4Q16 healthcare themes conference call

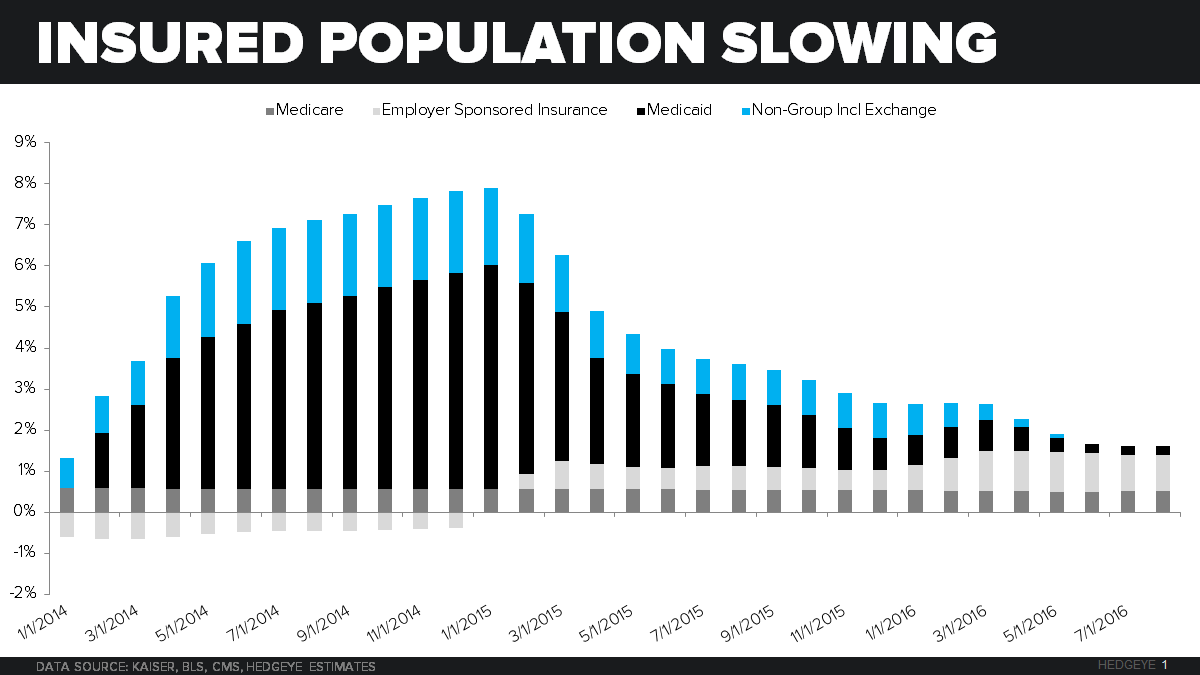

We hope you can join us for our 4Q16 Healthcare Themes Call Today at 1:00 PM ET. We will provide a comprehensive update of our #ACATaper and Healthcare #Deflation themes with new datasets and analysis, including a detailed look at the population of insured medical consumers by month, state, and payor type (chart above).

The U.S. Medical Economy remains extended after the largest expansion in insured medical consumers in a generation. Slowing growth in medical consumers, continued deterioration in affordability, aggressive payment reforms, company leverage at 15-year highs, and multiples at 10-year highs is a recipe for downside. We don't believe that the U.S. Medical Economy growth recovery of 2014 -2015 is durable, but rather a temporary boost in consumption driven by massive government stimulus.

We are also extremely pleased to announce that Emily Evans, Director of Health Policy at Hedgeye, will be joining the presentation and sharing her views on major policy initiatives including Alternative Payment Models, MACRA, and post-acute reform, among other topics that significantly impact our fundamental views.

Please contact for further information. An invite with dial-in instructions will be sent to subscribers ahead of the conference call.

key topics WILL include

#ACATaper Update and Review

Data updates since our JULY 2016 presentation

(continue to progress in line with our expectations for slowing demand)

- JOLTS and Medicaid Pent-Up Demand

- Exchange Enrollment

- Premium/Deductible Affordability

#Demographic Headwinds (YES HEADWINDS!)

Incremental medical spending for the US Medical Economy

(the most profitable in the world, will be sourced almost exclusively from Medicare, one of the least profitable payors with mounting deflationary pressures.)

- Impact of Aging Population

- Per Capita Spend by Age Cohort

- Utilization History

#Recession Risk

Hedgeye Macro Has Been Highlighting Risk to U.S. Growth

(which is negative for the U.S. Medical Economy)

- Employment vs. Privately Insured

- Hospital Bad Debt Expense

- Real Private Fixed Investment

- Biotech Fundraising Cycle

#Cleansweep Policy Post Election

(Emily Evans will provide her outlook for post-election policy pressures which are likely to deteriorate further if Democrats make a clean sweep in November)

- Major healthcare issues that have crystalized during campaign including affordability of health insurance, drug prices and public option

- Implications to those issues if:

- Democrats win White House and gain majorities in House and Senate

- Republicans win White House and retain majorities in House and Senate

- Government remains divided

- Major healthcare issues that have not moved to the fore but have bi-partisan support include addressing mental health and substance abuse, elimination of certain ACA-related taxes and payment and delivery reform

#Defensive Long Healthcare Positioning Looks Like Consensus...

(and likely a bad idea here)

Healthcare As A Safe Haven Looks Like Consensus...

(likely to unwind if we are right on emerging fundamental and policy headwinds)

- Style Factor and Surprise Analysis

- Estimate Revisions

- Relative and Absolute Valuation

Please call or e-mail with any questions.

Thomas Tobin

Managing Director

@HedgeyeHC