WMT was the antithesis of what we’ve seen this earnings season. If we could characterize what we’ve seen in 3Q to date in a sentence, it’d be this…low quality management teams at the likes of KSS and TGT posted big earnings beats, while underspending on SG&A on negative traffic and soft comps, which = upped guidance for the last quarter of the year. WMT just did the opposite, sales missed (in the US and globally), guidance left something to be desired, and the company spent it’s way to its 7th straight quarter of earnings decline, the last point is what really set this company apart from the rest of big box retail. At 16.5x earnings, that’s not enough for this company to get rewarded over the near-term. But we think the company is taking the right strategic actions (investing in stores, e-comm), putting the capital behind that plan (SG&A/sq.ft. was up 8.5% TTM), in order to continuously win the market share battle – especially in the US market.

Key Points

Better Working Capital = GM Benefit

As we ran our SIGMA analysis on the WMT numbers following the print, the fact that WMT had been in Quad4 for 6 consecutive quarters caught our eye. That’s usually a transitory quadrant which usually = margin expansion on better working capital management. WMT’s elevated SG&A spend obviously skews that metric, but when we look at the numbers just taking into account the GM performance – its clear that the company has made some serious improvements in its working capital management, good for 5 straight quarters of +40bps in GM improvement. And, WMT just comped the comp.

E-Commerce – A Win For WMT

There are a lot of moving pieces on the e-commerce line, total sales growth vs. GMV, Yihaodian divestiture vs. Jet.com acquisition and JD partnership. We look at the adjusted GMV line, which excludes the Yihaodian bit, to judge the efficacy of the e-commerce business this quarter. That was good for 28.6% growth. Jet was incorporated into those results for only 40 days of the quarter, which may explain away 4%-5% of that growth (our estimates no number was actually given). Whatever way you slice it, it was a meaningful acceleration in an area where WMT has underperformed retail and its peer group forever and a day. We’ve noted in the past the tightening spread between WMT and TGT online, and WMT just jumped the shark. We expect continued outperformance as WMT continues to invest in that channel while TGT pulls capital out of the model.

Investment Trends – Favor WMT

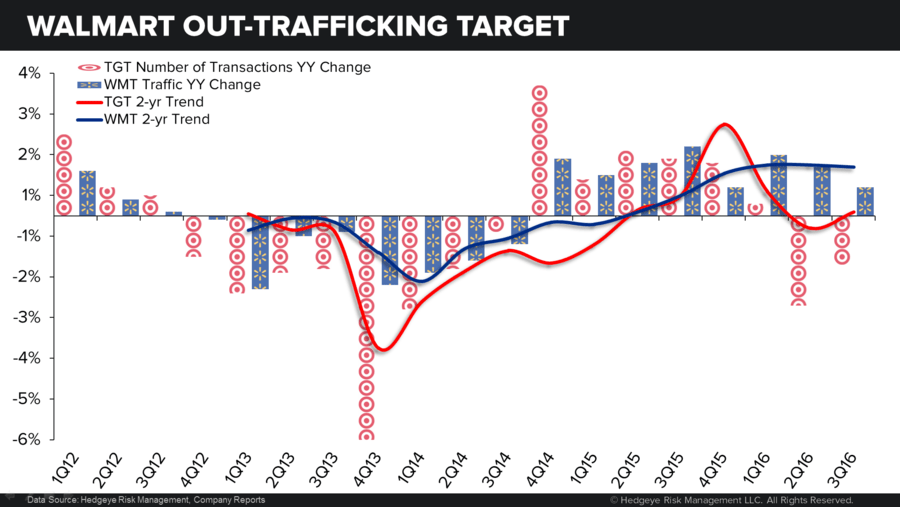

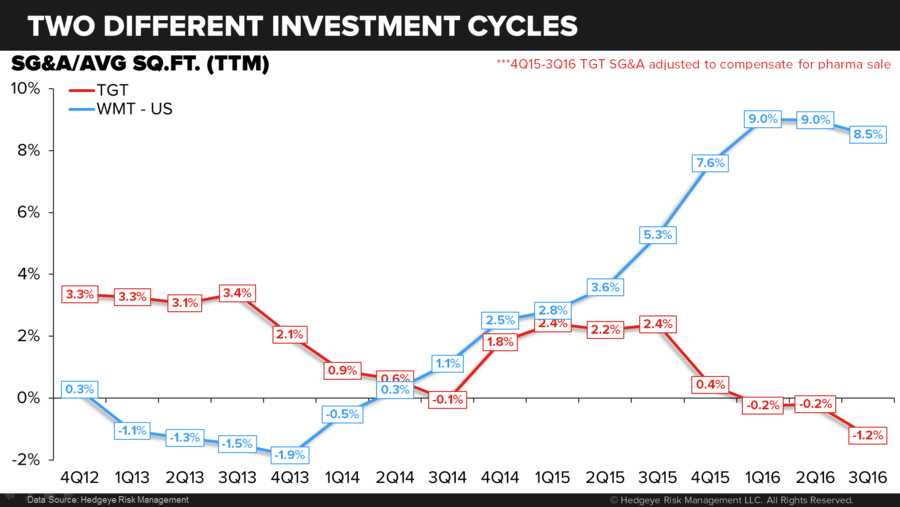

In a quarter where TGT beat earnings expectations by 25%, mostly from cost cuts on the SG&A line, WMT continued its investment behind the business. SG&A sq.ft. was up 8.5% on a TTM basis compared to TGT down 1.2%. That’s good for nearly a 10 point spread between the two retailers. We are hard pressed to see how this ends well for TGT as its biggest competitor dictates the marketplace, and it’s other biggest competitor (AMZN) takes 28% of the incremental consumer outlays. We’ve already seen the divergence in investment between the two retailers manifest itself in a meaningful bifurcation in traffic trends, with WMT at 2yrs of positive traffic, and TGT at 2 quarters of traffic declines. We expect that trend to continue.

Another Win For WMT

This chart speaks for itself. WMT posting a stable improvement in traffic as it infest behind the result, while TGT experiences extreme volatility.