RETAIL FIRST LOOK: H&M READ THROUGH

November 16, 2009

TODAY’S CALL OUT

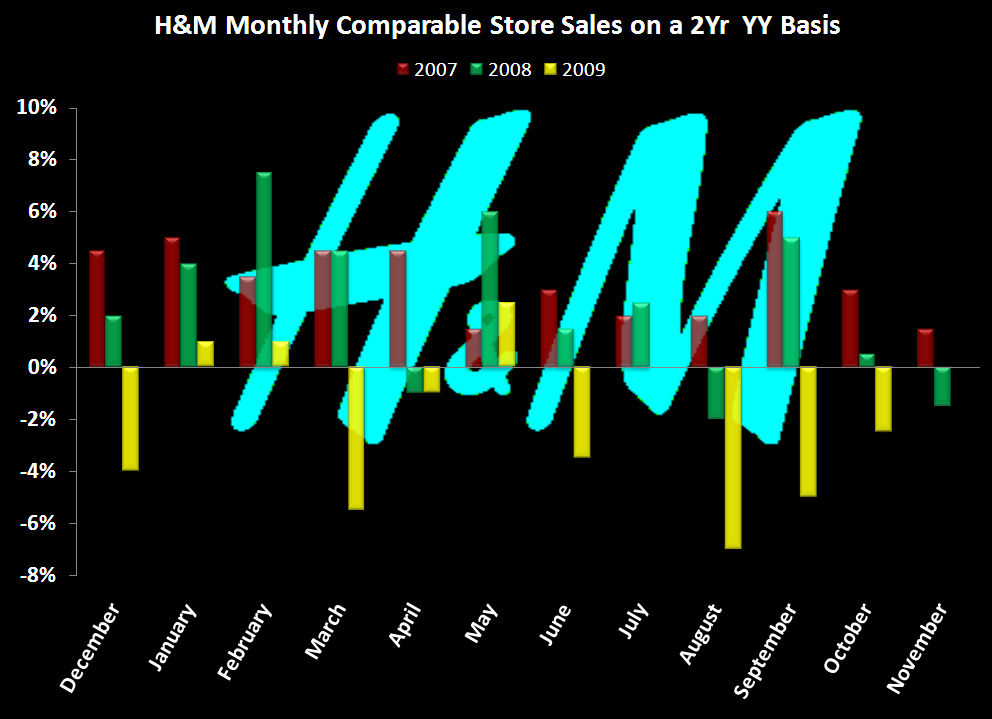

H&M sits near the top of my list of companies I track to keep a pulse on global discretionary spending. Many people underestimate how truly massive and relevant H&M is. But with sales of US$11bn, it compares to Gap, Inc at $15bn. While slightly smaller on the top line, its $2.6bn in EBIT dwarf’s Gap’s $1.6bn. Aside from being one of the largest, most profitable and highest-return apparel companies in the world, it is clearly the most diverse, as evidenced in the first exhibit below. That’s why the headline comp delta improvement for October was interesting to me.

The company highlighted Scandinavia, Central Europe, and Asia as geographic outperformers while France, Spain, and the US had another weak month. This ties in perfectly with what we’re hearing from Matt Hedrick (our Europe guru on our Macro team) in that consumption is picking up across the region, however we’ve yet to see substantial pick-up from the region’s largest economies. The UK reports October Retail Sales this Thursday, which is an important gauge from a Macro perspective. Based on H&M’s results, it does not sound like Western Europe is turning around meaningfully just yet…

LEVINE’S LOW DOWN

Some Notable Call Outs

- JC Penney provided some additional insights into its recent licensing partnership with Liz Claiborne. The namesake brand will be available in Penney stores for the Fall 2010 selling season. The brand is expected to span 30 product categories throughout the store. When surveyed, consumers indicated that Liz Claiborne was among their top three preferred brands, no matter where these customers chose to shop. Management was very enthusiastic for the potential growth of the brand, and indicated that they expect it to double in size over a five year period.

- ANF management was quick to point out that they believe they may have swing the pendulum too far on tight inventory management. As a result, key product categories like denim have been negatively impacted by overly conservative inventory plans. Fashion items, which have sold well, are also unable to make a substantial impact on overall topline results given the low inventory commitments made to “trend” items.

