In the latest in a series of episodes in which corporate America exhibits tone deafness, AET announced that it was exiting many of the Affordable Care Act exchanges. Complicating public perception of AET’s decision is the fact that the Department of Justice had highlighted the decreased competition on the ACA exchanges were the AET/HUM merger to proceed. Since, AET had, as recently as May, expressed confidence in its exchange business, their announcement on withdrawal looks more like a game of hardball to effect merger approval. Unfortunately for AET, the other team appears completely uninterested in the game.

AET’s announcement, of course, played into the confirmation bias of many in America that believe a.) The ACA is just fancy websites that sell insurance; b.) No insurer wants to sell their insurance there; and c.) Ergo, the ACA is doomed. The government’s reaction to the AET announcement was a big “meh” – not what you would expect if you subscribe to theories a.) thru c.) above. The government reaction suggests a number of things worth keeping in mind as we enter the second phase of the ACA’s impact which the Hedgeye Health Care team has so astutely titled #ACAtaper:

- No longer fixated on economy wide employment growth, the Obama administration has turned its considerable administrative influence to encourage health care innovation and those that pursue it.

- A large part of the focus is on encouraging payers to shift from fee-for-service to alternative payment and delivery systems.

- A paradigm shift for commercial insurers who influence the health care spending of the 160 million Americans enrolled in employer-based insurance will inevitably lead to slower growth in the medical economy.

From the government’s perspective, it would seem that AET’s departure represents more of an opportunity for reform than a death spiral of the individual insurance markets. AET’s experience with the exchanges would seem to suggest that maybe, they just don’t get it.

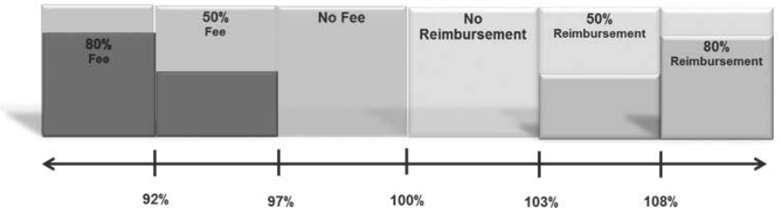

ACA Exchange History. AET entered the exchange market in 2014 with participation in 17 states. In that year, AET appears not to have managed its risk pool well, based on scheduled risk corridor payment calculations. The risk corridor program was designed so that an insurer that spent 97 percent or less of premiums collected for exchange plans would pay a portion to the government. Those insurers that spent 103 percent or more of premiums would get an offsetting payment from the U.S. Treasury. Chart 1 provides a graphic illustration of this arrangement.

Chart 1: Risk Corridor Payment Calculation

It was early in the game and the ACA had suffered a semi-tragic roll-out with a botched launch of the healthcare.gov website but the 2014 scheduled risk corridor payments provide a proxy of sorts for claims and premium experience (2015 data are not available). Risk corridor payment or receipts at or near zero would indicate good management of care costs and utilization versus premiums.

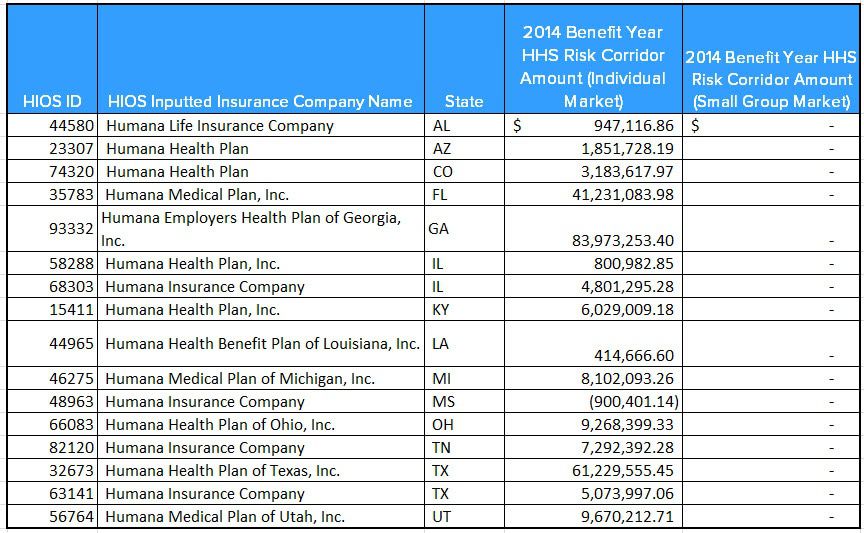

It appears the AET branded insurers balanced things pretty well out of the gate. The Coventry unit was another matter. Three AET branded insurers – in Pennsylvania, Washington, D.C. and Virginia – paid the government $1.1 million. The small group AET branded insurer in Washington D.C. paid out $600,000 because premiums exceeded claims by more than 3 percent. Six AET branded individual insurers – Arizona, Illinois, Pennsylvania, Oklahoma, Texas and Utah were scheduled to receive just over $4.0 million from the government. Not too bad considering, in terms of risk assessment, AET was driving blind.

