Nearly every restaurant operator is benefiting from lower food costs, so what is the differentiator to any given stocks’ outperformance – top line sales!

In the second half of 2009 to date, the casual dining stocks as a group have declined 7.6%, excluding Landry’s performance, which is up nearly 150% as a result of CEO Tilman Fertitta’s purchase offer and Pershing Square’s subsequently taking a 9.9% stake in the company. Outside of LNY, the top performers since June 30, 2009 have been (in order of best to worst) CBRL, BWLD, CAKE, PFCB and BJRI. These are also the only names in the casual dining group that have posted positive stock performance thus far in 2H09, which represents a big shift from the first half of the year when only LNY’s stock declined from December 31, 2008 with the group, on average, up nearly 84%.

When I looked at this list of outperformers in 2H09 to date, the first thing that jumped out at me was the fact that three of the names have a high concentration of their restaurant base in California with CAKE at nearly 20%, PFCB at about 16% and BJRI at over 50%. Based on what we have heard about recent trends in California, particularly as it relates to the 12%-plus unemployment rate in the state, it is somewhat surprising that these California-centric names have outperformed.

The more important similarity among the group is, however, that despite some of these companies’ exposure to California, all of these names, except for one, have outperformed the industry benchmark on a comparable sales basis as reported by Malcolm Knapp in the most recent quarters (as shown in the attached charts below). We all know the industry performance is not good, but having less bad results points to share gains and helps to explain, for the most part, the companies’ relative stock performance.

CBRL, which is up nearly 35% since June 30, continues to widen its gap to Knapp, outperforming by more than 6% in it last two reported quarters.

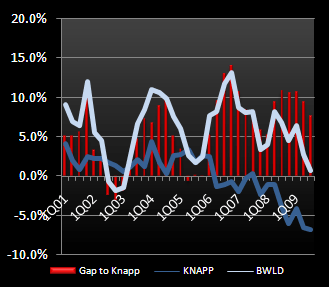

BWLD’s (up 22.8% over the same timeframe) gap to Knapp has come in somewhat in the last couple of quarters but the company still posted same-store sales trends that were 7.6% better than the industry average in 3Q09.

CAKE, up 8.8%, has not outperformed the industry average by the same magnitude as CBRL and BWLD, but the company has performed better than the average in each reported quarter of 2009 (by an increasing amount each quarter) after underperforming the average for all of 2008.

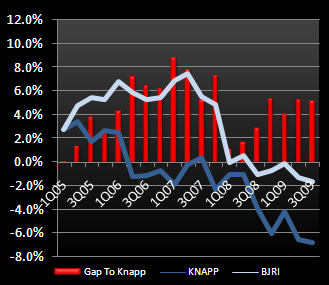

BJRI, up 1.2%, has maintained its 5%-plus gap to Knapp in the last two reported quarters despite the sequential decline in its same-store sales growth trends on both a 1-year and 2-year average basis.

So who does that leave out? PFCB is up 1.7% in 2H09 to date and is the only casual dining name (again outside of LNY) that has posted positive price performance since June 30 with same-store sales trends at its main concept (the Bistro) that are underperforming the industry benchmark. And, that underperformance increased by about 150 bps in 3Q09 on sequential basis from 2Q09. Same-store sales growth in 3Q09 decelerated sequentially from 2Q09 on both a 1-year and 2-year average basis.

Some might point to the improved margin trends at Pei Wei and to the concept’s recent same-store sales outperformance to explain the company’s relative stock performance, but it is important to remember that the Bistro still accounts for about 75% of total company sales. There is no reason to believe that Bistro trends will turnaround prior to the industry so I do not think it is reasonable to believe that PFCB will be able to maintain this stock price outperformance much longer.