- Score one for Under Armour and the company’s endorsement of Milwaukee Buck rookie, Brandon Jennings. Jennings is the only NBA player currently endorsed by Under Armour and was the first player picked to wear the company’s prototype basketball shoes. While the rollout of the basketball line is still TBD, we can’t ignore the success of Jennings so far. While he was already the leading scorer on the Bucks and one of the leading rookies in the league so far this year, the attention on Jennings is sure to elevate with his 55 point performance on Friday night (just his 7th game ever in the NBA!). Jennings performance puts him in elite company becoming the first player to score 50 points in the fewest amount of games and also surpassing Lew Alcindor’s franchise record for scoring the most points as rookie. With this success, we wonder how long it will be before the UA hoops collection finally makes its way into retailers.

MORNING NEWS

Obama to Seek Increased Trade in Asia - Speaking during his first trip to Asia since taking office, President Obama indicated over the weekend that the U.S. will seek to increase its engagement in trade in the region. Obama announced Saturday the U.S. will work with Vietnam, Singapore, Australia, Peru, Brunei Darussalam, New Zealand and Chile to shape a broader regional agreement out of the existing Trans Pacific Partnership (TPP) free trade area. Obama also indicated that the administration would engage South Korea in talks to work through outstanding issues keeping the stalled U.S.-Korea free trade agreement from moving forward, and pledged to continue working aggressively on the Doha Round of trade negotiations. “We’ve increased our exports to Asia at a healthy rate over the last decade, but not as much as other regions have — and we intend to change that,” Obama said. He delivered his remarks early in a weeklong trip that includes stopovers in Japan, Singapore, China and South Korea. <wwd.com>

U.S. Demand May Take Until Next Year to ‘Regenerate,’ Li & Fung Says - U.S. consumer demand may take until the middle of 2010 to “regenerate,” and it’s unlikely China can fill the gap as the global economy recovers, said Victor Fung, chairman of Wal-Mart Stores Inc. supplier Li & Fung Ltd. “The slide in retail sales has been arrested, but I think it may take a little while before demand will regenerate,” Victor Fung said in an interview in Singapore Nov. 14. “We will look toward the middle of next year for that to come back up, before you can see a perceptible pick up in demand.” Sales at U.S. stores open at least a year rose 1.1 percent in September, the first increase in 13 months, as discounts drew shoppers back to shops. Li & Fung, founded in China in 1906 near the end of the Qing Dynasty, is accelerating efforts to buy makers of clothing, cosmetics, home products, accessories and shoes as retailers increase reordering. <bloomberg.com>

Downside of U.S. Economic Recovery Is Swelling of Trade Gap - The U.S. economic expansion that began last quarter has a downside: the trade deficit will probably swell as imports jump. Purchases of goods made overseas climbed 5.8 percent in September to $168.4 billion, the Commerce Department reported today in Washington. The gain was the biggest since 1993 and reflected growing demand for crude oil, automobiles, metals, machines and even artwork. The figures illustrate the challenge faced by world leaders as they try to rebalance global growth away from American consumption and toward demand in emerging markets. President Barack Obama today began an eight-day trip focusing on trade that will take him from Singapore to Korea. <bloomberg.com>

Walmart Extends AA Rating Benefits to Apparel Vendors - Wal-Mart Stores Inc., the world’s largest retailer, said it’s allowing more than 1,000 apparel companies to benefit from its high credit rating and arrange financing after CIT Group Inc. filed for bankruptcy. Walmart wrote a letter to its apparel makers on Nov. 2, a day after CIT’s bankruptcy filing, saying they can “take advantage of Walmart’s AA credit rating to secure financing to manufacture and deliver products for our stores,” John Simley, a company spokesman, said today by telephone. The retailer is working with Wells Fargo & Co. and Citigroup Inc. to have them pay vendors between 10 and 15 days from receipt of goods in Walmart stores, the letter said. The banks can provide the funding at attractive rates with the understanding that Walmart will pay them directly and on a timely basis, Walmart said. <bloomberg.com>