However, in terms of balancing claims and premiums, the Coventry unit of AET faired more poorly. One Coventry insurer – in Delaware – paid the government just under $100,000. The rest of the Coventry insurers in Oklahoma, Iowa, Illinois, South Carolina, Kansas, North Carolina, Missouri and Florida were scheduled to receive payments from the government totaling $115.5 million. Most of the Coventry insurers experienced claims that exceeded premiums by at least 3 percent.

For 2014, AET reported that they had approximately 560,000 members enrolled on the public exchanges. Total medical membership in all AET health insurance programs was about 22 million. Table 1 illustrates the payments and scheduled receipts from the risk corridor program for AET and Coventry.

Table 1: 2014 Benefit Year AET Risk Corridor Payments and Scheduled Receipts

AET’s merger target, HUM had a similar experience with the exchanges as the AET Coventry unit in 2014. At the end of 2014, HUM had 1.1 million medical members in the individual market both on and off the exchanges. Total medical membership in 2014 was 13.8 million.

HUM’s insurance company in Mississippi was the only one whose premiums exceeded claims and enough so that they were required to make a risk corridor payment. Table 2 lists Humana’s scheduled risk corridor payments for the 2014 benefit year.

Table 2: 2014 Benefit Year HUM Risk Corridor Payments and Scheduled Receipts

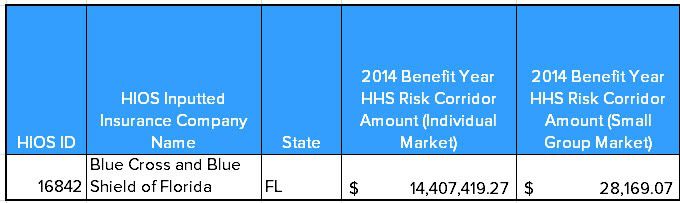

By comparison, Blue Cross and Blue Shield of Florida which has 700,000 members in Florida (2016 data) alone had a different experience. Again using the risk corridor scheduled payments as a proxy for claims and premium experience, it would appear Florida Blue had a better handle on things in that first year of the ACA exchanges. Table 3 presents the same data for Florida Blue.

Table 3: 2014 Benefit Year Florida Blue Risk Corridor Payments and Scheduled Receipts

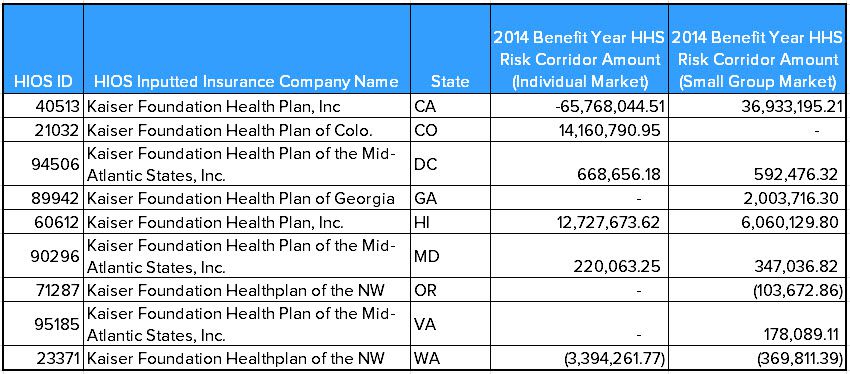

Kaiser Permanente which covers 860,000 individuals most of whom purchased their plans on the exchange also had a different experience than HUM and AET. Table 4 illustrates Kaiser’s experience in the 2014 benefit year.

Table 4: 2014 Benefit Year Kaiser Permanente Risk Corridor Payments and Scheduled Receipts

As it happened, the risk corridor payments were pro-rated due to poor estimates by CMS for receipts and disbursements. The political environment for ACA programs caused CMS to treat the program as budget neutral – meaning it could not go to the Treasury to make up the shortfall. In the end, payments for the 2014 benefit year were reduced to 12.6 percent of the scheduled amount. Risk corridor payments for benefit years 2015 and 2016 are subject to budget neutrality restrictions imposed by Congress. Ultimately what gets paid will be determined at the Court of Federal Claims.

There are a number of reasons, AET and HUM can cite for their relatively poor performance on the health insurance exchange. The major talking points are that the risk pool is unstable, the eligibility system too lax and the risk adjustment program too ineffective to allow for a sustainable program.

Additionally, the Obama administration, under pressure to honor its pledge that Americans could “keep their plan,” delayed enforcement of certain ACA requirements on existing plans until 2017. This decision, to the extent state insurance commissioners went along, meant that a number of already insured individuals delayed entering the risk pool.

Finally, whether it was because of the rocky roll-out of www.healthcare.gov or the economic recovery, employers, especially small employers, did not end their Employer Sponsored Insurance programs in favor of sending people to the exchanges as was anticipated by many policymakers and insurers. People insured through their employer tend to be healthier as indicated by their ability to work. In short, enrollees on the ACA exchanges were much sicker, required more services and provided less premium payment support than originally estimated.

