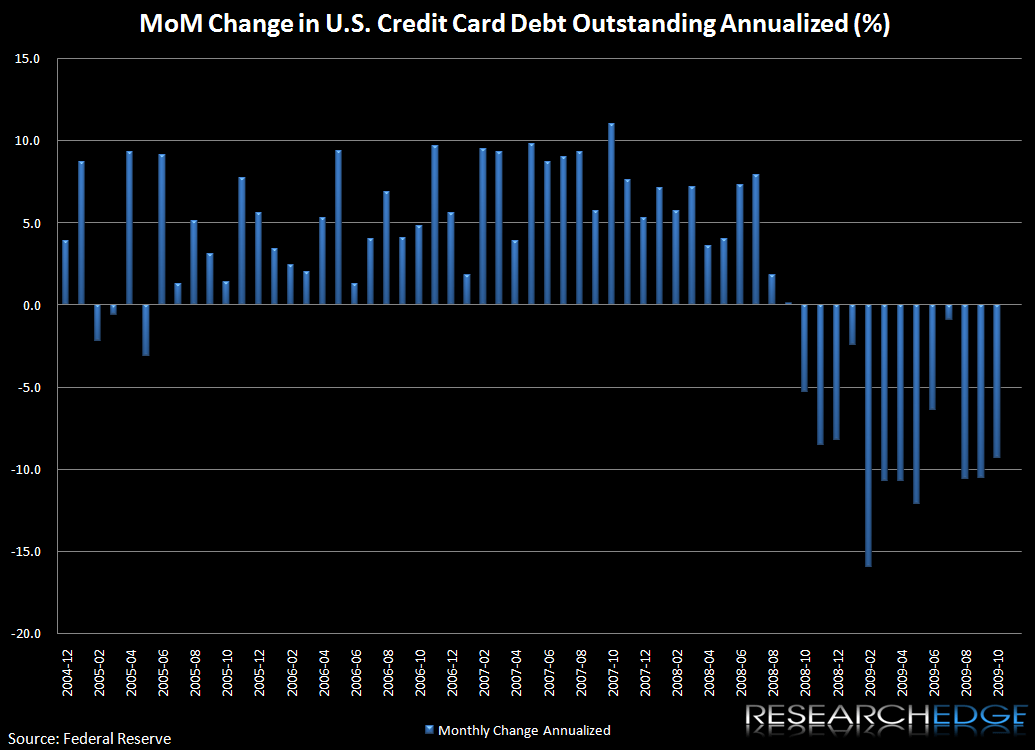

The crunch continues to have two drivers: consumers pulling back voluntarily and banks stripping credit away from the bottom third of the borrower profile (FICO <660). The rate of decline in October was 9.3%, right in line with the monthly average over the last several months. Some might take comfort in the fact that the rate was down modestly from September (10.5%) and August (10.6%), but we think it's too early to call any sort of emerging inflection in this trend.

The G-19 data is a lagging indicator, as October-end data is just becoming available some five weeks after the fact. It's important, however, as it confirms trends unequivocally. If we see this number flatten out and reverse course we'll know that consumers (and banks for that matter) are returning to business as usual. If the trend continues, we'll know the "new normal" is becoming more and more real.

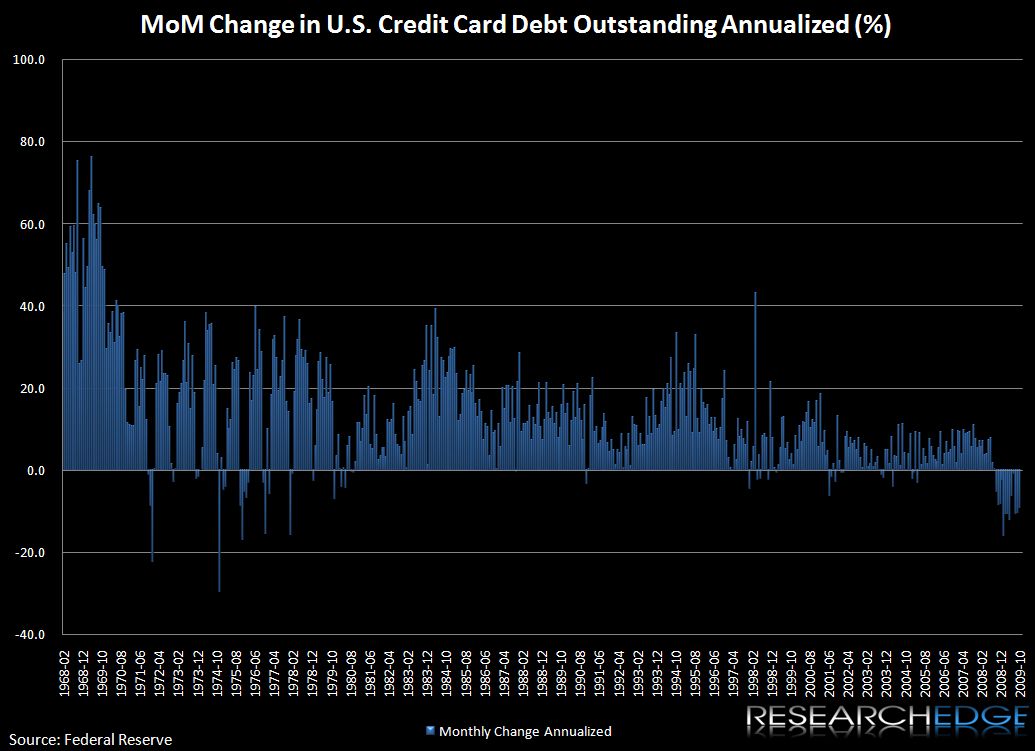

The next chart shows the monthly rate of change (annualized) going back about 40 years. The takeaway is that there's never been a period of credit contraction this sustained. We are in new territory here.

Finally, you might wonder how the individual companies are faring amidst this downturn. The answer: not much better. Take a look at Capital One's managed consumer loan growth - it practically mirrors that of the industry, and in fact, of late, has been accelerating to the downside.