China, Japan Say Fed’s Low Rates Fueling Speculation - Financial officials in Japan and China, Asia’s two largest economies, warned the Federal Reserve’s interest-rate policy risks spurring speculative capital that may inflate asset prices and derail the global economic recovery. Emerging economies “might overheat and experience financial turmoil,” Bank of Japan Governor Masaaki Shirakawa said in Tokyo today. Low rates and the dollar’s depreciation present “new, real and insurmountable risks to the recovery of the global economy,” Liu Mingkang, China’s top banking regulator, said yesterday. The comments reflect concern that the Fed’s pledge to keep rates near zero for an “extended period” may lead to a repeat of the financial crisis. MSCI’s emerging-markets stock index has risen 71 percent this year and Asian countries from Singapore to South Korea are trying to rein in surging real-estate prices. <bloomberg.com>

China, Vietnam Gain as Imports Fall in Sept. - Textile and apparel imports to the U.S. from China and Vietnam increased in September, but shipments from the other top suppliers continued to decline. The Commerce Department’s Office of Textiles & Apparel said Friday that imports from China gained 3.2 percent to 2.2 billion square meter equivalents, driven by a rise in apparel shipments. Apparel imports from China grew 12.1 percent to 1.1 billion SME, and textile shipments fell 4.4 percent to 1.1 billion SME. Textile imports from Vietnam helped propel an increase in total textile and apparel shipments of 14.3 percent to 199 million SME. Textile shipments to the U.S. from Vietnam spiked 116.8 percent in September to 54 million SME; apparel imports dipped 3 percent to 144 million SME. Vietnam was also the only top textile and apparel supplier to increase shipments to the U.S. for the year-to-date period, rising 20.5 percent to 1.6 billion SME. <wwd.com>

H&M's October sales drop but Jimmy Choo range is a success - H&M sales were worse than expected in October, down 3% on a like-for-like basis. The Swedish fashion giant said that sales in Scandinavia, Central Europe and Asia were satisfactory during October but that the performance in other markets including France, Spain and the US continued to be weaker. Total sales across the group grew 7% in October compared to the same month the previous year. The results came as H&M opened its doors to its latest designer collaboration, this time with Jimmy Choo which drew crowds across the country this weekend. H&M said it was “delighted” with the launch of the much-hyped range. There were long queues outside of the 19 stores in the UK and Ireland that carried the collection, which launched at 9am on Saturday morning. <drapersonline.com>

Japan Q3 GDP Grows Faster Than Expected - Japan’s third-quarter gross domestic product grew at a faster-than-expected rate but longer-term concerns about the health of the economy and deflation persist. Japan’s real GDP rose 1.2 percent in the July to September period from the prior quarter, the Cabinet Office said Monday. That figure reflects 4.8 percent growth on an annualized basis for the world’s second-largest economy. Stimulus measures, both in Japan and other countries, are considered responsible for much of the jump. Japan officially emerged from recession in the second quarter of the year. GDP for the April to June period rose 0.7 percent, revised downward from an original estimate of 0.9 percent growth. Still, concerns about Japan’s job market and overall economic health linger. The government is preparing to declare that the Japanese economy is in official deflation, according to a Cabinet Office spokeswoman. <wwd.com>

European October Consumer Prices Fall for Fifth Month - European consumer prices declined for a fifth month in October as rising unemployment discouraged household spending. Prices in the 16-nation euro region declined 0.1 percent from a year earlier after falling 0.3 percent in September, the European Union statistics office in Luxembourg said today. That matched an initial estimate published on Oct. 30 and the median forecast of 35 economists in a Bloomberg survey. In the month, consumer prices rose 0.2 percent. European companies have been forced to cut prices and eliminate jobs to survive the worst global recession in more than six decades. While the region’s economy returned to growth in the third quarter, rising unemployment has undermined consumer spending. <bloomberg.com>