The problem with all these excuses has two parts. First, insurers have had three years to modify their strategy to account for these obstacles. Yet, based on disclosures and public comments, the more claims paying experience they get, the worse their performance. To stem the tide, insurers have resorted to their go-to solution when claims exceeded premium revenue – rate increases.

Second, the excuses offered by AET and others ignore the fact that these challenges are nationwide. Yet regional participants like Florida Blue, Kaiser and other insurers have managed to overcome these obstacles and reiterate their continued involvement in the exchanges.

Government Reaction. Facing a less than innovative response and with ample evidence that a number of insurers are finding success, the Obama administration has shrugged off the AET announcement suggesting, in so many words, that perhaps AET and some others just aren’t up to the task. Specifically, many insurers are not sufficiently engaged, as Medicare has been for the last 18 months, in changing how they pay for care.

In an interview with Dan Diamond at Politico last week (32 minutes of your time you will not regret), Kevin Counihan, the www.Healthcare.gov CEO brushed off the loss of AET as part of the dynamism of the industry and says:

“Some of the big insurance companies…you do not necessarily find that their individual strategic strengths were in the individual health insurance line. Often you found that it was an area of the market that they felt was either harder to understand, had competition they did not necessarily want to match, had administrative expenses that were individually based that were just a little clunky for them and felt they were happier working with the big self-insured market.”

Translated out of the polite government-ese, Counihan is implying AET and perhaps UNH in this context just don’t know what they are doing when it comes to the individual insurance markets.

Now, this a pretty important characterization considering that also in the interview, Counihan identifies as a primary goal of the ACA to convert health insurance from a business-to-business model to a business-to-consumer model. Insurers with little experience with the individual market and no interest in gaining it seem poorly positioned for the future in Counihan's view.

So, too did Counihan seem unconcerned about the rate increases that have been making headlines and serve to buttress the popular wisdom that the ACA is in a death spiral. Of course, the implications of these rate increases are muted by the subsidies and cost-sharing provided to enrollees under 400 percent of the federal poverty threshold. Nonetheless, to Counihan the future does not include insurers that respond to increasing medical expenditures simply with rate increases. He tells Diamond:

“Now, there are a couple ways people are looking at [claims expense and premium rates]. One is that are saying ‘I am looking at my claims, I am just going to add my administrative expenses, add [medical cost] trend and that is my new price.’ Others are saying ‘Wait a minute. Let me look deep into those claims. What type of initiatives could I have taken to actually manage those claims differently, actually do unit cost and what’s the impact that has on price?...I would argue the latter is probably more sustainable.”

In other words, Counihan is sounding the death knell for an industry that has done little to reduce unnecessary utilization and medical cost inflation. In fact, as we alluded to in the context of the DOJ’s intervention in the AET/HUM and ANTM/CI mergers, multiline insurer have relied on dog-eared solutions like narrow provider networks and reduced reimbursement to keep premium increases in check. In the case of their Administrative Service Contracts for self-insured employers, they often haven’t even done that much. Most of the large insurers have eschewed innovative approaches like alternative payment models and use of less costly sites of services in favor of the status quo.

Counihan explicitly makes the point:

“[A} key element of the Affordable Care Act is to encourage innovation and to use the exchange population as a means for issuers to innovate and experiment, see what works and to see if that can be applied to their commercial population.”

Now, if that comment reminds you of things we have said about the CMMI and the spillover of Medicare payment and delivery reforms to the commercial payers and health care providers, you are thinking the right way about where HHS is going with the exchanges and the ACA in general.

Counihan goes on to cite Horizon Blue Cross in New Jersey which requires enrollees to activate their insurance card much like they would a credit card. While they have the enrollee on the phone, Horizon employees conduct a health status interview. He also brings up Blue Cross of Michigan which has managed to perform well despite the use of a wide network. Both insurers, incidentally, had a very positive claims and premium experience in the first year of the ACA according to risk corridor payment data.

(None of this is to say that the ACA individual market standards and operations are without fault. The law needs a tweak and with the public and the GOP ready to give up on repeal of the law, that just might be what happens. Topping our list is a reduction of the long, nonsensical and nonclinical list of required Essential Health Benefits that even the reform minded Institute of Medicine could not abide. Beyond that, we would like to see a little more fexibility in the various medal level plans to enhance affordability.)

Nothing Counihan says in his interview is new. Neither is what Patrick Geraghty, CEO of Blue Cross and Blue Shield of Florida and Bernard Tyson, CEO of Kaiser Permanente said in theirs last week. Yet, AET, which certainly has the resources to withstand the losses they reported from their individual market exchange business while they retool for the paradigm shift mandated by the ACA, decided to stick a finger in the Obama administration’s eye Their actions suggested both retaliation for the DOJ’s intervention in their merger with HUM and lack of comprehension about federal health policy and its direction.

Investors take note: AET is playing checkers when the situation calls for chess.