MARKET WATCH: What’s Happening? The sporting goods industry is a “tale of two cities.” One, the city of sports retail stores, is going through the worst of times. Bankruptcies abound, and the retailers that remain solvent face sliding earnings and waning investor confidence. The other, the city of sports and apparel brands, is doing much better. More consumers than ever before are getting their goods online or through brands’ own brick-and-mortar channels.

Our Take: The industry is at a crossroads, and retailers must make their stores a true destination for shoppers in order to compete. For now, the brands look to be the ultimate winners—and those that appeal to the new Millennial mindset stand to gain the most.

In a recent earnings call, Dick’s Sporting Goods (DKS) executives announced that the company is slashing the number of vendors that it works with by 20%, choosing instead to devote more shelf space to in-house brands.

The move is the latest sign of trouble among sports retail distributors, which comprise significantly more than half of all jobs in the sporting goods industry—but significantly less than half of all earnings. Dick’s is the largest of the retail crowd, earning $7.7 billion in revenue last year. Other competitors include product-specific retailers like Foot Locker (FL: $7.6 billion) and Finish Line (FINL: $1.9 billion)—both of which specialize in footwear—as well as regional players like Big 5 Sporting Goods (BGFV: $1.0 billion) and Hibbett Sports (HIBB: $972 million).

The sporting goods industry also includes sports and apparel manufacturers (which we’ll refer to here as “brands”). The two largest are Nike (NKE) and Adidas (OTC: ADDYY). Nike leads the way, having earned $33.5 billion in revenue last year. Adidas ($20.3 billion) is a global brand that does 83% of its business outside of North America. Under Armour (UAA: $4.8 billion) traces its origins to elite team sportswear; founder Kevin Plank’s first deals came selling products to collegiate and National Football League teams. Finally, Lululemon (LULU: $2.3 billion) specializes in apparel as one of the nation’s premier “athleisure” brands.

The industry as a whole is coming off of its worst year since the Great Recession. According to the Sports & Fitness Industry Association, total U.S. revenue for sporting goods, equipment, and apparel tallied $87.7 billion in 2016, growing just 1.9% YOY over 2015—in other words, almost zero growth after inflation. As recently as 2011, YOY growth was above 4%.

RETAILERS: VASTLY UNDERPERFORMING

Most of the industry’s overall loss of momentum can be traced back to a cratering retail landscape. In late 2015, Boston-based City Sports filed for bankruptcy, while Sports Authority followed suit in mid-2016. Other recent bankruptcies include MC Sports, Sport Chalet, and Eastern Outfitter.

What’s behind this wave of bankruptcies? Clearly, the traditional economies of scale long enjoyed by brick-and-mortar sports retailers have run out.

For one, the rise of e-commerce has marginalized firms that once used their product expertise to move merchandise. Not only is buying online easier than trekking out to the store, but thanks to online reviews, other buyers now serve as subject-matter experts who can steer you toward a pair of cleats just as effectively as an in-store expert could.

This issue is hardly unique to sporting goods retailers. Whether it’s department stores or big-box stores, firms of all types must come up with a compelling reason for shoppers to head to the store rather than shop from their living rooms. As our own Brian McGough pointed out in a recent call, the brick-and-mortar retail space as a whole is facing the prospect of a huge shakeout in the coming years as more and more capacity moves online.

What compounds the bad news for sports retailers, however, is the fact that the very brands that sports retailers depend on are increasingly becoming direct competitors. How? Direct-to-consumer (DTC) sales, by which brands sell directly to buyers through their own brick-and-mortar outlets or online channels. Nike has been particularly active in ramping up its DTC business, with CEO Mark Parker recently revealing that sales of this type surged 23% YOY during Q2 2016. Under Armour, meanwhile, earned 40 percent of its Q4 2016 revenue from its DTC segment.

Adidas Managing Director Greg Thomsen commiserates with sports retailers, acknowledging that, “It’s hard for sporting goods stores when their number one brand also becomes their number one competitor.”

