MARKET WATCH: What’s Happening? Since 2012, Priceline and Expedia have acquired nearly every OTA and travel metasearch company on the market. Once just an additional revenue stream for hotels, these OTAs have transformed into profit-eating giants. In response, the largest hotel operators are going all out to win back direct bookings.

Our Take: Despite these efforts, the future looks bright for OTAs. Increasingly, OTAs are driving sales away from the hotel industry and toward sharing-economy sites like Airbnb. And Millennial travelers are not tempted by the loyalty programs that hotels are pushing. Instead, they simply want a hassle-free travel experience—which is exactly what OTAs provide.

Hilton, in the midst of a marketing campaign designed to encourage direct bookings, recently agreed to list its rooms on TripAdvisor’s (TRIP) Instant Booking platform.

At first glance, this deal seems counterproductive to Hilton’s direct-booking mission. But it illustrates the complex relationship that hotels have with online travel agencies and metasearch engines. On the one hand, third-party bookings remain a valuable source of publicity and revenue that most hotels can’t afford to ignore. But on the other hand, deals with Priceline (PCLN) and Expedia (EXPE) also carry huge—and growing—commission fees.

It wasn’t always so complicated for hotels. Prior to 1996, travelers had two choices: book direct or speak to a travel agent. But that all changed when Microsoft spun off its subsidiary, Expedia, in 1996. Priceline was formed by entrepreneur Jay Walker the following year. While these OTAs originally were limited to hotel bookings, today they can help consumers book a cruise, rent a car, or find a flight.

The ensuing rise of so-called “metasearch engines” like TripAdvisor, Kayak.com, and Orbitz gave travelers a one-stop shop on which they could find the best deal, period—whether that deal was available via direct booking or through an OTA.

Today, two enormous OTAs control the vast majority of the OTA and metasearch universe. The clear leader is Priceline, a $76 billion behemoth that since 2012 has acquired brands such as Booking.com, Kayak.com, and RentalCars.com. Expedia is much smaller, worth a comparatively miniscule $18 billion. But the company boasts an equally impressive portfolio of brands—including Hotels.com, Travelocity, and Orbitz.

