***Below is an institutional research note written by Hedgeye Senior Macro analyst Darius Dale

Recently, Keith added the iShares MSCI Mexico Capped ETF (EWW) to Investing Ideas as a short. The crux of our structural bearish thesis on Mexico is quite simple:

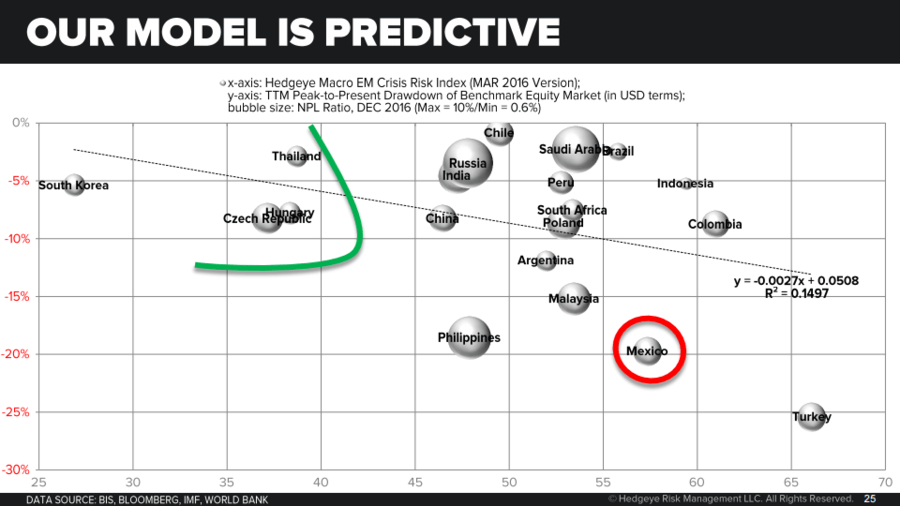

“Consistent with our view that the U.S. Dollar remains in a secular bull market, we remain predisposed to be short of Emerging Markets that have structural Balance of Payments (BoP) risks. Mexico, with its massive current account deficit, over-reliance upon foreign investment to finance growth and poor positioning within its domestic #CreditCycle, screens almost as poorly as any EM economy on our proprietary 20-factor EM Crisis Risk Index.”

For example:

- As a ratio to GDP, Mexico’s Current Account Balance of -3.3% compares to our EM sample average of -1.6%.

- As a ratio to FX Reserves, Total U.S. Dollar Debt in the Mexican Economy amounts to 141%, which compares to our EM sample average of 97%.

- As a ratio to FX Reserves, Short Term External Debt in the Mexican economy amounts to 29%, which compares to our EM sample average of 19%.

- Capital flight risk in the Mexican banking sector is exacerbated by the fact that the Turkish lira is -2.5 standard deviations below its trailing 10Y average on a Nominal Effective Exchange Rate (NEER) basis.

- The aggregate Debt Service Ratio in Mexico’s Private Nonfinancial Sector is +2.7 standard deviations above its trialing 10Y mean, which compares to our EM sample average of +1.0. Recall that a rapid increase in Debt Service Ratios have historically been a trigger for sharp deleveraging episodes in both developing and advanced economies.

- This is on top of Private Nonfinancial Sector Leverage that is +2.3 standard deviations above its trailing 10Y mean as a ratio to GDP. The takeaway? The Mexican private sector is getting squeezed at its highest rate ever at its most indebted point.

- And here’s the kicker: the aggregate NPL Ratio across the Mexican banking sector is only 2.3%, which compares to the prior cycle peak of 11.3% (1998). We’re not suggesting that Mexico is poised to see a retracement to such elevated levels anytime soon, but it is fair to suggest that a downturn in asset quality is more than likely ahead of the Mexican economy than behind it.

Moreover, given its reliance upon international capital to finance economic activity, we don’t have any confidence that the Mexcian economy can exhibit a sustained economic recovery to the extent we’re right on our call for the dollar to grind 10-20% higher from here over the intermediate term.

One additional risk factor we continue to call out is the elevated risk of protectionism from the Trump administration. While we refuse to structure any investment thesis around what may or may not happen in D.C., we can rest assured that the Trump overhang upon Mexican financial assets is unlikely to dissipate anytime soon – especially given Mexican President Pena Nieto’s soured relationship with the Don.

And then there’s this deep cover political intel from our boots on the ground in Mexico City which suggests an internally-driven political overhang may develop over the intermediate term:

“I just wanted to flag that there are also some pretty big tail political risks. The extreme left wing party Morena are 2 points behind in the polls for the Federal Election in mid 2018. They are socialists, against the oil reforms, and have an anti-trump platform. They aren’t winning now but the feeling is that the head of the Right wing party PAN, Margarita Zavala is not a great candidate. And the 7 points currently polling for PRD (moderate left) will likely go to Morena. I don’t think they are going to end up like Venezuela – but I don’t think the political risk is baked in.”

-Insider with the CIO of the Mexican Electoral Commission

All told, we think the relief rally to lower-highs in Mexican financial assets is long in the tooth and are keen to reiterate our bearish bias.