Hardest hit have been middle-market, all-in-one vendors à la Sports Authority. These firms are beat on price by e-commerce, and are beat on quality by specialty stores. As 23-year-old consumer Sarah Hermina says, “Sports Authority always had older styles, and its prices are more or less the same as a Nike outlet, so I’m more likely to shop where I have more options from the brand.” Firms like Hibbett, Big 5, and Dick’s are most exposed to these risks going forward—though the latter’s effort to focus on exclusive private-label brands that shoppers can’t get elsewhere helps its cause.

It’s clear that the brick-and-mortar business model that sports retailers rely on is in serious trouble. With DTC and e-commerce sales comprising more than the sector’s total growth, these firms are forced to undercut each other to stay afloat. However, slashing profit margins is a problem when you’ve got overhead in the form of millions of square feet of store space. It’s easy to see why virtually all sports retailers have seen their stock lose value since 2014.

BRANDS: FARING MUCH BETTER

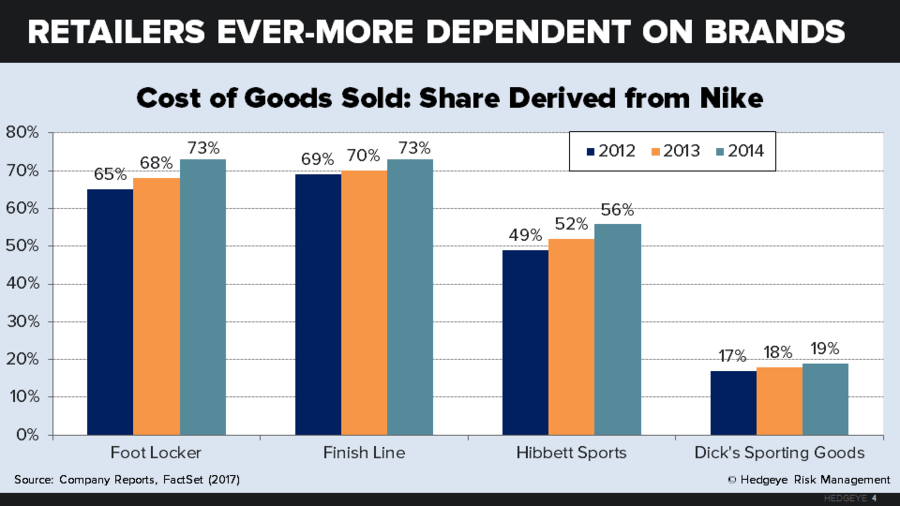

With each passing year, profitability is moving away from the distributors—and toward the brands themselves. Just look at Nike, which is far and away the biggest growth driver for many retailers. More than three-quarters of Foot Locker and Finish Line revenue came from Nike in 2014.

Nike is not the only brand faring well. Adidas has been perhaps the biggest success story lately: Its stock has doubled in value over the past year alone, and it has recently reclaimed its place as the second best-selling brand in the United States. Lululemon has rebounded from a rough 2014 brought on by its yoga pants scandal and subsequent PR debacle. The outlier has been Under Armour, whose stock has plummeted 80% since late 2015.

So what separates the best-performing brands from the pack?

Pricing power. Some brands are more profitable than others. In Q4 2016, Lululemon’s LTM net margins came in at 12.6%, just ahead of Nike (11.6%). Margins were far lower for Adidas (5.3%), and were lowest for Under Armour (4.1%).

Two factors enable Lululemon and Nike to continually post high net margins. One is cost savings. Lululemon does not use wholesale distributors (thus saving on costs), instead relying on its own channels and select partnerships with fitness studios. Nike, meanwhile, recently added efficiencies to its production process that Deutsche Bank analysts predicted could slash its labor costs by 50% per unit.

Another is market positioning. Lululemon and Nike are luxury brands able to charge a premium for their products. Much like Apple in consumer tech, these aspirational firms know that their target customers want (and can afford) a $298 pair of running leggings or a $720 self-tying running shoe.

Compare these brands to Under Armour. The company first became popular in the late ‘90s thanks to its flagship moisture-wicking compression shirt—but has struggled to adapt in the face of growing competition. Under Armour has attempted to remedy the situation by jumping simultaneously into the high-end space (see its $1,500 trench coat) and the discount space (see its rollout to 1,100 Kohl’s stores)—which only muddles its branding.