Q&A With Jones Apparel Group: "We can't keep [enough] boots in stock" - “We really [have been] focused on getting the house in order and getting the core brands running well,” Card said in a recent interview. “The economy is still tough, and it’s a tough period to operate in, but we’re still doing as well as we can — and better than others. We’re well positioned for when the recovery really starts to take hold.” Meanwhile, as other companies have scaled back on new initiatives, Jones continues to invest in growth, this year launching Rachel Rachel Roy, an exclusive contemporary brand at Macy’s; a Vintage America collection within its Nine West brand; and the Shoe Woo retail concept, which offers a multibrand approach to footwear shopping. In the last few weeks, in particular, footwear has been a bright spot for the firm, thanks to brisk boot sales. “We can’t keep boots in stock,” Card said at last week’s Women’s Wear Daily CEO Summit. “[Shoppers] are buying boots like there’s no tomorrow. When consumers see an item they really want, [they’re buying it].” <wwd.com>

GM to start repaying loans soon - General Motors Co. will announce on Monday it plans to start repaying a $6.7 billion loan to the U.S. Treasury by year-end due to modest operating improvements, a source knowledgeable about the situation said. GM, due to unveil its first post-bankruptcy earnings report on Monday, will begin making $1 billion quarterly installments on the loan on December 31. At the same time, the automaker also will start repaying a $1.4 billion loan to Canada at a rate of $200 million per quarter. GM was not required to make any payments on the U.S. loan before it matured in July 2015, but better-than-expected vehicle sales will let it start repayments much sooner than expected. <canada.com>

American Apparel to Supply US Navy Task Force Uniform Items - American Apparel in Selma, AL received a maximum $8.1 million firm-fixed-price with indefinite-quantity contract to supply items for the US Navy Task Force Uniform (TFU). The original Navy TFU contract was awarded to Wellstone Apparel in 2007; American Apparel purchased Wellstone in 2009. The Navy TFU was redesigned in 2006 to provide a single working uniform for all ranks… The BDU-style working uniform, designed to replace 7 different styles of working uniforms, is made of a permanent press 50/50 nylon and cotton blend. The working TFU includes several cold weather accessories, such as a unisex pullover sweater, a fleece jacket, and a parka. <defenseindustrydaily.com>

Cherokee Heads to Retailer in China - RT Mart Stores, a division of Ruentex Industries Limited, has signed an exclusive international license deal with Cherokee. The multi-year agreement covers a complete range of categories, including men's, women's and children's clothing, footwear and accessories, as well as home textiles. "RT Mart, with its retail knowledge, merchandising and sourcing expertise, creates an ideal partnership for Cherokee in China," says Larry Sass, executive vice president of Cherokee. "By developing distribution in China, we have now achieved another significant goal in our 'world brand' strategy and are proud to have licensed Cherokee in more than 20 countries and five continents. Over the coming months, we plan to build upon our strategy throughout Asia, as well as Australia, Europe, Russia and Latin America." <licensemag.com>

TSA Hires Chief Marketing Officer and Chief Strategy Officer - The Sports Authority appointed industry veteran Jeffrey Schumacher to oversee all marketing, advertising, private brand strategy, digital/eCommerce, corporate and business development strategy. Schumacher, who currently serves as a Partner in McKinsey & Company's North American Marketing and Sales Practice, brings more than 15 years of industry experience in marketing, advertising, sales and brand/retail strategy. Schumacher's appointment to Executive Vice President, Chief Marketing Officer and Chief Strategy Officer is effective November 16, 2009. <sportsonesource.com>

INSIDER TRANSACTION ACTIVITY:

COH: Michael Tucci, President-N. American Retail, sold 92,000 shares after exercising options to buy 75,000 shares for a net gain of $1.8mm.

BBY: Bradbury Anderson, Vice Chairman, sold 51,000 shares after exercising options to buy 30,000 shares for a net gain of $1.4mm.

TUES: Madison Dearborn Partners, 10% Owner, sold 10,300 shares for a gain of $31k.

SHOO: Peter Migliorini, Director, sold 7,500 shares after exercising options to buy 7,500 shares for a net gain of $188k.

FOSL: Jennifer Pritchard, Divisional President, sold 4,000 shares for a gain of $124k.

NFLX: Reed Hastings, CEO, sold 10,000 shares after exercising options to buy 4,500 shares for a net gain of $583k.

ANN: Gary Muto, President-LOFT, sold 6,500 shares for a gain of $91k.