Nitpick the TIF quarter all you want. There’s a Brand problem, with not enough capital deployed to fix it. SHORT.

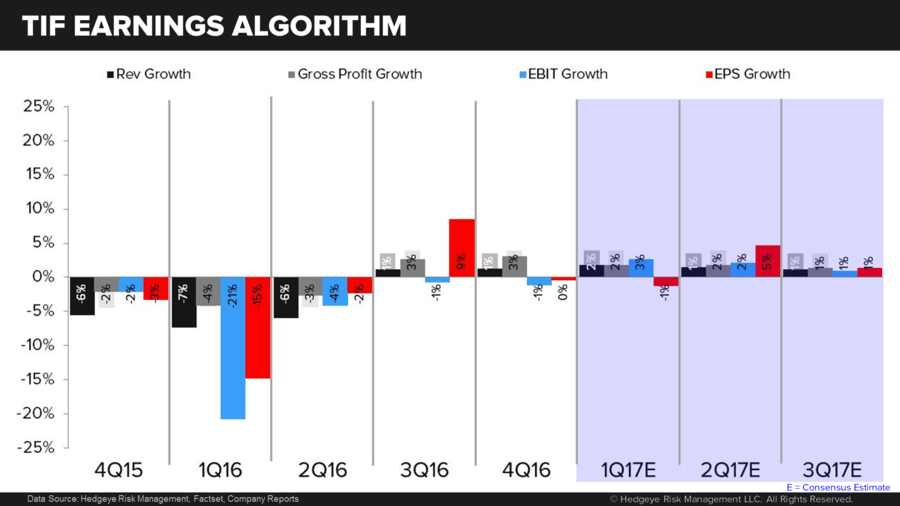

- First off, this TIF print is bad on a stand-alone basis. -2% comp and a 1% EPS decline.

- But I’m not going to look at this glass-half-empty just cuz I’m short it. The reality is that it is better than expectations. And all stock moves (most) are relative to expectations. This one is no different.

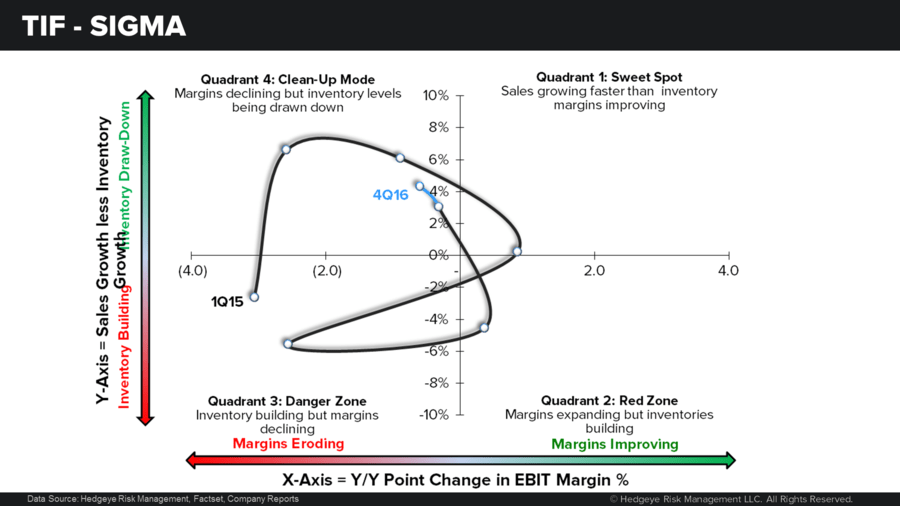

- TIF guided in-line, inventories look good relative to last year (despite 400+ days of diamonds in inventory), and it’s about to face its easiest comp of the year in 1Q.

- The reality, however, is that this company has to comp consistently – and it has not comped in 9 quarters.

- And I’m not talking a 1-2% comp. It needs the msd comps of yesteryear.

- I’m pretty dang certain that TIF has a brand problem. The soonest I’ve seen a brand problem fixed is 2-3 years AFTER the investment (SG&A and capex) needed to fix a brand problem. TIF has not allocated that capital yet.

- I don’t care who’s going activist on this name – albeit with little skin in the game – the company has to take down numbers to set it on a path of consistent growth.

- The 10% capex boost and slight SG&A deleverage for FY18 is nice. But how about a 100% boost to capex ($500mm), and 1,000 bp SG&A deleverage. Don't laugh. That's what's on par with what TIF needs.

- Someone actually asked on the call if Reed Krakoff would affect Fall/Holiday assortment. Of course the company said Yes. But one singular person -- even someone with RK's track record -- cannot meaningfully affect the product mix of a $4bn company a) so soon, and b) without a much bigger design team (ie cost more $$).

- I also don’t care about a ‘reset’ with a sandbag (which we did not get) UNLESS the research call shows me that the capital is being deployed in a way that will fix the brand. I actually think that management is in denial about there even being a brand problem. Activists can put Roger Farrah on the Board and Reed Krakoff could do whatever…but it will cost money, and earnings.

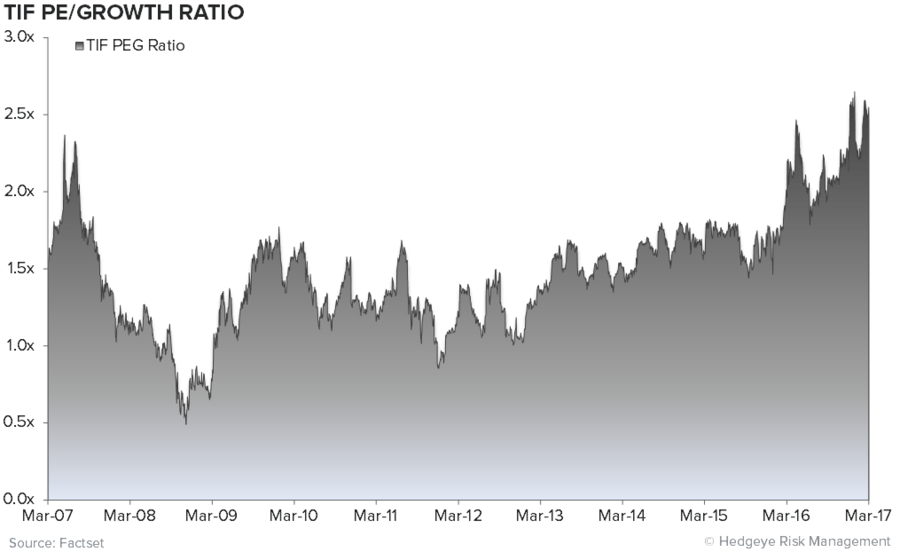

- I'm elevating this on my Short list -- from #13 to #5 (out of 22). TIF is trading a cycle-high p/e (24x) and EBITDA (12.5). That's bad enough, but get... at the same time growth is structurally challenged, it is trading at a new peak all-time high PEG. That tells me that this company either needs to a) get bought (no), b) accelerate comp meaningfully (no), or c) beat earnings expectations by 20-30% (no).