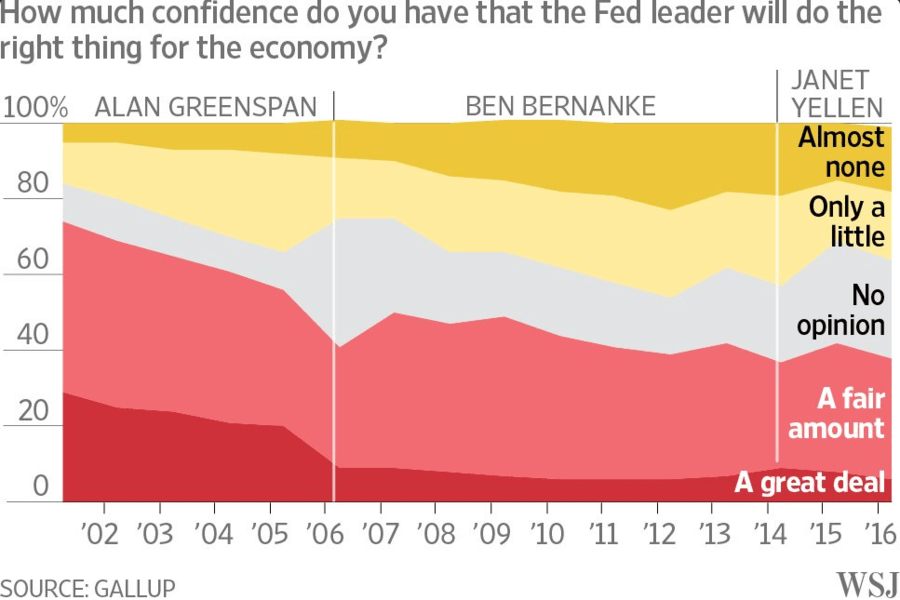

According to Gallop polls, there has been a 14-year slide in confidence that the "Fed leader will do the right thing for the economy?"

Shocker, we know...

Source: WSJ

Fed head Janet Yellen did little to inspire confidence at yesterday's FOMC press conference with statements like this:

- “Asset values aren't out of line with historical norms.”

- “The Fed wants the expansion to last as long as possible.”

- “There is little risk to falling behind the curve in the near future so the FOMC can be gradual in its rate hikes.”

What Does the Fed's Confidence Crisis have to do with Gold?

As Hedgeye CEO Keith McCullough points out in the video below, "Gold loves the blowup of the central planning belief system."

Make no mistake, the central planning #BeliefSystem failing. And fast.