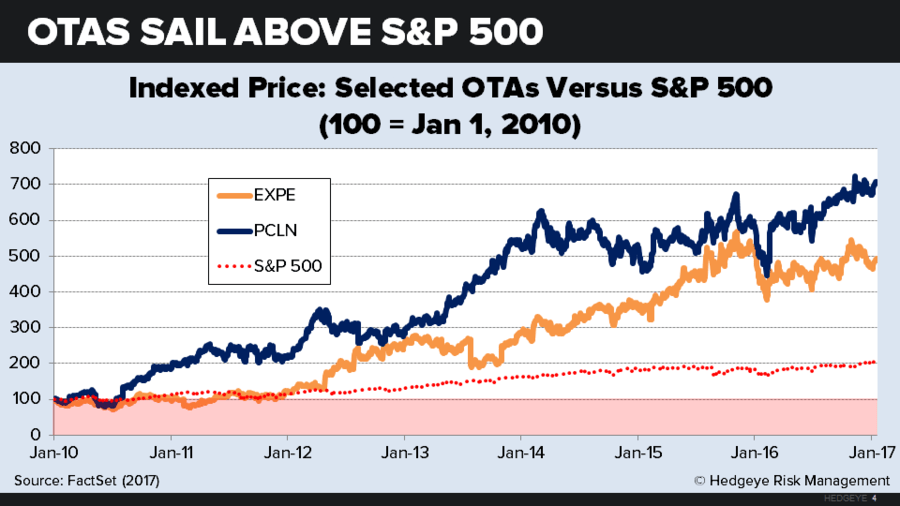

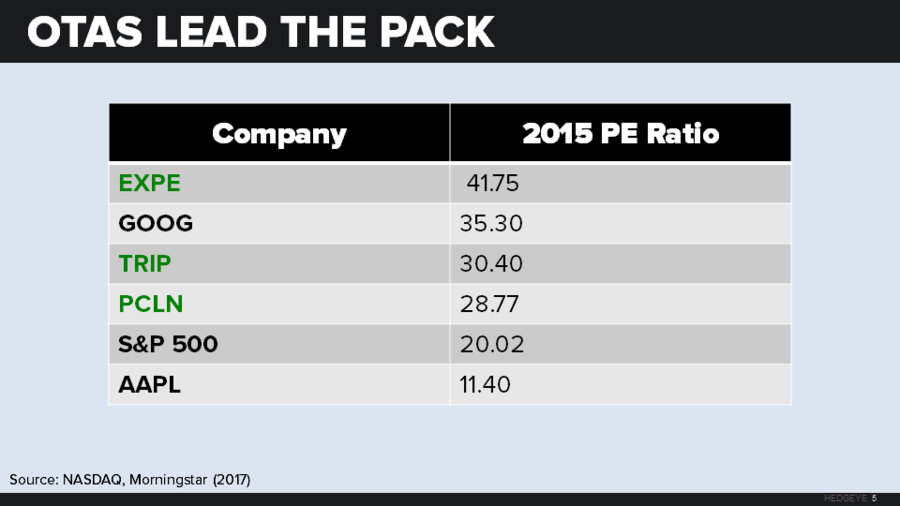

These stocks are highly coveted by investors. Priceline costs a massive $1,500 per share, making it the S&P 500’s single priciest company. Sticker shock hasn’t kept analysts like Paul La Monica from proclaiming that Priceline is worth every penny. Both Priceline and Expedia stocks have soared far higher than the S&P 500 since 2010. If anything, investors appear more bullish on Expedia—given its sky-high P/E ratio of 106. (Priceline’s P/E is a more “reasonable” 39.)

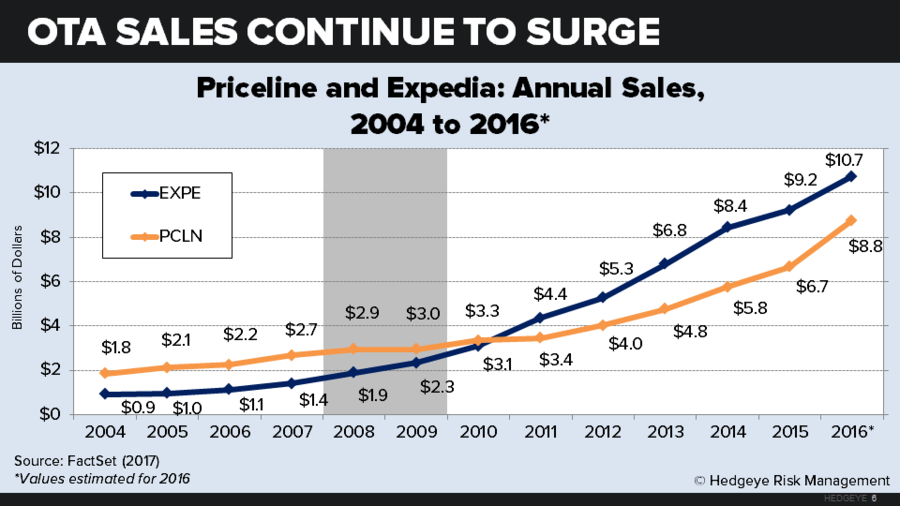

It’s tough to argue with this optimism, judging by the continued sales growth posted by these companies over recent years. Annual sales revenue has nearly tripled for Expedia since 2010 (from $3.3 billion to $8.8 billion), while growing even faster for Priceline ($3.1 billion to $10.7 billion).

How do these firms make money? OTAs operate under one of two business models. The first is the “agency model,” whereby the OTA lists deals and makes a cut of each transaction. Priceline generated 93% of its gross bookings through its agency segment in Q1 2016. Though this model gives Priceline little control over inventory (rooms, flights, etc.), it frees the company from inventory risk—one reason why Priceline regularly attains annual operating margins above 35% of earned revenue.

Alternatively, Expedia relies more heavily on the “merchant model,” whereby OTAs purchase inventory and resell it to travelers. Expedia earned 44% of its gross bookings through this channel in Q1 2016. Though merchant OTAs face high upfront costs (the price of buying a block of hotel rooms) and high inventory risk (the prospect of not selling those rooms), they are free to repackage and resell the rooms however they want.

ONLINE TRAVEL AGENCIES: A DOUBLE-EDGED SWORD

For years, OTAs and hotels enjoyed a valuable synergy. OTAs raked in profits without having to spend anywhere near the overhead of hotels, while hotels could move unsold inventory and enjoy an instant popularity boost. A 2009 Cornell University study highlighted the extent to which hotels can profit from the additional popularity: Thanks to what researchers call “billboard effect,” a hotel listed on Expedia can expect to see its direct bookings spike by as much as 26%. That’s not even counting the obvious subsequent boost in third-party bookings. In the early days of OTAs, when commission fees typically averaged around 5%, the partnership was a no-brainer for hotels.

Since 2015, however, the story has changed. Not only is the number of transactions booked through an OTA rising, but so is the commission rate per booking. By 2015, 27% of all hotel bookings valued at $100 per night or more were carried out by a third party—up from just 19% in 2011. As a function of growing OTA market concentration, Priceline and Expedia have ramped up their commission rates to as much as 30% of each transaction.

Combined with slowing hotel revenue growth, these rising commissions have seriously eaten into hotels’ bottom lines. In 2015, hotels experienced 10% YOY growth in commissions and wholesale transaction costs—far above the industry’s 7.3% revenue growth.

HOW HOTELS HAVE RESPONDED

All of the largest hotel chains have embarked on expansive direct-booking marketing campaigns encouraging loyalty signups. Their reasoning is clear. Though “rate parity agreements” bar hotels from undercutting OTA prices, these contracts only apply to rates offered to the general public. Hotels can offer lower rates to a select group of customers—say, loyalty members—without violating rate parity.

In 2015, Marriott became the first hotel giant to try this approach with its #itpaystobookdirect campaign advertising its lower member rates. Last year, Hilton released its largest-ever marketing campaign, “Stop Clicking Around,” which extended direct-booking discounts to all loyalty members. Hyatt announced a 10% discount for Hyatt Gold Passport members who book through the hotel website or app.

Do OTAs feel threatened by these tactics? Not publicly: In a Q2 2016 earnings call, Expedia executives brushed aside a question about whether direct-booking campaigns caused a YOY slowdown in booking growth. Industry forecasters claim that the impact of these programs is negligible. Consultancy Morningstar predicts that direct-booking campaigns will create headwinds of just 1% for Priceline, and 1.5% for Expedia, through 2020.

But based on their actions, OTAs are starting to show real concern. Expedia reportedly strips descriptive details (such as pictures) out of certain hotel listings, while Booking.com “dims” offending hotels by lowering their favorability ratings.

WHICH SIDE WILL PREVAIL?

So how will the direct-booking war play out? The future looks brightest for OTAs.

To be sure, OTAs face one significant headwind in the years to come that could limit their growth: metasearch. Sites like TripAdvisor were once simple ad-supported price comparison sites that would send users to an external site to book deals. But increasingly, these sites are encroaching on what OTAs do: Orbitz, TripAdvisor, and others now allow users to book directly on the site.

Low barriers to entry make it relatively easy for young metasearch firms to strip away OTA revenue and force a buyout. Yet the number of unaffiliated metasearch firms is growing just as quickly as Priceline and Expedia are gobbling them up. Massive YOY revenue growth spurred Trivago (TRVG) to go public last month, while even Google (GOOGL) has dipped its toes into metasearch by offering everything from airfare forecasts to exclusive hotel deals through its Maps app.

Yet hotels face many more significant obstacles.

The emergence of sharing-economy lodging options. Both hotels and OTAs are snatching up sharing-economy upstarts. Back in 2014, Hyatt invested in upmarket, U.K.-based firm Onefinestay through a joint pilot program and a round of funding. The company was then purchased last year by French hotel group Accor. Expedia, meanwhile, bought HomeAway for $3.9 billion in late 2015.