A winning generational strategy. In many ways, the dividing line separating winning and losing brands has been drawn by generational turnover. In the ‘80s and ‘90s, Nike rose to prominence among hypercompetitive Xers who embraced rugged all-black ensembles coupled with a no-frills tagline (“Just Do It”). The signing of Xer phenoms like Michael Jordan and Tiger Woods sealed the deal.

But the strategy of selling to Xer athletes who want to push their bodies to the limit has a shelf life. As athletes, Millennials are more concerned with living healthy every day than with winning the race. (See more on the new Millennial attitude toward fitness in “Activewear is in Excellent Shape.”)

Leading brands are taking full advantage of this generational shift. Lululemon offers free fitness classes and social events, building a relationship with Millennials that goes beyond products. Adidas owes much of its success to a recent rebrand emphasizing everyday fitness: In H1 2016, the company’s lifestyle-oriented “originals” segment surged 60% YOY.

Adidas has also emphasized relearning, and retelling, its history: The brand established a history management department back in 2009, and has even published a book documenting the company’s beginnings. This strategy is a surefire way to engage Millennials, who embrace “heritage marketing” as a way to find out the story behind their favorite products. (See: “Out with the New and In with the Old?”)

Nike’s marketing, meanwhile, has also evolved since the original “Just Do It” days. In 2015, Nike released a new ad campaign, titled “Last,” that showed marathon stragglers trudging through a street littered with paper cups. It’s no longer all about winning, the ad seemed to say, but about trying. The company also portrays larger-than-life Millennial sponsored athletes like LeBron James in a highly personal, vulnerable light—a strategy that would have elicited blank stares from Gen-X young adults.

It’s little surprise that Nike is the #3 favorite Millennial brand overall, tops among all sports and apparel brands. Nike subsidiaries such as Converse (#84) and Jordan (#44) also make the top 100.

LOOKING AHEAD

Sporting goods retailers face a tough task—winning back market share from online competitors and their own brands’ DTC operations. Amazon alone maintains a 14.3% market share on sporting goods according to Brian McGough, the fourth-highest share of any category (behind only toys, media/entertainment, and luggage/travel).

The growing draw of e-commerce means that sports retailers must make their stores a destination. As retail reporter Mallory Schlossberg says, “The only way to hook customers into a [sporting goods] store would be to make shopping there an ‘experience.’”

But sports retailers aren’t making any headway here. Though many “outdoor” retailers have taken the “experience” route (see L.L. Bean’s adventure clinics), not many sports retailers have followed. In fact, it’s the brands that are getting this right. Lululemon offers free fitness classes and hosts hobby events like a bouquet arrangement workshop. Adidas recently opened a 45,000-square-foot store on Fifth Avenue, while Nike’s SoHo location boasts everything from soccer to half-court basketball.

And make no mistake: There is an opportunity here. Sporting goods includes many types of products where there is real value added by trying out an item in person. For example, a runner may want to jog around the store to get the feel of a pair of running shoes before buying. A football player may want to try on a pair of receiver gloves and catch a few footballs to determine that the gloves work as advertised. Brands like Nike are already doing this: What better way to try out a pair of soccer cleats than by strapping them on and dribbling a soccer ball on synthetic turf?

One way of making the store a must-visit destination would be to embrace the nascent concept of “made-to-order design,” by which retailers manufacture personalized goods for consumers on premises—a trend highlighted by McGough. But again, it’s Nike that has been working on this, and Amazon that has filed a recent patent indicating that they may follow. If this kind of customized, on-the-spot production takes off, it will be more bad news for retailers who have neither the capital nor the rights to manufacture branded products in their stores.

Unless this situation changes, brands will continue to build up their DTC businesses and take ever-more control of the transaction, while retailers will struggle to remain relevant. The real long-term winners will be brands like Nike and Lululemon that not only sell high-quality products—but that prove they’re interested in helping Millennials live healthy lives. Such brands may just win over this young generation for life.