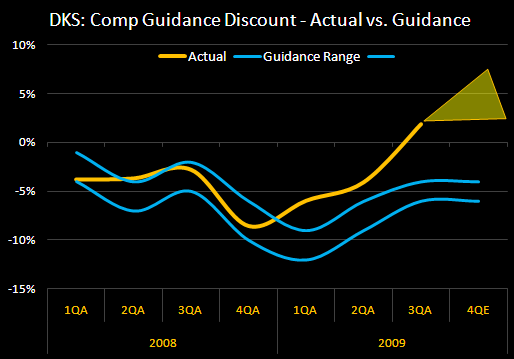

The company printed a solid quarter, but as evidenced below it suggests a massive roll in 4Q top line. They’re going to need to give solid detail as to why this should be the case.

The company printed a solid quarter, but as evidenced below it suggests a massive roll in 4Q top line. They’re going to need to give solid detail as to why this should be the case.

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.