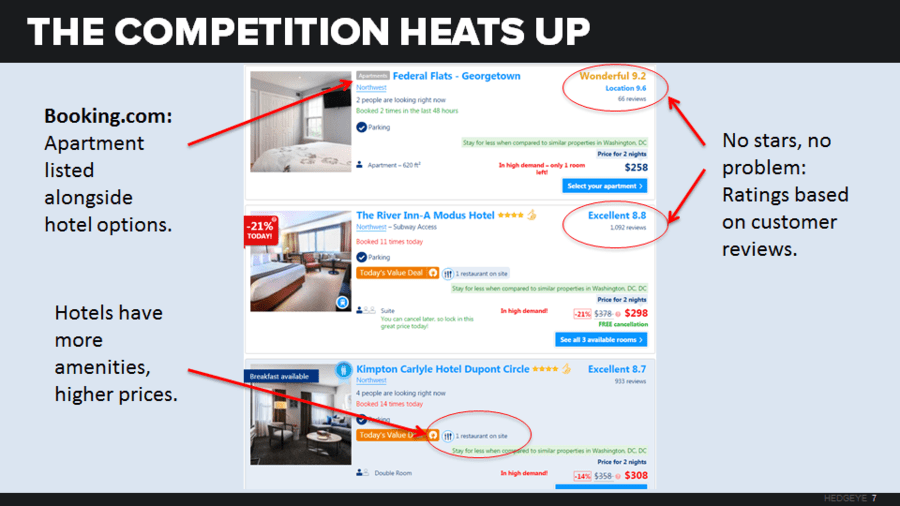

These deals have completely reshaped the travel booking experience for users. Priceline-owned Booking.com contains 7.3 million listings’ worth of “alternative accommodations” (think apartments, B&Bs, etc.) that travelers can view alongside traditional hotel rooms. This is a nightmare scenario for hotels, effectively transforming the sharing economy from a niche alternative into a full-blown competitor.

Changing generational currents. The preferences of today’s Boomer and Xer travelers have been a tailwind for the hotel industry. According to a 2014 Deloitte study of frequent travelers, Boomers are the most likely generation to be members of four or more loyalty programs (at 35%). Armed with these memberships, relatively few Boomers would risk losing out on their Hilton points by scouring Kayak.com for a deal. Xer travelers, meanwhile, are looking for the best value—and could be drawn in by rewards programs featuring cash incentives. Additionally, Xers don’t mind scouring the Web themselves for the best deal—in other words, the entire function of an OTA—if it saves them money.

But Millennials are a different story. Expedia data reveals that OTA customers skew young: Fully 36% are between the ages of 25 and 39, a high figure for an industry heavily weighted toward older customers. Millennials simply haven’t shown much interest in loyalty programs: Deloitte found that only 55% have more than one loyalty membership, the lowest share of any generation. Meanwhile, Millennials are drawn into the simplicity of choice that OTAs offer. To them, a brand like Priceline that curates and automatically selects the best option is showing that it cares about consumers’ time. (See my discussion of why Millennial consumers want fewer, not more, choices: “When Less is More.”)

THE FUTURE OF ONLINE TRAVEL AGENCIES

While today the main battle is between OTAs and hotels, it doesn’t end there. Other travel- and leisure-centric industries are at risk for disruption as well.

Though there has been some talk of airlines trying to win back direct bookings, the airline industry holds the clear upper hand over OTAs. Hotels are losing out because of the vast number of options available to travelers. Someone who wants to stay in New York for the night can choose from hundreds of hotel rooms, motels, and Airbnb listings. Someone wanting to fly from Dallas to New York at a given time may only have the choice of one airline. Price comparison doesn’t do a consumer much good when there’s only one option available.

So which industries feature the same degree of consumer choice as hotels? The rental car business is one. At any given airport there are a vast array of companies, from Avis to Budget to Enterprise, waiting to sell consumers essentially the same product. OTAs could even make a dent in the revenue of ticket sites like StubHub and Ticketmaster. Someone traveling to see their favorite band in concert could find a package deal on Expedia featuring a ticket, a hotel room, and a flight out of town.