“We assume that common goals bind groups together, but reality is they often drive groups apart.”

-Adam Grant

When thinking about “policy makers” vs. the rest of us, I think that’s a good quote. Do I think these people actually want to do something like raise rates into a slow-down? No. Do they realize the economy continues to slow? Obviously not.

“According to Dartmouth psychologist Judith White, a lens for understanding these fractures is the concept of horizontal hostility” (Originals, pg 117). While a common goal may have been to inflate US stocks, forever… rate hike rhetoric is driving returns lower.

Sure, you might say “it’s only 25 bps.” But that small “difference” in rates created a wide gap of portfolio performance when the Fed raised rates into a slow-down last time (December). If they raise (again) this December, I think they’ll be cutting rates (again) by Q1.

Back to the Global Macro Grind…

Double-dip US Earnings #Recession, another leg-down in China, Brexit crashing the British Pound, and @Hedgeye cutting its Q3 GDP forecast (again) this morning… perfect time to raise rates, eh?

You go, rate hike pros… you go!

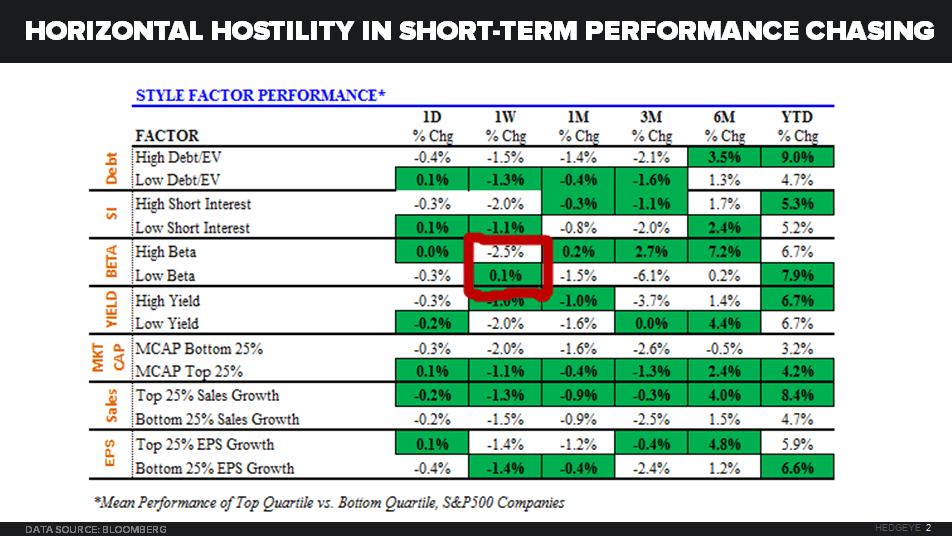

Unlike Odell Beckham’s performance yesterday (222 yards, 2 TDs, and 55 Fantasy Points), High Beta, as a US Equity Style Factor, got rolled by the Low-Beta Defense last week:

- High Beta -2.5% to +6.7% YTD

- Low Beta +0.1% to +7.9% YTD

*Mean performance of Top Quartile vs Bottom Quartile, SP500 Companies

That shouldn’t surprise anyone who watched Week 1 of Q3’s Earning Season. Hopefully, whoever was calling for a “bottom in Earnings” and a “weakening US Dollar” only had that idea on in #Fantasy too.

In terms of the flow-through on another #StrongDollar move, here’s how the Currency War played out last week:

- US Dollar Index +1.5% on the week, taking its 1-month gain to +2.9%

- British Pound -2.0% on the week, taking its 1-month loss to -7.9%

- EUR/USD -2.0% on the week, taking its 1-month loss to -2.5%

Since I reiterated our long-term super cycle case for the US Dollar on our Q4 Macro Themes Call (and reiterated the short Euro call on #EuropeImploding), in #FF (FX) I’m still cool with playing USD at RB2 (Gold at RB1). Watch-out below if the Euro snaps $1.05.

While most things you’d expect to get smoked on #StrongDollar, Weak China did get smoked last week, Oil (WTI) was still able to get another +1.0% out of the “Freeze” tag game that OPEC and Putin are playing with US day traders:

- WTI Oil +1.0% on the week, to +16.1% YTD

- Basic Materials (XLB) stocks -1.2% on the week to +6.7% YTD

- Copper -2.7% on the week to -2.3% YTD

- Hang Seng -2.6% on the week to +6.0% YTD

- Cattle and Hogs -5.8% and -0.9% to -26.0% and -31.2% YTD, respectively

I know. Who the heck (at the Fed or on the Old Wall) cares about US farmers and miners anymore anyway? Everything in #StrongDollar Rate Hike land (i.e. Dollar based asset #Deflation) is awesome, remember?

Sure, we’ll probably get another “higher than expected” inflation report this week (CPI is reported tomorrow), but with 5-year forward US break-evens only at 1.57% and the Fed’s preferred inflation calculation (core PCE) sub 2%, that’s not enough to “hike.”

Or maybe I should say, ‘it’s not enough to validate a hike’… especially if we get 1 or 2 more #EmploymentSlowing reports. Never forget that Janet is primarily a Labor Economist. So all of this rhetoric from Rosengren doesn’t matter if US Labor continues to slow.

While Oil’s developed a short-term POSITIVE correlation to USD, broadly speaking asset prices do not like “rate hikes”:

- SP500’s immediate-term inverse correlation to USD is now -0.72

- Gold’s immediate-term inverse correlation to USD is now -0.88

- CRB Index’s immediate-term inverse correlation to USD is now -0.67

And obviously my Long-term Bonds feel like this every time the Fed gets cocky, albeit from a lower-long-term-high in the 10yr Yield just about every time (7x in the last 17 months).

With the US Stock market (SP500) down for the last 2 weeks and -1.4% in the last 3 months, the good news is that sentiment is souring for both SPYs and Gold. Unfortunately for small cap and Oil bulls, consensus remains too bullish:

Looking at the positioning from a CFTC non-commercial futures & options perspective, here are those points:

- SP500 (Index + Emini) net SHORT position of -3,767 contracts is +0.2x on a 1yr z-score

- Russell 2000 (mini) net LONG position of +12,892 contracts is +1.7x on a 1yr z-score

- 10YR Treasury net LONG position of +17,317 contracts is 0.00x on a 1yr z-score

- Oil’s net LONG position of +458,776 contracts is +2.23x on a 1yr z-score

- Gold’s net LONG position of +153,776 contracts is +0.05x on a 1yr z-score

In other words, just like heading into DEC of last year, consensus is stuck chasing small cap (and High Beta) US Equities in hopes of rectifying performance problems… and missing another chance to buy Long-term Bonds and Gold into the next leg of the slow-down.

While we all have a common goal to generate high single digit (or double digit) % returns this year, reality is that our differences in future growth, earnings, and rate hike views have driven us apart. There’s plenty of horizontal hostility in that.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.58-1.84%

SPX 2123-2153

RUT 1

VIX 14.02-17.44

USD 95.60-98.75

Oil (WTI) 46.39-51.79

Gold 1

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer